Input Capital (TSXV: INP) announced they were going to be bought out by a company (Bridgeway, trading as BDGY) for $1.75 in cash.

This represented nearly a double in share price and a total purchase price of nearly $100 million dollars.

The only problem is that when I am doing research on Bridgeway, I am getting the shell of an entity with a market cap of about $600,000 (yes, six-hundred thousand dollars).

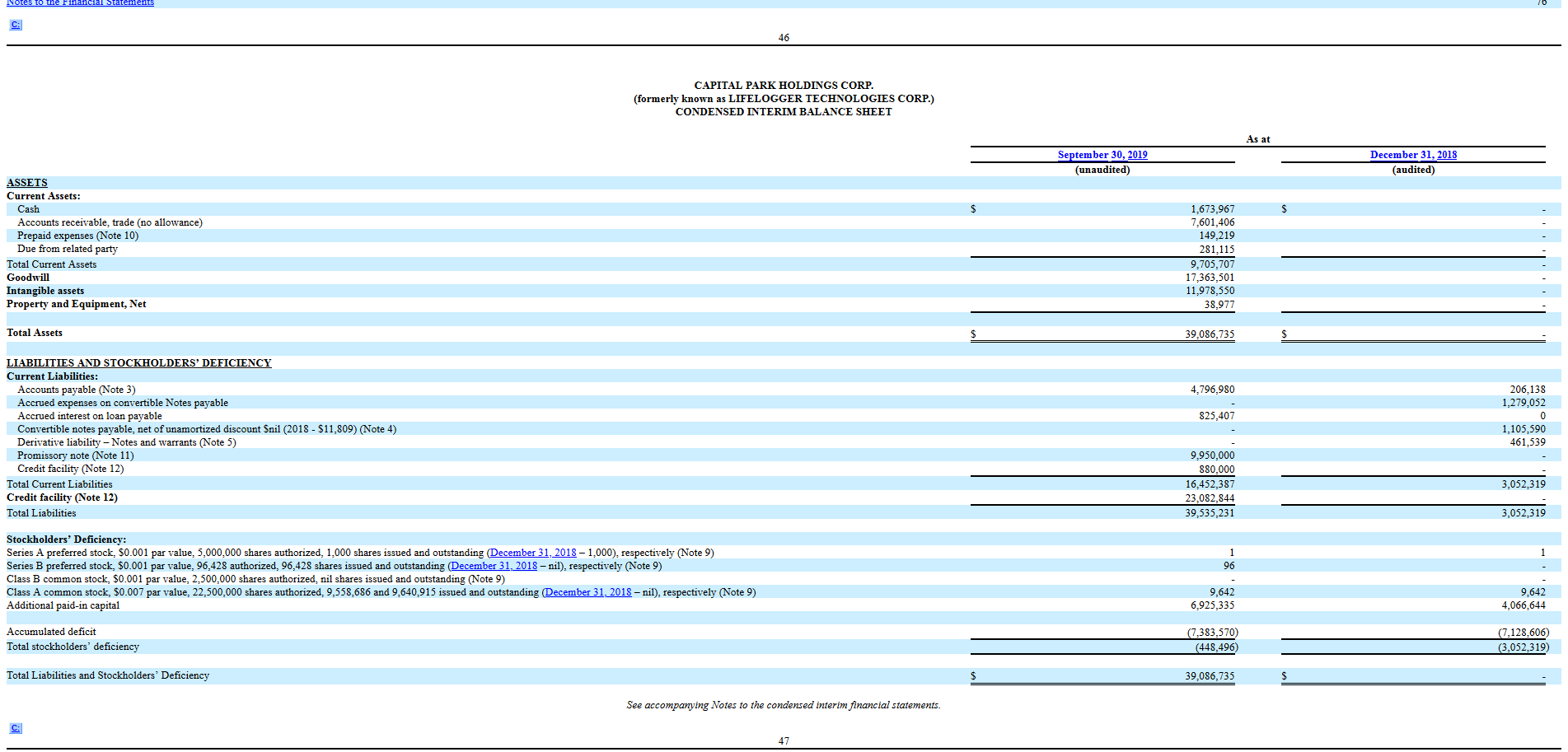

I dig into the SEC filings. They are late on their 10-K and 10-Q filings. Their last snapshot comes from their S-1 (registration statement) where on page 47 we see a financial statement, as of September 2019, that contains nowhere close to $100 million in cash. Indeed, it is about $1.7 million in cash and a whole bunch of liabilities (about $40 million).

