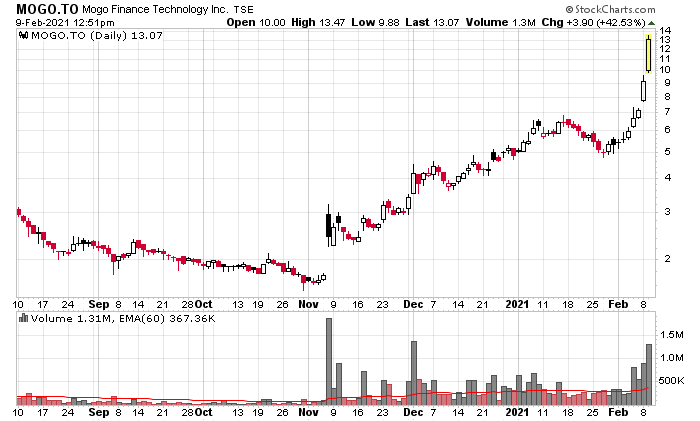

Look what popped up on my radar today – Mogo Finance (TSX: MOGO), primarily due to its massive price increase.

I’ve been looking at them on and off since they merged with Difference Capital a couple years back (this was to save MOGO as an entity since they were heavily indebted and no proper refinancing routes with their ultra-expensive line of credit). I had a prior investment in the debentures of Difference Capital, and hence the interest (they had an equity interest in MOGO).

Mogo also had a matter with their convertible debentures, which were extended, this was back in April of last year.

My very quick take of Mogo at the time was that they were not making money, and they were quite unlikely to make money given that their credit facility was priced at 12.5% plus LIBOR, although this was re-priced to 9% plus LIBOR (effectively 10.5%). They also had a non-publicly traded debenture that was also expensive (note 10 in their Q3-2020 financial statement if you care to look).

So when you look at the stock chart above, instantly, you realize that the business is now going to get an extension on its life because they will be able to raise equity financing.

Why did they get such a bounce?

Just take a look at their website. They are trying to be like a Canadian version of Robinhood, mixed in with some consumer finance.

And now, of course, they are getting into Bitcoin.

I can see why the market is ramming up the stock of this company, which did $2.3 million in operating income for the first nine months in 2020. A market cap of CAD$500 million is cheap in comparison to what Robinhood’s last secondary offering was reported to do (apparently during the Gamestop fiasco their revised valuation was at US$30 billion).

I am somewhat mystified and frustrated at my lack of imagination to correlate the two together. Was this thing worth a stab at a valuation of CAD$50 million (plus debt?). The convertible debentures would have been a relatively cheap entry point, with some seniority over the common.

When I look at my portfolio at present, it is most definitely an “old man’s” portfolio of very real-economy type stocks. The most technological of them is Corvel (Nasdaq: CRVL) which produces software that is in a dominant niche (my one and only post on it is here), but this is hardly a millennial starling! I can’t be the only investor out there that is getting this type of feeling that I am getting too old for the markets.