I wrote about Just Energy (TSX: JE) last December after they suspended their preferred share dividends and were obviously awaiting a recapitalization.

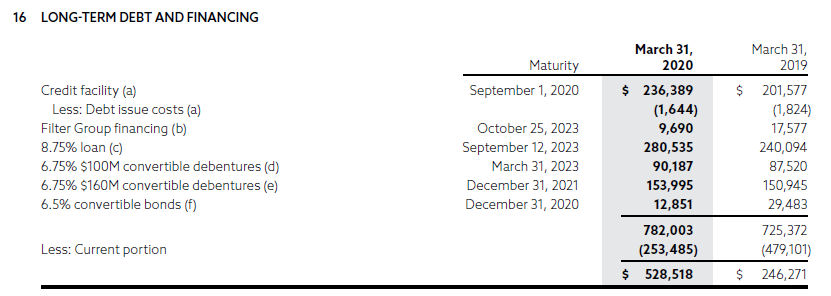

A memory refresher on their debt structure:

A couple days ago the proposal came out.

Given all of the classes of debt, this is a messy proposal to read through all the relevant terms. It involves a debt/preferred share conversion, a 33:1 reverse split, and then a follow-on offering of equity.

* Exchange of C$100 million 6.75% subordinated convertible debentures due March 31, 2023 (TSX: JE.DB.D) and C$160 million 6.75% subordinated convertible debentures due December 31, 2021 (TSX: JE.DB.C) (the “Subordinated Convertible Debentures”) for new common equity;

* Extension of C$335 million credit facilities by three years to December 2023, with revised covenants and a schedule of commitment reductions throughout the term;

* Existing senior unsecured term loan due September 12, 2023 (the “Existing Term Loan”) and the remaining convertible bonds due December 31, 2020 (the “Eurobond”) shall be exchanged for a New Term Loan due March 2024 with initial interest to be paid-in-kind and new common equity;

* Exchange of all 8.50%, fixed-to-floating rate, cumulative, redeemable, perpetual preferred shares (JE.PR.U) (the “Preferred Shares) into new common equity;

* New cash equity investment commitment of C$100 million;

* Initial reduction of annual cash interest expense by approximately C$45 million; and

* Business as usual for employees, customers and suppliers enhanced by the relationship with a financially stronger Just Energy – they will not be affected by the Recapitalization.In total, the Recapitalization will result in a reduction of approximately C$535 million in net debt and preferred shares.

Translated:

1. Convert C$260 million of convertible debt into equity

2. Convert US$117 million par of preferred shares = ~CAD$160 million in equity

3. Add CAD$100 million in equity financing

4. Convert ~CAD$15 million in the “Eurobond” to equity

This is where they get the bulk of the CAD$535 million figure from – from the publicly traded JE.DB.C/D and JE.PR.U securities.

None of the other tranches of debt receive a haircut – instead, they get extended. I will note that the holders of debt is that is the (unlisted) US$207 million unsecured term loan receives relatively preferential treatment in this recapitalization. The likely reasons for this: “The US$14 million draws were secured by a personal guarantee from a director of the

Company.”, and the fact that this tranche of debt was loaned from Sagard Credit, who is backstopping the equity offering.

The CAD$260 convertible debentures will be converted into 56.7% of the equity of the company, prior to the CAD$100 million equity financing.

JE this second is trading at 49 cents per share. At their existing market cap, JE equity is valued at $74.3 million. Convertible debt holders are being asked to convert CAD$260 million into $42 million of pre-diluted equity. This would also explain why the debentures presently are trading at about 18 cents on the dollar.

Preferred shareholders receive 9.5%, and this works out to 4.4 cents on the dollar. This class of shareholder is lucky to get anything.

The common shareholders will retain 28.8% of the company, and they should be even luckier to hold onto anything.

The convertible debentures are subordinated unsecured obligations of the company, which means that they are the lowest tranche of debt in the pecking order. However, the convertible debentures upon maturity can be converted into shares of JE with a standard VWAP clause:

The Corporation may, at its option, on not more than 60 days and not less than 30 days prior notice, subject to applicable regulatory approval and provided no Event of Default has occurred and is continuing, elect to satisfy its obligation to repay all or any portion of the principal amount of the Debentures that are to be redeemed or that are to mature, by issuing and delivering to the holders thereof that number of freely tradeable Common Shares determined by dividing the principal amount of the Debentures being repaid by 95% of the Current Market Price on the date of redemption or maturity, as applicable.

