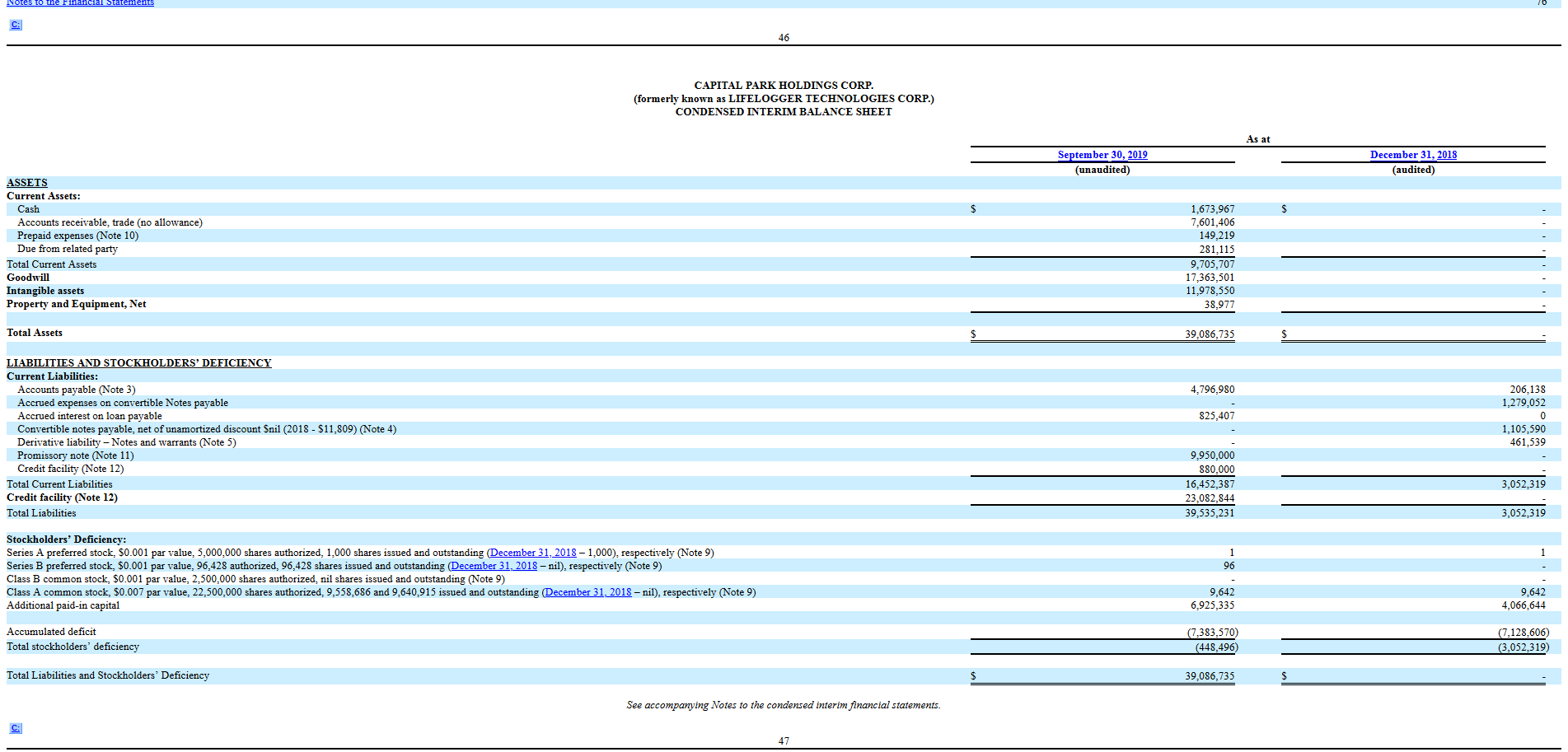

This post is a little more abstract, but the thinking should be fairly easy to understand. The revolves around the concept of hurdle rates, and making comparisons to baseline investments.

I’ve been reviewing a bunch of companies that have balance sheets that have tangible (or nearly tangible) financial assets that when netted against their liabilities are trading below liquidation value. An example of this would be Input Capital (TSXV: INP) which Tyler has tweeted about, in addition to SM keeping me informed by email.

In the case of Input, taking their December 31, 2019 balance sheet as-is without mental adjustments, gives them a $1.24 book value. At a current market rate of 71 cents, that’s trading at a 43% below book discount. Assuming the asset side of the balance sheet doesn’t have more write-down surprises, the company on the income side still makes a modest amount of cash on their canola/mortgage streaming business, albeit at a rather high cost on administration (as a percentage of assets). If they decide to wind down, shareholders should be able to get out with a mild positive. Their mortgage portfolio will amortize and the board of directors can command management to fire themselves and call it a day.

