I’m not one to typically invest in pipelines. All of them are quite heavily levered, and in most cases, it is justifiable with the predictable streams of cash flows they generate. As a result, the equity is typically treated like a bond by most investors, plus you add a couple percent to make up for the ‘risk premium’.

In the Canadian retail space, there’s no better example of this than Enbridge, where investors blissfully clip their 74 cent a quarter dividend, with the promise by management that this will grow 10% a year indefinitely. The fact that there’s 65 billion in debt and 8 billion in preferred shares ahead doesn’t matter because of those high cash flows, so one can safely assume you will receive dividends forever. The current headline yield of 6.6% sure looks good and can only go up from here!

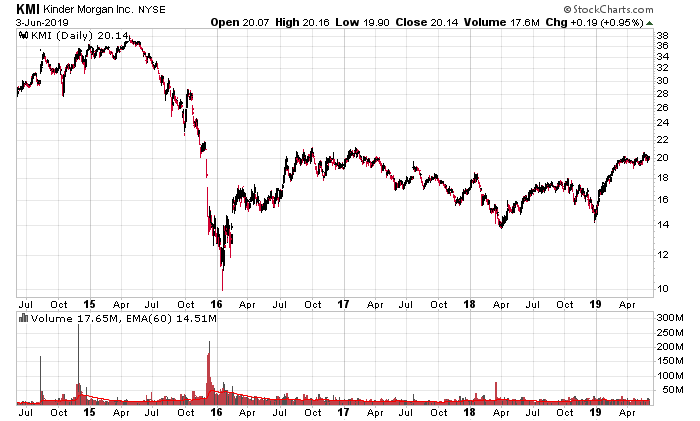

This might sound great, but investors of Kinder Morgan (NYSE: KMI) learned their lesson (2015) that some things can go wrong with this model and when corrections are required, shareholders take the hit and not the senior part of the capital structure. Taking equity risk on Enbridge in exchange for very limited capital appreciation upside is not my idea of a good investment, but I’ll digress.

Enbridge and other pipeline companies do have one virtue – because of intense political opposition, it becomes a lot more difficult to develop pipelines, especially in Canada. Thus, there is a huge element of advantage to incumbents. Even if you gave a competent oil major $30 billion, you wouldn’t be able to replicate Line 3 or Line 5 from scratch. Especially with Canada’s Bill C-69, there is really no point – TransCanada learned the tough way (even without C-69) that Energy East is a dead cause because of politics. The only real option these days are avoiding the federal scene entirely and going for intra-provincial pipeline infrastructure. An example of this is the Coastal Gaslink pipeline, connecting the northeastern BC gas formation to Kitimat, BC for LNG export. Even this has received heavy opposition of all sorts, but they were able to miraculously make agreements with all 30 elected First Nations councils and get the thumbs-up from the provincial NDP government (despite having a Green party coalition partner), which has been one of the big political surprises over the past couple years.

Which brings me to another pipeline company – Inter-Pipeline (TSX: IPL). What has been encumbering the company is the construction of their propane to polypropylene refining facility, which needless to say, is very expensive (all of this political talk of being able to refine your own production is completely uninformed about how expensive these facilities are and how much expertise they require to construct and operate – they don’t come up on their own like marijuana!). Their cost estimate of $3.5 billion is probably conservative and looking at the balance sheet, simply put, they have enough debt as it is without constructing this facility.

Now the media has caught wind that somebody wants to take them over, and somebody floated an unsolicited bid for $30 for the whole thing. Management rejected it, but this is starting to get the stock market interested. It’s an interesting valuation when considering that the enterprise value at IPL stock at $30 is 7 times the annualized revenues (1H-2019), while Enbridge’s is currently 3 times.

Appendix – Bill C-69

Here is a snippet of the new requirements that the environmental impact (now “impact assessment”) agency must consider:

Factors — impact assessment

22 (1) The impact assessment of a designated project, whether it is conducted by the Agency or a review panel, must take into account the following factors:

(a) the changes to the environment or to health, social or economic conditions and the positive and negative consequences of these changes that are likely to be caused by the carrying out of the designated project, including

(i) the effects of malfunctions or accidents that may occur in connection with the designated project,

(ii) any cumulative effects that are likely to result from the designated project in combination with other physical activities that have been or will be carried out, and

(iii) the result of any interaction between those effects;

(b) mitigation measures that are technically and economically feasible and that would mitigate any adverse effects of the designated project;

(c) the impact that the designated project may have on any Indigenous group and any adverse impact that the designated project may have on the rights of the Indigenous peoples of Canada recognized and affirmed by section 35 of the Constitution Act, 1982;

(d) the purpose of and need for the designated project;

(e) alternative means of carrying out the designated project that are technically and economically feasible, including through the use of best available technologies, and the effects of those means;

(f) any alternatives to the designated project that are technically and economically feasible and are directly related to the designated project;

(g) Indigenous knowledge provided with respect to the designated project;

(h) the extent to which the designated project contributes to sustainability;

(i) the extent to which the effects of the designated project hinder or contribute to the Government of Canada’s ability to meet its environmental obligations and its commitments in respect of climate change;

(j) any change to the designated project that may be caused by the environment;

(k) the requirements of the follow-up program in respect of the designated project;

(l) considerations related to Indigenous cultures raised with respect to the designated project;

(m) community knowledge provided with respect to the designated project;

(n) comments received from the public;

(o) comments from a jurisdiction that are received in the course of consultations conducted under section 21;

(p) any relevant assessment referred to in section 92, 93 or 95;

(q) any assessment of the effects of the designated project that is conducted by or on behalf of an Indigenous governing body and that is provided with respect to the designated project;

(r) any study or plan that is conducted or prepared by a jurisdiction — or an Indigenous governing body not referred to in paragraph (f) or (g) of the definition jurisdiction in section 2 — that is in respect of a region related to the designated project and that has been provided with respect to the project;

(s) the intersection of sex and gender with other identity factors; and

(t) any other matter relevant to the impact assessment that the Agency requires to be taken into account.

My comments: Good luck! Especially with the very quantifiable “intersection of sex and gender with other identity factors” criterion.