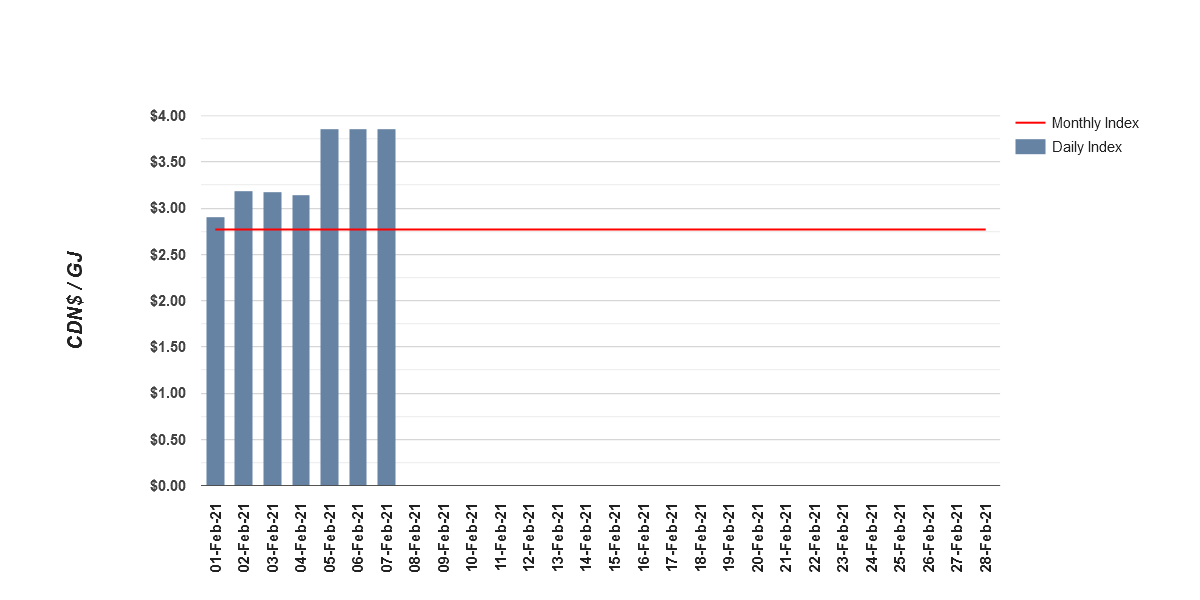

Natural gas producers are getting a spike today because of spot demand:

Just remember a couple years ago AECO was at nearly negative pricing due to the glut caused by US shale oil producers (and this resulted in a lot of associated natural gas production).

Different story today. US shale peaked at the end of 2019.

The other story will be how every piece of “clean renewable” electricity generation is going to be a stealth increase in future natural gas demand. The higher the potential volatility peaks in electricity generation, the higher the requirement will be for dispatachble sources – this comes either in the form of hydroelectric or natural gas. Ultra-large batteries are possible but they suffer from significant losses and they depreciate relatively quickly.

Hydro is pretty much tapped out – most of the good sites are built, and here in British Columbia, we’re having incredible difficulty building the 900MW Site C project (indeed, it might even be scrapped even though a few billion have been dumped into it).

The flip side of the equation will be some “demand management” applications where people will be compelled to use the bulk of their electricity generation in off-peak times (e.g. charging your electric vehicle after 9pm) and giving pricing incentives to doing so. Still, the efficiency gains to be made using demand management will be limited. Are factories going to be compelled to operate between 8pm to 6am because of electricity load factors? I don’t think so.

Until such a point where policy makers become serious about increasing base load power supplies, these sorts of problems will increase as intermittent sources become increasingly large fractions of the electric grid. You can stall the problem with using imports as buffers, but this solution only goes so far as California discovered last summer.

