Corus Entertainment (TSX: CJR.B) is a well known company. They have various media assets in Canada on television and radio. At one point I was considering a purchase, but held back because they are highly leveraged and I didn’t have a solid grasp on the risk/reward profile – I suspect they do have competitive advantages but the broadcasting industry is shifting so much (“cord-cutting”, Netflix, etc.) it is difficult to tell whether it is sustainable.

Reading their year-end financial statements, there are a few interesting wrinkles which caught my attention.

0. Fiscal year ends August.

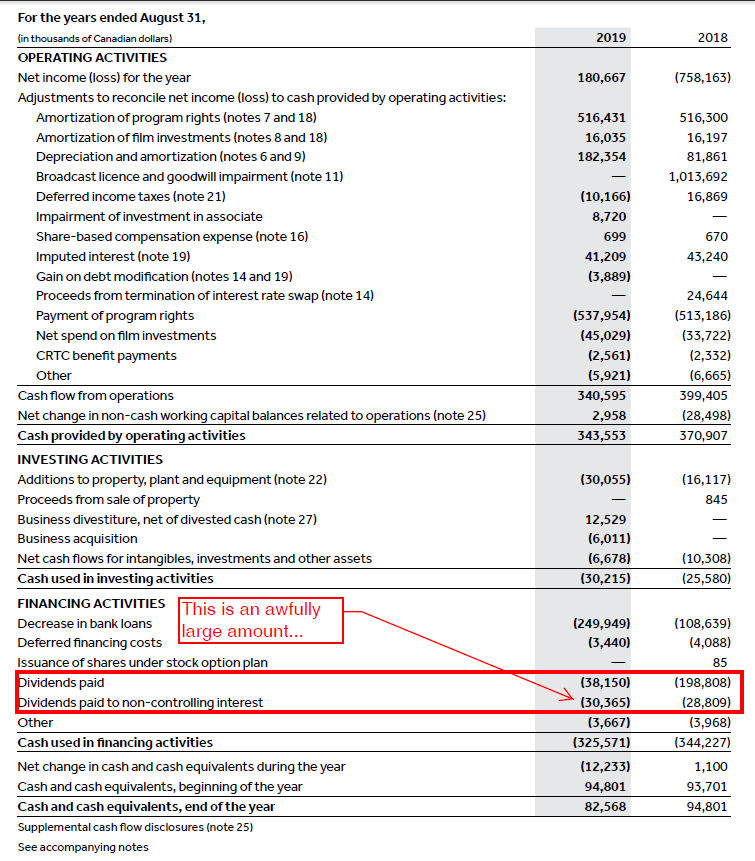

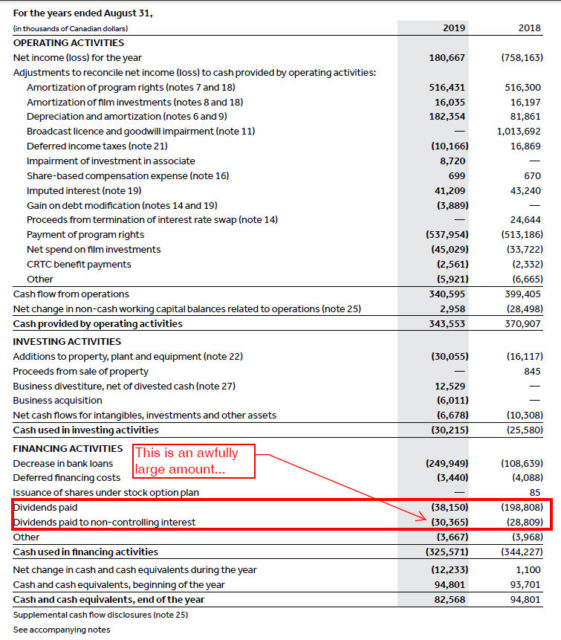

1. They historically have generated a lot of cash. FCF in FY2018 was $344 million, and $307 million in 2019. In 2019, they chipped away $250 million on their debt (which stood at a FY year end balance $1,732 million). Most of this debt was issued to facilitate the acquisition of Shaw Media. $258 million is due November 2021, $869 million on May 2023 and $639 million on May 2024. Clearly they won’t stand much of a chance of paying back the 2023 and 2024 tranches, but one would presume if they rake in $300 million a year in free cash, this won’t be a problem to refinance. The effective rate on the debt is 4.3%.