So lets assume I have a chunk of cash, and I’m evaluating this option for the portfolio. To be clear, I’m not interested, and INP has very poor liquidity – typical trading volumes in a day is less than CAD$10,000. Piling onto our list of assumptions, let’s say liquidity is no concern.

The question is: What do I compare this to?

If I compare this to the simple risk-free cash amount (e.g. the brain-dead option is (TSX: PSA) which yields a net 2%), then yes, Input Capital looks fairly good by comparison. If INP materially winds up in 3 years and captures 90% of its present book value (conservatively assuming they lose a bit in the process of wind-down), that’s a 16% CAGR gainer. You’re effectively getting 14% net on the risk-free option – the risk of this not happening is what you’re getting this 14% spread for (such as the critical assumption on whether they choose to liquidate or not!).

However, things are not so easy in our multiverse of investment options.

For instance, you have other choices. Coming up with baseline options is vital for making comparisons. Other than the risk-free option (government bonds or for smaller scale amounts of money, PSA), there are surprisingly a lot of companies out there trading under book value that appear to be making money.

Perhaps the least glamorous, most boring, but relatively safe option is E-L Financial (TSX: ELF) which owns nearly all (99%+) of Empire Life, 37% of Algoma (TSX: ALC), and 24% of Economic Investment Trust (TSX: EVT). At the end of Q3, its book value (stripping the $300 million of preferred shares outstanding) was $1,421/share while its market value today on the TSX is $814, which is a 43% discount below book value, identical to INP’s discount today. ELF also from 2009 to 2018 compounded its book value by 9.7% annually, and clearly is a profitable entity.

So we compare two opposing options: INP and ELF – why in the world would you choose INP? The only reason would appear to be a chance of a quick and clean liquidation over the next few years, and that is measured against ELF earning 10% of book value over those three same years, and staying at a 43% below-book valuation. The only thing you don’t get with ELF is an interesting conversation at a cocktail party.

The baseline comparison of ELF compounding book value at 10% a year creates quite a hurdle for other below book value investments – the underlying mis-valuations must be very severe in order to warrant an investment in other vehicles. When scanning my portfolio, all of the common share investments have clear rationales for expected returns higher than this hurdle rate.

When you compare to real bottom of the trash barrel options like Aberdeen International (TSX: AAB) which are trading 85% below book value, why would you want to put investment capital into a sub-$100 million market capitalization entity when there is a perfectly viable option that is clearly a legitimate firm, and has a very good track record of building its balance sheet? (For those financial historians out there, many years ago Aberdeen was subject to a bruising proxy fight where an activist tried to take over the board for the purpose of realizing book value, but the management was successful at fighting it and then proceeded to fritter away the company into what it is today – a 3.5 cent per share stock – shareholders got what they deserved!).

As a final note, the presence of fixed income options that appear to give off very high low-risk returns tends to make such comparative decisions really difficult. For example, Gran Colombia Gold’s notes (TSX: GCM.NT.U) are linked to the price of gold and give out more yield when above US$1,250/Oz. Given the seniority of the notes (they were secured by the company’s primary mining operation), even at the baseline gold price, the notes represented a very low-risk 8.25% coupon. At current gold prices, the coupon effectively rises to around 15%. It is difficult to compete against such investments, except in this specific instance they must be capped as a reasonable fraction of the portfolio (if the mine had an implosion, explosion, earthquake, etc., then there would be trouble). The opportunity is now gone since the notes are now in a redemption process and the remaining principal value will be whittled away with quarterly redemptions at par values below market trading prices, and the rest of it will likely get called off after April 30, 2021 (at 104.13 of par).

I won’t even get into comparisons with the preferred share market, where there are plenty of viable options with little risk that will yield eligible dividend yields roughly in the 6% range that would require an economic catastrophe of huge magnitude before they stopped paying out. The ebbs and gyrations of the underlying business itself is almost irrelevant to most of these preferred share issuers (e.g. Brookfield preferreds will likely pay dividends in your lifetime and mine). People, however, do get confused on the “stopped paying out” part of preferred shares vs. them losing market value – the preferred share trading today at 6% might look good to leverage up money at 2.2%, but if those preferred shares start trading at 7% or 8%, you might be the unwilling recipient of a margin call or the margin calls of others.

To conclude, just because an investment looks good on an absolute basis doesn’t mean the research stops there before hitting the buy button – making comparative measurements is just as important. Nothing precludes one from buying into both options; after all, if there is no correlation between the two investments and your success rate is 70%, you’ll hit your target on at least one investment half of the time.