Brookfield Business Partners (TSX: BBU.UN) announced a $750 million investment (Brookfield’s release) (Teekay’s release) in Teekay Offshore (NYSE: TOO).

I’ve written extensively about Teekay Offshore and thought they would cut their distributions to zero and likely cutting their preferred unit distributions because of impending financing issues. This prediction turned out to be mostly incorrect – they are cutting their common unit distribution to 1 penny per quarter (down from 11 cents), and maintaining their preferred distributions.

In general, my expectations for the outcome for this pending recapitalization transaction have been worse than what materialized.

Not surprisingly, Offshore’s preferred units are trading considerably higher in the markets – up about 28%.

Teekay (parent) unsecured debt traded up to 98.5 cents on the dollar today – I am happy regarding this transaction – it is likely to mature at par (January 2020) or earlier via a call option. Offshore debt holders have even more reason to be happy – theirs are up from 82 cents to 97 cents, with a 7% yield to maturity. (On a side note, I notice somebody was asleep at the switch at 5:00am today – there was a $100k bond trade for 90.8 cents on TK unsecured, which was a steal for the buy-side – NEVER leave those GTC orders out in the open unless if you’re willing to scan the news before the market opens!).

Summary thoughts (apologies in advance for this not being in a more professional manner, I am not writing from my usual location):

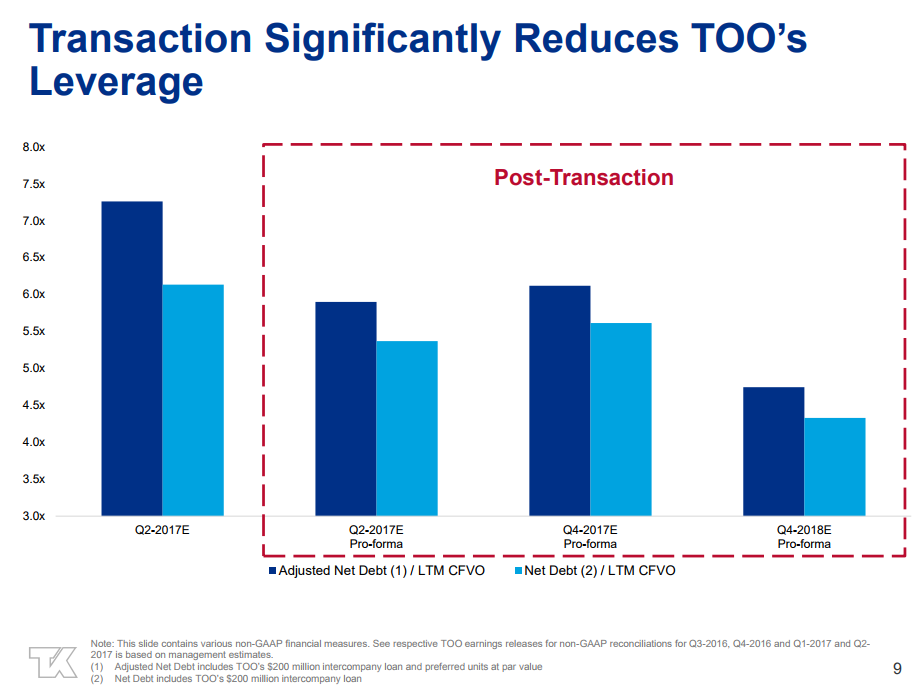

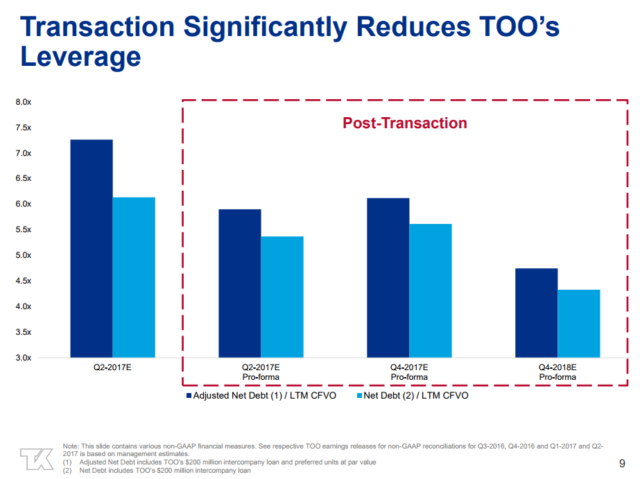

The first chart is from their today’s presentation, while the second chart was from an early 2016 presentation. Compare the two:

1. With this equity injection, Offshore buys itself a couple years of time (which is what they desperately needed) – however, their debt leverage goes from “very high” to “above average” – slide 9 is considerably above what they were anticipating in their 2016 slide when they initially recognized the pending financial crisis. Pay attention to the Y-Axis of those charts!

2. Teekay dumps its $200 million loan to Brookfield for $140 million cash and 11 million warrants in Offshore;

3. It’s not entirely clear what the terms of these warrants are, or how Brookfield picks up 51% control of the GP (they get 49% of it right now);

4. Offshore’s financial metrics (cash flows through vessel operations) should start to improve, but I suspect there will be upcoming challenges as long as the oil price environment is not supportive (thinking counterparty risk, potential future contract renewals, pricing pressure, etc. – examining Diamond Offshore, TransOcean, etc., although not strictly in the same market as TOO, leads one to believe that the present environment is also not favorable to maintenance offshore oil production expenditures);

5. Teekay also liquidated their preferred unit holding in Offshore, and this is functionally a sell-off to Brookfield.

6. The creation of a “ShuttleCo” subsidiary of Offshore will create some more financial complexity in the operation – they probably want to spin this out for valuation and/or leverage purposes (as this division apparently is doing reasonably well).

7. Offshore’s operational challenges and risks are still not going away with this equity injection, but Teekay has more or less divested as much as they could from them.

8. Teekay also get relieved of guarantees from Offshore, which will improve its financial position dramatically in the event of insolvency (this is huge for Teekay unsecured debt holders). Teekay is functionally at this point a play on their LNG daughter entity, while having some minority economic participation in offshore.

9. Teekay’s cash flows through Offshore will obviously be curtailed significantly, they have their own vessel operations which are cash neutral, so they will be solely reliant on either equity distributions of Offshore (if they decide to fully liquidate) or LNG’s distributions.

If I was an investor in the preferred shares or debt of Offshore, I’d be taking gains right now and going elsewhere.

I remain long TK unsecured debt and do not have any intentions to sell – I took a full position back in them last year. I’m not keen on any of the equity.