You know you’re starting to get old when you consistently start reciting your own work from years on back.

Does anybody remember Husky Energy (now consumed by Cenovus Energy) tried to take out MEG Energy at $11/share in 2018?

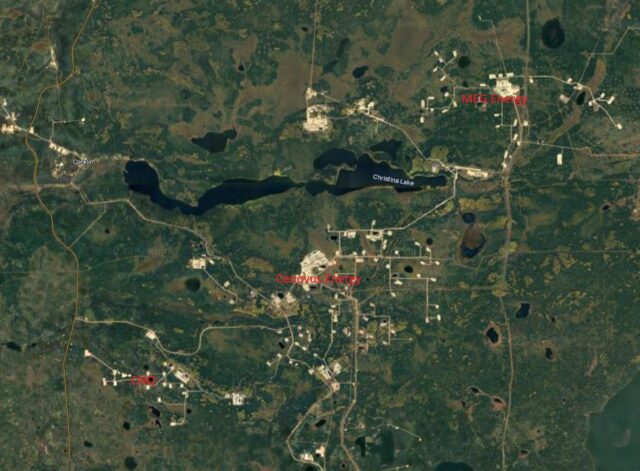

Subsequent to this, I wrote about MEG’s pending takeover in May and December of 2021 where I speculated that Cenovus was the most likely strategic acquirer of MEG Energy. There are significant synergies with the acquisition, including geographical ones (Cenovus and MEG Energy are side-by-side at Christina Lake, Alberta):

(MEG is on the north-eastern end of the lake, CVE is on the southern and northern end, and CNQ is on the southwestern end)

For those unaware, these oil sand assets are the crème de la crème of the Alberta oil sands – they have the best steam-to-oil ratios out of all the oil sands. As most of the capital has already been spent on the projects, they will be generating cash flows for decades. It cannot be understated how valuable this asset is whether oil is trading at 50, 75 or 100 a barrel – they are the lowest cost production fields in North America.

Indeed, I wrote those articles when MEG was $12/share and my very pithy analysis speculated that one of CVE or CNQ would just do a 30-40% premium buyout and get it over with. This would have been about $17/share equivalent. The only element that has changed since then (the commodity price environment round-tripped after the Russian invasion of Ukraine, and when adjusting for Canadian currency and the narrower WCS differential the price is virtually the same today as it was back then) is the price being paid – roughly speaking, $5.2 billion in cash and 84 million shares of CVE for a grand total of about $7.2 billion at today’s market value of CVE or about $28/share for MEG.

This is a very unusual transaction considering that Strathcona’s offer was originally higher than Cenovus’ offer, but the even more shocking factor to me is that Cenovus is trading higher after delivering a lower bid than Stratcona, which MEG agreed to!

I wasn’t expecting this set of circumstances to be on my bingo card.

When running my paper napkin calculations, it will be a synergistic acquisition. Just looking at an apples-to-apples comparison in 2024, CVE trades at 11x EV/FCF, while MEG trades at 10x – this is using the currently elevated share prices at August 27, 2025.

There are other synergies – there are plenty of greenfields in the MEG geographical footprint to facilitate the maintenance of their SAGD projects, TMX allocation, and tax shield assets which will deliver quite a bit more cash flow to the underlying Cenovus entity (not to mention the cost elimination of a management layer). The CVE cash portion will be funded by low cost (and tax deductible) debt and the leverage situation after the acquisition is still modest. Finally, MEG in the end of 2024, in an attempt to appear relevant, announced they would spend about half a billion dollars in what they titled a “Facility Expansion Project”, adding 25,000 boe/d of production in a few years – presumptively this project will be canned as half a billion dollars is one hell of an opportunity cost when you have a limited geographical footprint like MEG did (not to mention egress issues).

Strathcona will also get a tactical victory by virtue of its short-term investment in MEG paying off, but strategically they are still looking for ways to tap into the very valuable market of having enough of a stock float to be picked up by index ETF investors – I am absolutely sure they will be on the prowl in the oil patch to boost their own liquidity. At this point the only other obvious target that is publicly traded is Athabaska Oil Sands (TSX: ATH), but they’ve received too much of a bid recently in anticipation of exactly that.

What is ahead in the Canadian fossil fuel industry?

From a broad strategic perspective, the next logical merger would be Cenovus and Suncor. The major synergy here is with the refining networks both companies have – internal consumption of your own product hedges against the inevitable egress risk that will be coming up later this decade. Irvine, Valero, Shell and Imperial Oil would still be primary competitors in the refining space.