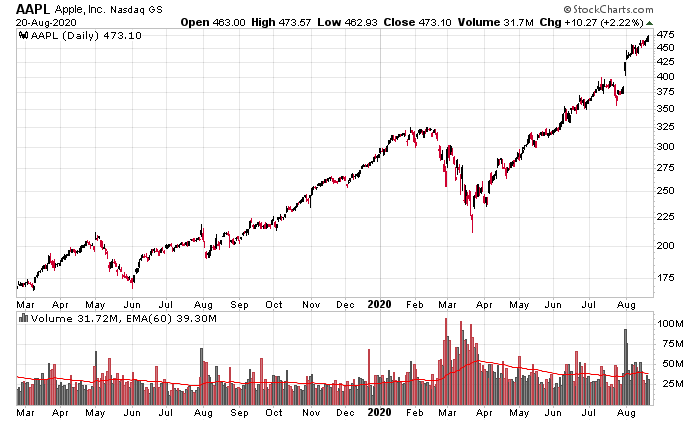

The S&P has more or less been on an uphill trend for the past 3 months. The last major incursion to the prevailing market trend was in June, which shook out the people with low amounts of conviction. Since then, the people that have cashed up during Covid (“let’s wait for a vaccine”, “let’s wait for case rates to go to zero”, “let’s wait for the presidential election to conclude”), etc. have been staring at stock charts of companies like Tesla, Microsoft, Zoom, etc., all rising in price. During the three month process, the temptation to buy becomes too much (“let’s board the train”), and that also starts attracting unsophisticated retail investors (Robinhood traders) into the mix.

There is still a lot of cash on the sidelines, and there is still a lot of pessimism out there in regards to Covid and the general state of the economy, so this cash will be the ultimate backstop to the markets.

However, once in awhile, the markets need to exhibit a “shake-out”, where confidence is obviously lost, and the sentiment turns short-term negative, such as the moment we got yesterday and today – what’s happening is that equity holders with less conviction are taking gains and this creates its own stampede of people that have decided that taking gains on the past three months of performance is “good enough”.

Note I haven’t mentioned a thing about valuation in this post. Of course companies like Apple, Microsoft, etc., are trading at elevated ratios. Where else are you going to stick your capital, 30-year US treasury bonds yielding 1.4%? Of course companies like Zoom and Tesla are over-valued, but over-valuation alone is not a sufficient condition for going all negative on the S&P 500. Indeed, if the entire S&P 500 index were to collapse 25% in the next week (without a corresponding change in interest rates), you’d have the media shouting about how everything is going to hell, but privately within the halls of pension funds and institutions, would be a pretty good chance to deploy cash into equities.

The underbelly of the high profile, high-PE, high capitalization stocks still shows a market that is relatively stable and doesn’t appear excessive.

I’m guessing this hiccup will be a two week ordeal, especially when combined with presidential election antics. Panicked hands will bail, and when they’re finished, we’ll begin the slow march up against the wall of worry.

Indeed, the implied volatility of the S&P 500 has spiked, where the short term contract (mid-September expiry) is hovering around the 35% mark, while the October contract is at 40%. This massive diversion is due to the anticipated effects of the US presidential election on equity markets.

In general, I would be a seller of volatility going into the election.

Finally, this is not to say there will be economic headwinds that will cause issues in the marketplace. But this is going to be a 2021 story, not 2020. All of this nearly free money provided through quantitative easing, central bank asset purchases, and the provision of massive government fiscal deficits will have consequences. The analogy is that the shot of meth has been given to the patient and the patient has been feeling really good. But this high only lasts for so long before you either have to pump up the patient again, or let the patient sober up.