If for whatever reason this future operating cash flow were to drop at a more accelerated pace, however, the equity is going to suffer badly.

But needless to say if one believes that $300 million is the norm, $1.42/share in cash means the Class B shares trade at a 3.5x multiple…

2. The amount of dividends issued is structured in a peculiar manner:

Corus slashed their dividend 80% last year so they can concentrate their capital on deleveraging. However, the amount of dividends going to non-controlling interests is quite high.

The concept of non-controlling interests is not easy to explain in accounting terms, so I will try here.

Let’s pretend you own a holding company, but this company’s only asset is the ownership of 70% of voting and common shares of an operating entity. If the operating entity makes $100 of income, you consolidate the operating company’s financial statements into your own, but $30 of that income is attributable to non-controlling interests. Shareholders of the holding company effectively only “see” 70% of the operating company’s income.

This is most prominent in a case like Interactive Brokers (Nasdaq: IBKR) where a shareholder of IBKR (76.7 million shares outstanding) owns 18.5% of IBG LLC, which is the entity that actually owns most of the assets. In the 3 months ended June 2019, for example, IBG LLC reported $210 million in net income, but $178 million goes to non-controlling interests (the 81.5% that owns IBG LLC, mainly Thomas Petterfy) while IBKR holders effectively see $32 million. Indeed, IBKR holders will only be able to “cash in” if IBG LLC is generous enough to distribute earnings to it (which they do through a nominal dividend, and control is not an issue because the entity has the same controlling shareholders).

