Sometimes an investment stares at you in the face and it is so obvious that it makes you wonder why others do not see it this way.

This is the case with Birchcliff Energy (TSX: BIR). Now that it has appreciated well beyond its Covid lows, I’ll write a little more about it in detail. I’ve been long shares of this (both common and preferred) for quite some time.

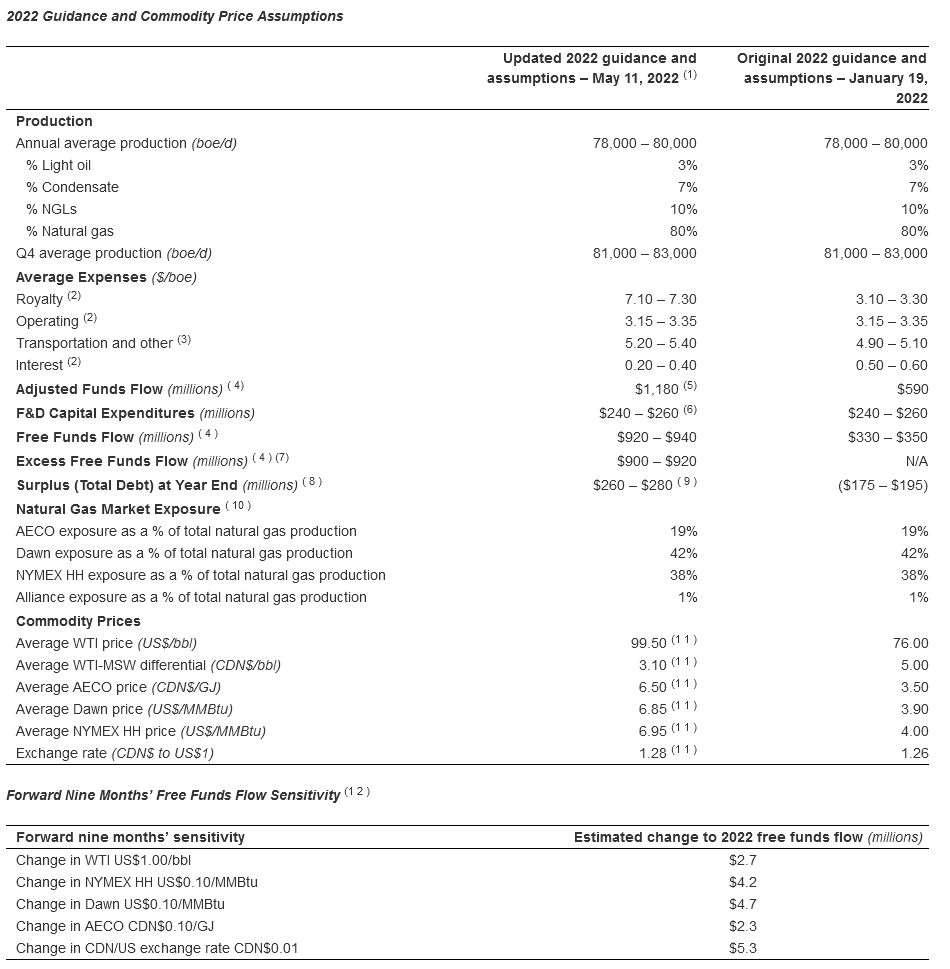

In 2022 it will produce about 79,000 boe/d equivalent (exit 2022 at approx. 82,000 boe/d), of which 80% of it is in the form of natural gas. All of this production is in the northwestern Alberta area, right up to the BC border.

Thus, the primary driver for this company is the state of the natural gas market. It has exposure to Dawn, Henry Hub and AECO.

Birchcliff is an unusual company in that they do not host quarterly conference calls. Instead, they issue information through large press releases and make it very easy to look at the assumptions. Although I have no problem sharpening my pencil and doing the leg works to do a proper pro-forma projection given various commodity price environments, Birchcliff expedites this process considerably.

There is some fine print to wade through, but the point is that BIR will generate $910 million in “excess free funds flow” (effectively cash flows after capex and projected dividend payments) with the average commodity prices as displayed in the release.

Notably, spot WTI and the spot Henry Hub price is well above their assumptions (US$114 and US$9.2 as I write this). Dawn typically tracks Henry Hub. Let’s ignore that spot is higher than modeled rates in the press release.

$910M of “excessive free funds” translates into $3.43/share.

At Wednesday’s closing price of $11.56, that is 3.4x or a yield of about 30%.

Normally companies are constrained with leverage and debt servicing. At the end of 2021, Birchcliff had $539 million in net debt (which includes BIR.PR.C) and another $50 million for the redemption of BIR.PR.A. The redemption of the preferred shares will result in a $6.8 million annualized savings on dividends (3 pennies a share, every bit counts!).

This will leave the company with a positive net cash amount of $270 million at the end of the year (the “Surplus”), unless they decide to blow some money on acquisitions and the like. Importantly, the math does not have to be adjusted for a leveraged return (indeed, it has to be corrected in the opposite direction).

The company will also be making enough money to eat through most of its tax shield ($1.9 billion at the end of 2021) and start paying income taxes in 2023, if the current price environment continues. Still, at US$88 oil, and US$5.50 Henry Hub for 2023 assumptions, the projection is for $535 million or about $2/share in free cash flow.

The stated policy on what to do with the cash surplus is to dividend it out beyond that which is to be used for strategic purposes. Management does not appear to be big on share repurchases other than to offset dilution that which has been issued from option plans (which is a real cash cost and will drag cash flows accordingly).

They will increase the dividend to $0.80/year in 2023, which is a $212 million outflow. This dividend can be maintained at price levels that are unlikely to be seen barring a great depression.

If they dividend the rest of their cash flows, when plugging in current commodity prices, they can give out far more than $0.80/year in dividends. It would be closer to around $2.80, or about $0.70 per quarter. Needless to say, if this is what they did, the market would find the yield (24%) tough to resist.

This is a very similar situation to Arch Resources (NYSE: ARCH), where the company will be giving out half of its free cash flow as a dividend and the other half to buy back shares. Considering its Q2 dividend will likely be around US$11/share, the obvious value of a share buyback is apparent. I wish Birchcliff would more actively consider it, at some cut-off threshold. For example, they can buy back shares until the price gets to a point where it is at 15% projected long-term free cash flows, a very conservative metric for a beneficial buyback. Right now that would imply that buying back below $15/share will clear that hurdle. At 12%, that number is about $19/share. There’s quite a way to go from current market prices.

None of this is a huge secret. It’s all in plain sight. It all relies on elevated commodity prices.