Similar to the concept of liquidity in the financial marketplace, intermittent electricity generation sources (wind, solar) are much more expensive than their numbers would seem because it involves a surrender of “power liquidity” – getting the power when you want it, not when it passively is received by you. Right now the cost of this liquidity is being outsourced to others, but as the value of this liquidity continues to increase, the true cost of intermittent sources becomes much more known.

Is there a scenario where nat gas prices are much higher in the future as demand increases at the same time there is less supply (maybe less oil extracted and less “byproduct” nat gas). In other words, what is the breakeven cost of nat gas if it has to be extracted on its own right (not sure if that makes sense / is the right way to look at it?)

Companies like TOU, ARX, BIR, VII and PEY are primarily gas drillers, CNQ also does a fair quantity of gas as well, so you can look at them…

The Labrador dam, Muskrat Falls, has also been a total disaster to build and is projected to break even now at 30-32 cents/kwH, last I checked. It is also bankrupting the province and causing a headache for Ottawa, which will probably cast another dampening layer on any other possible hydro development.

Stealthy, incremental increase in demand for NG with the deployment of renewables is an excellent point Sacha. However, hydro isn’t tapped out from this perspective. For every MWhr produced by intermittent renewables, an equivalent MWhr can be held back behind the dam. In this sense, there is huge runway to introduce renewables into the mix in places like BC and Quebec. It does, however, change the economics of hydro as total energy dispatched could fall resulting in higher fixed costs per unit of energy (mitigated somewhat by higher prices presumably).

By “tapped out”, I meant the physical locations for major hydro projects (there’ll be some dinky run-of-river projects here and there that’ll get built). The capacity utilization of hydro to serve as the buffer for intermittent has quite a bit of runway to go, but that’s going to go pretty quickly, especially for those renewable-heavy jurisdictions reliant on imports…

Gotcha. It’s going to be very interesting to see how renewables equilibrate in the system. Grid integrations through tie lines and trans-jurisdictional high capacity distribution are the least talked about but most impactful changes to come I think. At extremely low interest rates, this type of infrastructure gets much easier to build. Low rates also give a boost to capital-intensive, no fuel generation – like wind, solar and hydro – and to battery storage vs intermittent generation (gas). Nuclear ought to have a bigger role, but will it? All of this and more will play out in real time. Will be fascinating to navigate investment-wise.

I wonder whether this’ll be Maxim Power’s year…something I’ve wondered annually for over a decade…

I sold all of my BIR.PR.A and C yesterday at basically par…..My cost was was below 19 and 18. I feel the markets are very frothy and everything will get pulled down, deservedly or not. Natural gas has not peaked imo, but will be lower by april. I also expect OPEC and Russia to raise output soon, and Biden and the European union will come to an agreement with Iran who will add their oil to the marketplace.

Spot gas will always go down after the winter freeze is done, plus when the ground is frozen at -35 degrees that’s the time the drillers do their thing up in Alberta and NE BC. There’s a reasonable chance that the BIR prefs get redeemed next year, in the meantime, I’m happy to be getting my very low risk tax-preferred yield while it is still around. I don’t see anything worthy in fixed income at the moment, hence my reluctance to do the same.

Yes…they’re good issues…I have had success flipping these before, and will try again.I have my starting bids in at 24.

I preferred to dump them at 4 cents over par, and buy them back again at 60 cents… I don’t think I’ll be seeing that ever again sadly.

Not sure why you wouldn’t want to wait a couple months and just put the C’s back to BIR, you’d clip the dividend and also get the extra 5% spike on an equity conversion (or a $25 redemption). But otherwise, taxes notwithstanding, the trade is sound if you have somewhere to redeploy. The fixed income choices for a solid 850bps is few and far between though.

Trying to squeeze every last penny out of a trade has cost me dearly in the past….I dont have anywhere to redeploy atm….just getting 1.8% until new ops come up, which I expect

to be forthcoming with this bubble.

sorry…getting 2.3%

Given BIR’s quarter, if things keep up until September 2022, I don’t think BIR.PR.A is going to last long at all.