Wow, that was quick.

I said less than two weeks ago:

One major event that will occur in the future (a matter of when, not if) will be a significant power grid failure that will have been instigated by having too much intermittent energy sources on the grid, without available backup from domestic or external grid sources. This may be caused by a freak transmission failure (cutting an intermittent-heavy grid from a dispatch-able heavy grid) or some other ‘black swan’ event. When this occurs, there will likely be a dramatic shift in power generation policy to increase the robustness of a domestic power grid.

And what did we get last Saturday? Headlines such as:

(August 14, 2020) * Stage 3 Emergency Declared; rotating power outages have been initiated to maintain grid stability

(August 15, 2020) ISO Requested Power Outages following Stage 3 Emergency Declaration; System Now Being Restored

(August 16, 2020) Flex Alert Issued for Next Four Days, Calling for Statewide Conservation

What happened?

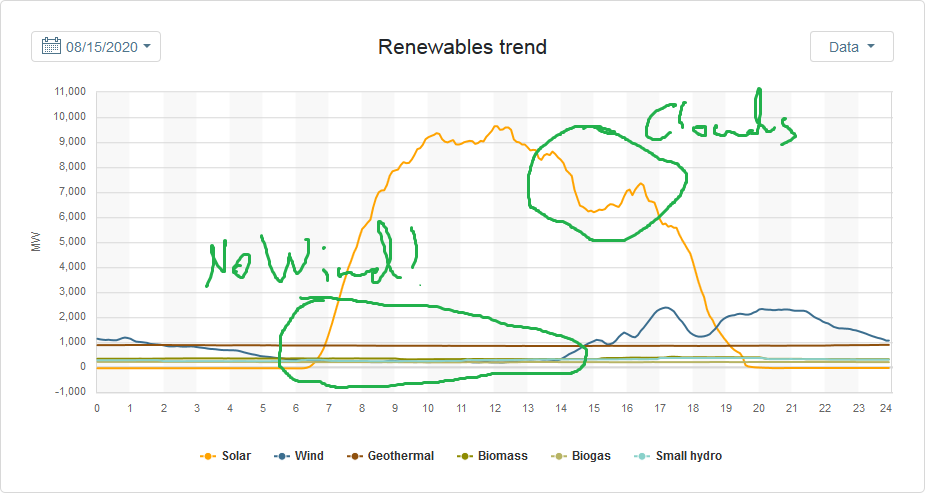

Excuse my crappy handwriting, but I had to illustrate this. Factors:

1. Wind dies down (can’t predict the wind very well, so you have no idea what your future supply is going to be);

2. Solar gets interrupted during the peak of the afternoon due to clouds;

3. Natural gas supply is down due to plant shutdown;

4. Cannot import (other grids are facing similar demand/supply issues).

5. Record-high daytime temperatures (e.g. Riverside, CA which is a suburb about 80km east of Los Angeles, at daytime highs of 40 degrees C), which causes huge demand for air conditioning.

What do you get? Rotating blackouts.

While I wouldn’t call this a “major event”, the fact that a major jurisdiction can’t keep the lights on speaks volumes.

This issue isn’t solved by adding renewables onto the grid – indeed, having too many renewables on the grid with the lack of dispatchable power sources was the cause of the problem.

If my suspicion is correct, this is going to be the start of a paradigm shift on what was a dead power production market (ruined by floods of cheap capital for intermittent power sources). I can’t tell whether this comes in the form of further power price increases (see: California, Ontario, Germany, etc.), increases in dispatchable energy supply (read: natural gas, nuclear or thermal coal!), or energy restriction mandates (or a combination of all), but either way, there are obvious investment angles coming down the line.

My only other comment is there are operational implications when you allow your quasi “crown corporation” primary power supplier PG&E (NYSE: PCG) to be sued into bankruptcy due to wildfire transmission line risk – when you get into situations like this weekend, it is obvious they will be shutting down transmission grids which reduces the robustness of a power grid since they don’t want to get sued to death again in case a spark catches fire somewhere. I wonder when they will get sued for constructive negligence because they shut down transmission lines and caused a huge cascade power failure which caused even more economic damage. Companies that operate under heavy regulatory coverage in California live and die at the behest of the state – watch out if you’ve got capital in PCG equity!