There are no 8-K filings indicating they are in the receipt of any further financing except for about $750k (not million) they raised in March 2020.

I couldn’t find shares to borrow, hence this post. While I don’t give investing advice, I think my conclusion from this post is quite obvious.

Clearly a US entity with no money cannot pay (overpay!) $100M for a Canadian specialty finance company that recovers its dollar capital as canola.

Stalking horse bid (oh! that fell through but here is a management bid for $1.25)? A third-party private US entity financing a shell to expand the concept across the border?

Still no Form 8-K from Bridgeway… you’d think a publicly traded company with a market cap of less than $1 million would consider a $97.5 million acquisition to be a materially disclosable event!

Bridgeway National ($BDGY) posted their 10-K yesterday here

https://www.otcmarkets.com/filing/html?id=14399360&guid=Mwy6Uqt7kDuAd3h

No mention of the huge acquisition of Input Capital in there either. Not even in the “Subsequent Events” section. Something seriously smells about this. Thanks for the quick writeup.

Shareholders voted (not surprising in the least) 99.99% in favour of the deal. The last question is – will Bridgeway be able to find $100 million in spare change behind the couch to wire over to the transfer agent?

More properly – will the entity behind this deal purporting to use the Bridgeway shell find $100 million …?

They’re still looking between the cushions in the couch in their corporate headquarters… “I know that $100 million is here somewhere!”

Bridgeway filed 10-Q today for the 3 months ended March 31. 2020. Still nothing relevant to INP…

Doesn’t make any sense whatsoever to not even mention the Input Capital acquisition. Expected close is Oct 1 so we will see by week’s end

On the day of the expected close Input gets told “hold on wait a week”:

“The Company has received an update from the Purchaser with regard to closing and has been informed that the Purchaser will be in a position to close on or about October 9, 2020. Closing of the Plan of Arrangement remains subject to certain customary closing conditions.”

They’re still looking for the $100 million hidden in the couch!!

“Trust us guys, the cheque is in the mail, we’re told it will get there by the 9th”

Bridgeway filed 10-Q for June 30, 2020. Again, nothing there of relevance.

INP obtained court approval (https://www.newswire.ca/news-releases/input-capital-corp-obtains-final-order-approving-plan-of-arrangement-with-bridgeway-national-corp–878226177.html).

If this actually closes at the price involved, this is the most mysterious thing imaginable.

The market is putting a 99% probability on this thing closing. Insane. I really wish there was borrow available. Risk 2 pennies for 100 if it doesn’t close

Two more 8-K filings, relating to management hiring and compensation…

Eric Blue paying himself $500k which is 5x the amount of cash on the latest balance sheet. Makes sense in Bridgeway National Corp land.

Hiring Eon Washington as an exec who looks like filed for Chapter 7 bankruptcy in 2019.

https://www.docketbird.com/court-cases/Eon-Washington/nyeb-1:2019-bk-44226

Makes even more sense

The story gets even better, they finally filed an 8-K with their August 2020 press release about the Input takeover, and also instituted a stock buyback plan! Still looking for that $100 million…

Hahahahaha WTF is Bridgeway National Corp. and Eric C Blue doing???

A $5M share buyback plan with a stock that was $500k in market cap. But dummies fell for the pump so it’s $1.8M MC now. All with $97k in cash current on the balance sheet. Makes perfect sense in Bridgeway National Corp land. lol

If the Input Capital acquisition actually closes then I think the second coming of Jesus Christ is soon to come

The dummies at Bridgeway actually have the balls to backdate the PR here:

https://www.otcmarkets.com/filing/html?id=14425064&guid=PPH6UaGHcQH3M3h#EX99-1_HTM

There’s no record that this PR was released on August 18, 2020 that I can find. The first record I can find of this PR is from today.

I also love how there’s no expected closing date too. lol

“The cheque is in the mail. Really!”

LOL!

I really wonder what it’ll take for Input Capital to admit they’ve been had.