Presumably, if the convertible debentures were allowed to be exchanged for shares under this formula they would be receiving more than 56.7% of the pre-diluted equity. This is not allowed to happen because the senior creditors (the facility due on September 1, 2020) want to squeeze them out for a lot less.

This is what I’d call a fairly “unjust” recapitalization of Just. Caveat Emptor for those that were holding onto any of these securities! In particular, the purchasers of the February 22, 2018 offering of the 6.75% convertible debentures have realized an approximate 70% loss in their investment over the 2 years they’ve been holding it, which is fairly impressive.

No positions, never had any, do not intend on taking any either, and also commend management for ruthlessly taking out more retail capital – this is a textbook case.

Am I crazy to think that the equity might be interesting once the recap is done?

Shitty business, but if theyre able to do 100+ millions in EBITDA as theyve guided, this is some serious cash flow.

Nothing prevents you from buying the common right now if that’s the case… EBITDA is easy to generate if you just make lots of capital expenditures to generate a little return and then amortize an excess amount. Both fiscal 2019 and 2020 were lacklustre to say the least.

I’m thinking JE should have hired whoever did the Cineplex deal, that would have solved the problem!

Yep, that deal is something else. I wonder who’s buying the convertible… 5.75% seems awfully low for a business who might have to go under CCAA to survive.

I rolled the dice on this one and got snake eyes.

I understand how the debentures can be converted into common shares at maturity, but I’m a little confused as to how they’re converting the preferreds. I’ve read through the prospectus and the redemption process seems to require that JE pay out the face value. There doesn’t appear to be a stipulation that they can convert the preferreds into common shares like there is in other preferred prospectuses that I’ve read. For instance, one class of Bombardier preferred explicitly states that the company can convert the preferreds at their discretion.

The company essentially puts a gun to your (preferred shareholder) head and says take the deal (a 9.5% equity stake conversion) otherwise the alternative is that we will CCAA you and you will likely end up with zero.

What are the chances of a successful revolt from conv. debenture holders? It seems they get shaft very badly considering how much the common holders are getting.

The math is pretty simple, let’s just pretend a full-fledged CCAA process will suck up about $100 million in consulting, legal and operating losses by the time it resolves. If you think in a protracted CCAA you can get more than roughly ~$750 million out of this stone then it’d make sense to vote against the arrangement. Converts are sitting behind roughly $540 million of more senior debt right now, plus whatever priority small claims (e.g. payroll, small suppliers) on the books. Other than the senior debt, these figures are very rough and approximate.

[…] regards to Just Energy (TSX: JE), after a suspenseful suspension of the recapitalization proposal meeting, a couple days later an agreement with substantially most of the shareholders and debtholders was […]

Here is a recent excerpt from Canaccord’s investment in Just Energy. How does this match with what you’ve written above? I fail to see how anyone who purchased at part in 2016 expects to come close to recovering all their capital?? Thoughts?

___________________________________________________________

Recent Example of a Complete Corporate Restructuring and Recapitalization: Just Energy 6.75% 31DEC21

In October 2016 we initiated a position in the Just Energy 6.75% 31DEC21 convertible debenture at par value “100.00”. On June 30th, 2019 this “busted convert” closed at “99.90” – just as the company initiated a “sales process” in an effort seeking to maximize shareholder value. Concurrently, the company started to “clean-up” and rationalize its operations – supposedly in an effort to make the company more attractive to a potential buyer. After failing to find an “acceptable bid” for the company, Just Energy announced a comprehensive reorganization and recapitalization plan on July 8th, 2020 which included the conversion of $420 million of debt and preferred shares (including our convert position) to equity, and a $100 million recapitalization via a Rights Offering, which was made available to investors in all parts of the capital structure. The converts subsequently traded down to a “disconnected” 12 cents on the dollar in August (a price of “12.00”), and the recapitalization and reorganization was finalized on September 28th , 2020. The result of these changes was that the company’s original shareholders saw their ownership stake significantly diluted – and convertible debenture holders, which were paid interest right up until September 28th, 2020, were put in a position to fully recover their capital – assuming they took advantage of the company’s recapitalization Rights Offering made available to them.

On our end, we did take full advantage of the Rights Offering – and expect to end-up with a full recovery on our invested capital – and realize a significant positive return on this investment. At the time of publishing this report we have not yet sold or reduced our new equity position in the company.

I am going to let smarter people than myself figure out this one. The rights offering was offered to those holding onto it in July 23, 2020 and at C$3.412, but quite frankly, I’m not that interested in doing the math. Good for them for dredging out blood from that stone!