I’d like to thank Larry MacDonald for mentioning me on his regular article on the Globe and Mail about short selling on the TSX.

A hedge-fund analyst once sold short a company in which Sacha Peter had invested. Then he published a critique on it.

Did Mr. Peter, author of the Divestor blog, rush to his keyboard to click on the sell button, or log into online forums to urge a squeeze on the short seller? Not at all.

Instead, he rolled up his sleeves and dived into the critique. After reading it, the shares remained in his portfolio and were later unloaded at a profit.

It may not always turn out as well as it did for Mr. Peter, but there is something to be said for monitoring the trades of short sellers to see if any are targeting a stock you hold. As Mr. Peter says, “I very much like reading the short-sale cases of anything I hold. It forces me to check my analysis.”

Larry was referencing my post back in April 2018, The case to short Genworth MI, where a very intelligent young analyst won an accolade for writing a fairly comprehensive short report on Genworth MI.

Keep in mind there is no “one size fits all” strategy concerning how one deals with new information that comes with people or institutions issuing short selling reports on your holdings. Everything depends on your ability to perceive fact from fiction, and perhaps more maddeningly, perceive the market’s sense of reality versus fiction that they bake into the stock price.

I’ll also talk about a time where I got things less correct.

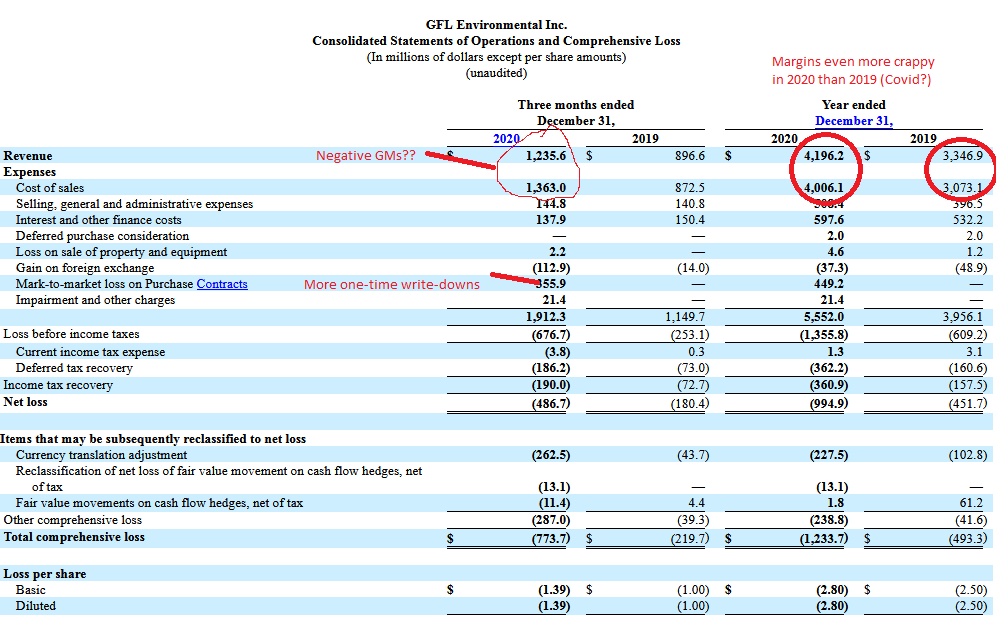

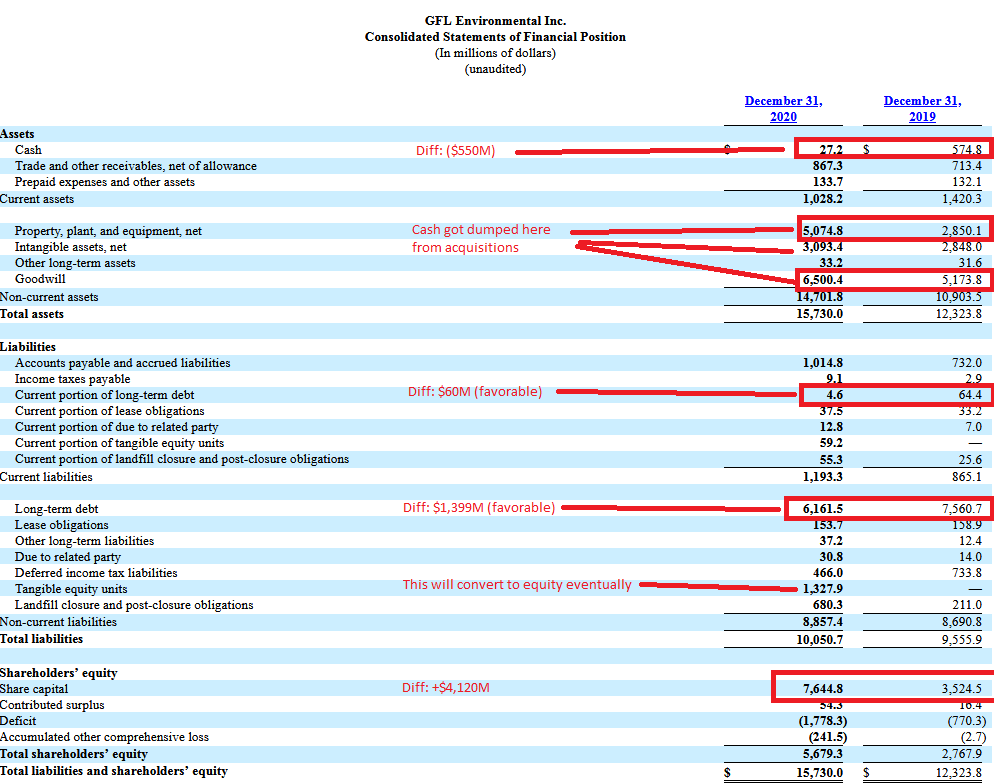

Go read my August 2020 post on what happened when a short selling firm released a report on GFL Environmental. I had taken a small position on one of their hybrid securities (effectively yield-bearing preferred equity with equity price exposure above and below a certain GFL price range) and then a short sale report came out. I bailed very quickly. Retrospect has shown that wasn’t a good decision financially (right now GFLU is about 70% above what I sold it for including dividends), but one of the reasons for bailing was because I was not nearly as comfortable with my level of knowledge about the company than I was about Genworth MI. Another reason is that there were still very active market reverberations going on during COVID-19 so there were plenty of alternate investment candidates for my capital. I’d also like to give a hat tip to Jason Senensky of Chapter 12 Capital for his comment that has stuck in my mind ever since, which is his insightful analysis that my “return on brain damage is too low” – which indeed is an accurate reflection that my mental bandwidth on such cases is better spent elsewhere.

And while I’m on this topic, Jason also wrote a fantastic article on the near-demise of Home Capital Group, instigated by a high profile short seller. Hindsight is 20/20, but I feel like there was a missed opportunity on that one – I should have taken the cue after they announced they obtained their ultra-expensive secured line of credit facility (it marked the bottom of their share price).