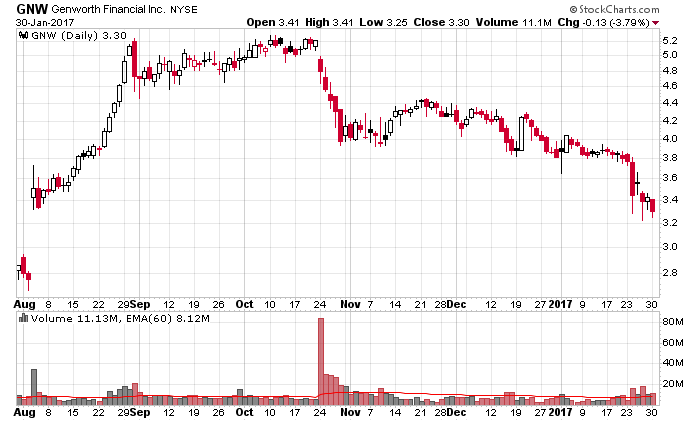

Imagine my initial surprise when I saw a news feed that Genworth had been bought out. Unfortunately for me, it was Genworth Financial (NYSE: GNW) and not Genworth MI (TSX: MIC).

Genworth Financial is being taken over by China Oceanwide Holdings, chaired by Lu Zhiqiang, who apparently has a networth of $5 billion.

In the press release, there are scant details. They mentioned the buyout price and the intention of the purchaser to inject $1.1 billion of capital into Genworth to offset an upcoming 2018 bond maturity and shore up the life insurance subsidiary, but the release also explicitly stated a key point:

China Oceanwide has no current intention or future obligation to contribute additional capital to support Genworth’s legacy LTC business.

The LTC (long-term care) insurance business is what got Genworth into trouble in the first place, and its valuation is the primary reason why the company’s stated book value is substantially higher than its market value.

The press release also declared that this is primarily a financial acquisition rather than a strategic one, with management and operations being intact.

One wonders how long this will last.

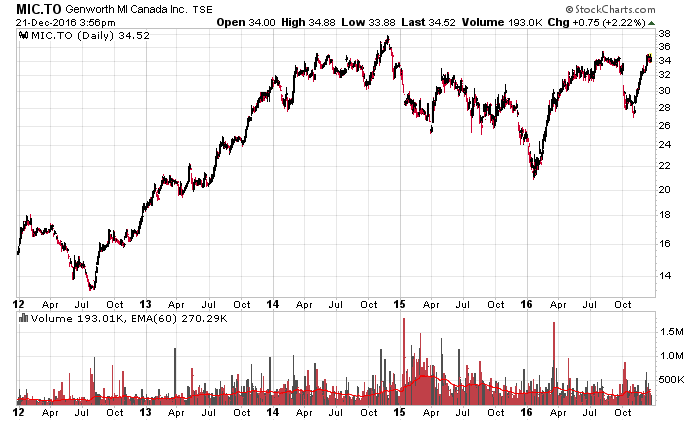

Since Genworth Financial controls 57% of Genworth MI, it leads to the question of what the implications for the mortgage insurance industry will be – and it is not entirely clear to me up-front what these implications may be. Will the government of Canada be comfortable of 1/3rd of their country’s mortgage insurance being operated by a Chinese-owned entity? What is the financial incentive for China Oceanwide’s dealings with the mortgage insurance arms of Genworth Financial (noting they also own a majority stake in Australia’s mortgage insurance division)?

One thought that immediately comes to mind is that if Genworth Financial is not capital-starved, they will no longer be looking at ways to milking their subsidiaries for capital. In particular, if Genworth MI decides to do a share repurchase, they might opt to concentrate on buying back the public float (currently trading at a huge discount to book value) instead of proportionately allocating 57% of their buyback to their own shares (in effect, giving the parent company a dividend). This would be an incremental plus for Genworth MI.

Finally, one wonders what risks may lie in the acquisition closing – while it is scheduled for mid-2017, this is not a slam dunk by any means. Genworth Financial announced significant charges relating to the modelling of the actual expense profile of their LTC business and it is not surprising that they decided to sell out at the relatively meager price they did – there’s probably worse to come in the future.

However, as far as Genworth MI is concerned, right now it is business as usual. There hasn’t been anything posted to the SEC yet that will give me any more colour, but I am eager to read it.

(Update, early Monday morning: Genworth 8-K with fine-print of agreement)

Yes, I’ve read the document. Am I the only person on the planet that reads this type of stuff at 4:00am in the morning with my french-press coffee? Also, do they purposefully design these legal documents to be as inconveniently formatted as possible, i.e. no carriage returns or tabs at all?

A lot of standard clauses here, but some pertaining to subsidiary companies (including Genworth MI), including:

(page 47): Section 6.1,

the Company will not and will not permit its Subsidiaries (subject to the terms of the provisos in the definition of “Subsidiary” in Article X) to:

…

(viii) reclassify, split, combine, subdivide or redeem, purchase or otherwise acquire, directly or indirectly, any of its capital stock or securities convertible or exchangeable into or exercisable for any shares of its capital stock (other than

(A) the withholding of shares to satisfy withholding Tax obligations

(1) in respect of Company Equity Awards outstanding as of the date of this Agreement in accordance with their terms and, as applicable, the Stock Plans, in each case in effect on the date of this Agreement or

(2) in respect of equity awards issued by, or stock-based employee benefit plans of, the Specified Entities in their respective Ordinary Course of Business and

(B) the repurchase of shares of capital stock of Genworth Australia or Genworth Canada by Genworth Australia or Genworth Canada, as applicable, pursuant to share repurchase programs in effect as of the date hereof (or renewals thereof on substantially similar terms) with respect to such entities in accordance with their terms);

(note: Genworth MI’s NCIB expires on May 4, 2017)

(page 53): (e) During the period from the date hereof to the Effective Time or earlier termination of this Agreement, except as set forth on Section 6.1(e) of the Company Disclosure Letter, or as required by applicable Law or the rules of any stock exchange, the Company shall not, and shall cause any of its Subsidiaries that are record or beneficial owners of any capital stock of or equity interest in Genworth Canada or any of its Subsidiaries not to, without Parent’s prior written consent (which consent, in the case of clauses (ii)(B) and (iii) below (and, to the extent applicable to either clause (ii)(B) or clause (iii) below, clause (iv) below) shall not be unreasonably withheld, conditioned or delayed):

…

or (z) any share repurchases that would not decrease the percentage of the outstanding voting stock of Genworth Canada owned by the Company and its Subsidiaries as of the date hereof)

(note: Hmmm… this does open the door for repurchases).

I’m still unsure of the final implication on Genworth MI other than the fact that if this merger proceeds that the parent company is going to lean less on their subsidiaries for capital.