An annoyance of mine in the oil and gas space is the action of management hedging against changes in commodity prices. They engage in this activity for various reasons. A valid reason is if there is a financial threat that would be caused by an adverse price move (e.g. blowing a financial covenant is something to be avoided). A not-so-valid reason is “because we have done so historically and will continue to do so”. An even less valid reason is “I’m gambling!” – that’s my job, the job of the oil and gas producer is to figure out the best way to pull it out of the ground!

One additional problem with hedging is that you will get ripped off by Goldman Sachs and the like when they place positions. Your order will always be used against you. There are always frictional expenses to getting what is effectively a high cost insurance policy.

Such policies look great in a dropping commodity environment, but in a rising environment they consume a ton of opportunity cost to maintain. For example, in the second half of last decade, Pengrowth Energy managed to stave off its own demise a year later than it otherwise should have because it executed on some very well-timed hedges before the price of oil collapsed. Incidentally, the CEO of Pengrowth back then is the CEO today of MEG Energy (TSX: MEG).

MEG Energy notably gutted its hedging program after 2021 concluded. They lost $657 million on that year’s hedging program, just over $2/share.

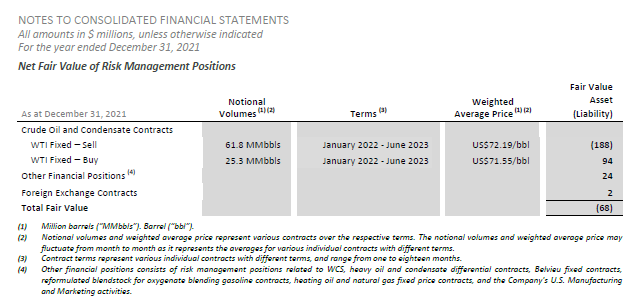

Let’s take another example, Cenovus Energy. I have consistently not been a fan of Cenovus Energy’s hedging policies, especially since it is abundantly clear that they will have been able to execute on their deleveraging. In their Q4-2021 annual report, digging into their financial statements, you have the following hedges:

For those needing help on their math, if you ignore the minor price differential between the buy and sell, it is approximately 66,666 barrels per day that is pre-sold at US$72, up until June 2023.

As I write this, spot oil is US$103. That’s about $1.1 billion down the tubes.

So today, Cenovus fessed up and said they’ve blown a gigantic amount of money on this very expensive insurance policy:

Realized losses on all risk management positions for the three months ending March 31, 2022 are expected to be about $970 million. Actual realizations for the first quarter of 2022 will be reported with Cenovus’s first-quarter results. Based on forward prices as of March 31, 2022, estimated realized losses on all risk management positions for the three months ending June 30, 2022 are currently expected to be about $410 million. Actual gains or losses resulting from these positions will depend on market prices or rates, as applicable, at the time each such position is settled. Cenovus plans to close the bulk of its outstanding crude oil price risk management positions related to WTI over the next two months and expects to have no significant financial exposure to these positions beyond the second quarter of 2022.

As this hedging information was already visible, the amount of loss can be reasonably calculated, so the actual loss itself isn’t much of a surprise to the market. The forward information is they’re reversing the program.

However, even if they did not, an investor can still reverse their decision in their own portfolio, using exactly the same West Texas Intermediate crude oil contracts that Goldman and the like will use. As an investor, you can take control in your own hands the level of hedging that an oil/gas producer takes.

For instance, using the above example, it works out to 2 million barrels of oil a month (net of sales and purchases) that is being hedged. Note each futures contract is good for 1,000 barrels of oil.

If you owned 100% of Cenovus Energy, you could sell 2,000 contracts of each month between the January 2022 to June 2023 WTI complex. Obviously you wouldn’t want to hammer such a size in a two second market order, but there is enough liquidity to reasonably execute the trade.

I don’t own 100% of Cenovus, but the same principle applies whether you own 10%, 1%, or whatever fractional holding of the company – you just reduce the proportion of the hedge.

The only impractical issue to this method is the 1,000 barrel size per futures contract sets a hefty minimum. You need institutional size in this particular case. For instance, just one futures contract sold across January 2022 to June 2023 would correlate with the ownership of approximately 1,000,000 shares of Cenovus Energy. Anything more than this and it would be positive speculation on the oil price (which is what one implicitly does when investing in such companies to begin with!).

The same principle applies for companies that do not employ the desired amount of leverage (debt to equity) in their operation. Assuming your cost of financing is the same as the company (this factors in interest, taxes, covenants, etc.), there is no theoretical difference between the company taking out debt versus you buying shares of the company on margin to achieve the desired financial leverage ratio.

Going to back to crude oil, deciding to un-hedge only works when you assume there is a rising commodity price environment. Management’s actions, no matter which ones they take, are implicitly a form of speculation on future prices and if you disagree – if for whatever reason you don’t want to sell the company outright (e.g. continuing to defer an unrealized capital gain) you can always hedge yourself by going short those crude futures. The power is always in your hands as an investor!