I will be terminating the Divestor Canadian Oil and Gas Index (DCOGI) effective today. It took a bit too much effort to administrate (the dividends, in particular, were cumbersome) and also this might be a signal the fossil fuel trade is nearly over.

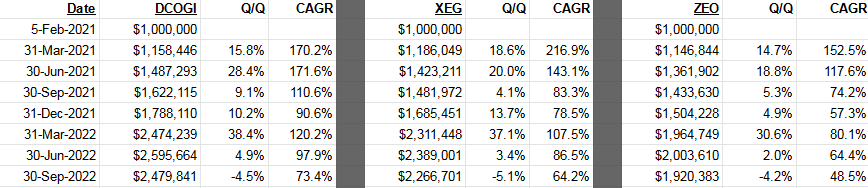

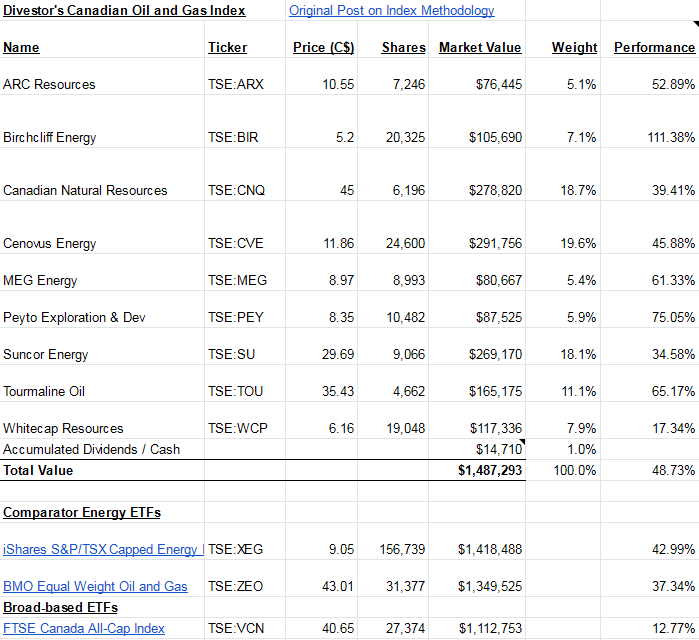

The DCOGI was created on February 5, 2021 with a hypothetical million dollars invested among 9 very well known Canadian oil and gas companies, with the larger companies having more weighting.

From an index level of 100 at February 5, 2021, the DCOGI ended 2022 at 283.9.

The comparators were the energy ETFs XEG.to, ZEO.to and the broad-based index ETF VCN.to.

XEG ended at 257.5;

ZEO ended at 209.6;

VCN ended at 113.2.

These values are all with one dividend reinvestment cycle at the end of 2021, otherwise for 2022 the cash from dividends accumulated yield-free.

In 2022, the DCOGI had an 11.9% cash yield based off of its initial cost, an indication of the incredible amounts of cash flow that have been spun off by this sector (the primary contributor to this was Tourlamine’s special dividends, with CNQ as a close second).

2023 should also feature, if indications suggest, that increased cash yields will be coming from ARX, BIR, CVE, PEY and WCP in relation to 2022.

I will leave the final spreadsheet here in case if anybody wants to continue the work, but otherwise it will be kept in an unmaintained state.