This just gets greater and greater… 8-K from Bridgeway today:

“Effective October 15, 2020, Bridgeway entered into two purchase agreements (the “Purchase Agreements”) pursuant to which we agreed to acquire 100% of the outstanding capital stock of Merchandize Liquidators, Inc., a Miami-Florida based direct wholesale and retail liquidator of surplus merchandise (“MLI”).

The first Purchase Agreement with CW Merchandize Liquidators, LLC (“CW Merchandize”), the minority shareholder of MLI (the “CW Merchandize Purchase Agreement”), provides for the acquisition of CW Merchandize’s shares in MLI in exchange for payment of cash consideration of $6.999 million. The second Purchase Agreement with Edgar Martinez, the majority shareholder of MLI (the “Martinez Purchase Agreement”), provides for the acquisition of his shares in MLI in exchange for the issuance of 252,644,000 shares of Bridgeway Class A Common Stock.”

So, they can apparently scrounge up another $7 million but we forgot about the $100 million we need for Input! Or maybe CW Merchandize (not Merchandise!!) has $100 million in their couch that they can use to pay for the Input transaction… better close the deal quickly!

“As disclosed in a Current Report on Form 8-K filed by Bridgeway National with the SEC on October 2, 2020, the Company and a newly formed Saskatchewan subsidiary intended to be a special purpose vehicle, entered into an arrangement agreement (the “ Arrangement Agreement ”) with and Input Capital Corp. (“ Input ”), a Saskatchewan, Canada based company which is engaged in agriculture commodity streaming with a focus on canola, the largest and most profitable crop in Canadian agriculture. Pursuant to the Arrangement Agreement Bridgeway National will acquire all of the issued and outstanding common shares of Input for cash consideration of CDN$1.75 per share (US$1.31 per share based on an exchange rate of CND$1.00 = US$ 0.76) or aggregate consideration of CDN$ 96.152million (US$73.1 million).

A portion, if not all of the purchase price for the Input shares may be raised through the sale of our capital stock, although the Company has no definitive arrangements therefor.”

Like everyone and their dog had figured out, Bridgeway National doesn’t have the cash to pay Input Capital shareholders. No definite arrangements to raise the cash either.

252.6M shares for dilution for this new crazy acquisition. I’m sure the Bridgeway National

stockbagholders will love that.This is the craziest series of events I’ve ever seen. Slow motion car crash that I can’t look away from.

Bridgeway can’t complete (surprise surprise), and the kicker in respect to the termination fee contemplated:

“and Input has provided banking instructions for the processing of the funds.”

Good luck collecting on that one!

Ah, the end of a wild story. What a ride.

Yeah, I very much doubt Input Capital will receive the termination fee.

The press release reads like Input Capital is completely blameless. Insane.

Congrats to those that sold in the 1.60-1.74 range on this “bid”. I don’t know what the heck the buyers at those prices were thinking.

Bridgeway filed 10-Q for September 30, 2020. $147,000 cash on the balance sheet. No mention of the INP merger attempt. Good luck to Input getting blood from this stone!

Going from acquired to acquirer, doing a weird pivot to “cyber security and physical protective services”. What has Input done to give shareholders any confidence they know what they are doing with this acquisition?

https://www.newswire.ca/news-releases/input-capital-corp-enters-term-sheet-to-acquire-srg-security-resource-group-inc–884433827.html

Interesting… Doug Emsley is the Chairman & CEO…

Wonder what his payout is?

https://securityresourcegroup.com/about/#senior-management

At first I thought it was just dumb, turns out it’s not dumb but it is very scummy

They have the financial strength to do it, in the form of the run-off of the residual streaming contracts at decent prices for canola. Bad move though – they really ought to have just run out the contracts buying back shares at a big discount to book along the way, then returning in one big whoosh of a special dividend. At that point, the shell would be ready for a reverse-IPO to allow some private entity to go public.

Wow. The only thing shocking about Input after this point is that people are still willing to buy the equity. Guessing those auto-purchases from dividend ETFs really do have an impact!

[…] was this post at Divestor, where several readers also commented knowing the deal was bullshit. There was a lot of posts on […]

The incompetence of Input Capital’s management and board continue to amaze. Just when I thought the Bridgeway National fake deal couldn’t be more dumb they come up with this.

The conflicts of interest and self-dealing couldn’t be any worse. LOL. Is corporate governance dead in Canada?