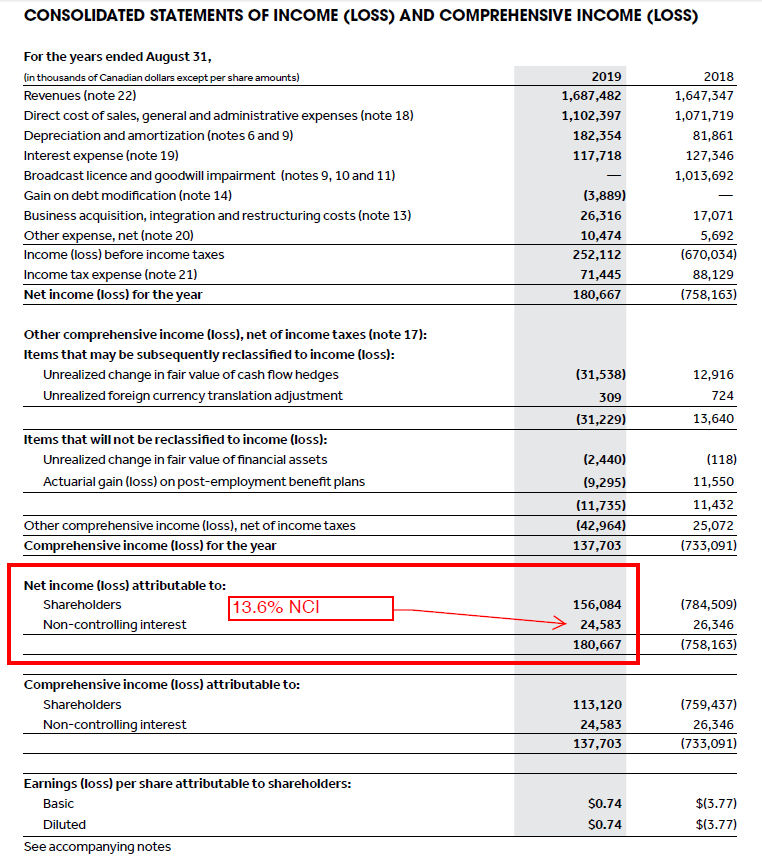

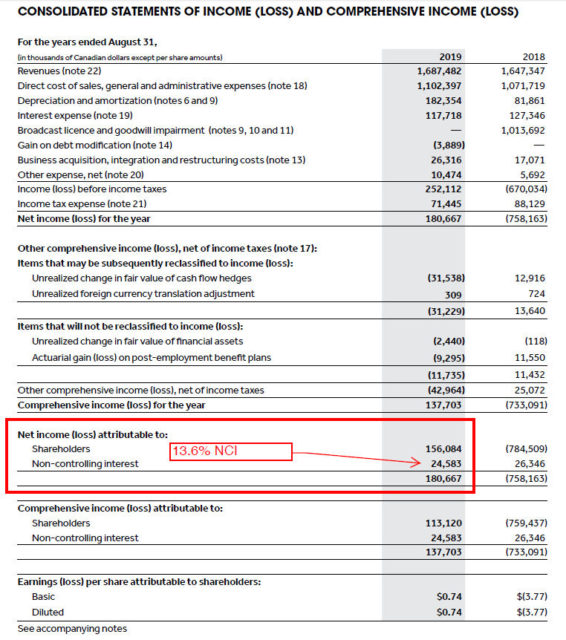

Indeed, when we look at Corus’ income statement, we see that various entities contribute a 13.6% slice on net income:

So one obvious question is the following: what is the agreement governing the non-controlling interest and Corus? It appears that the non-controlling interest has favourable agreements with respect to cash distribution than common shareholders. What entitles these non-controlling interests a $30 million slice of income each year when common shareholders get 56% of the dividends paid by Corus?

I haven’t been able to figure this out.

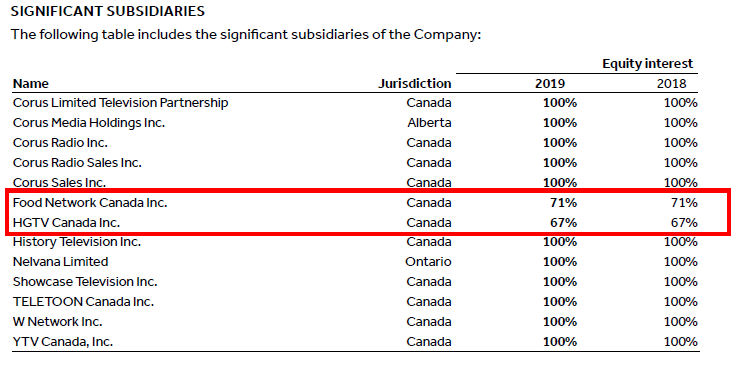

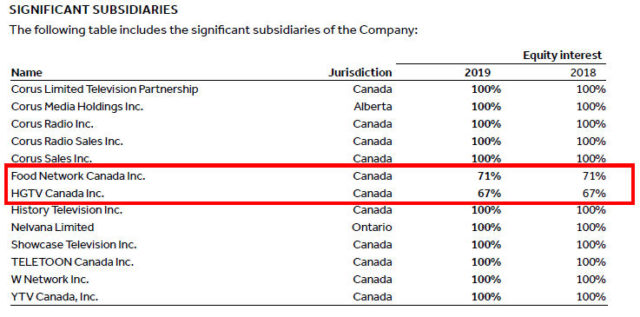

However, on page 51 of their financial statements, we have the list of subsidiaries, and the non-controlling interest must come from these entities:

I never knew the Food Network and HGTV was so profitable!

What sort of agreements are stripping so much value away from common shareholders? I tried looking into the MD&A and AIF, but couldn’t find any relevant answers.

3. Here is the biggest issue I have with Corus – alignment of interests.

Shaw used to own 38% of the non-voting Class B shares of the company (the only shares which are publicly traded). They dumped this stake for CAD$6.80/share on May 31, 2019. However, the Shaw family trust still owns 85% of the Class A voting shares (3,412,392 shares outstanding) which means they have an economic stake in the company of 1.6% but still total control. Now that Shaw is virtually out of Corus, the incentive structure is completely mis-aligned with common shareholders. Right now the 24 cent/year dividend is the only thing they have going for it. One wonders what sort of value-stripping agreements might take place in the future (similar to my suspicions on the relatively high cash drain coming from non-controlling interests – where is this value going?).

It is one thing if the controlling shareholder has a significant economic interest in the firm they are leading (e.g. one would suspect that Genworth Financial is not going to take actions that will hurt the economics of the underlying Genworth MI entity). It is completely another thing if somebody has control but no economic interest – this sort of alignment asks for common shareholders to get the short end of the stick.

If anybody has answers on this one, or if I’m completely out to lunch, I’d like to know.