Corus Entertainment (TSX: CJR.B) has been a slow melting cube business case, dealing with the woes of competing against Netflix and streaming media, and the internet in general. Despite these competitive factors, they have still been able to generate a prodigious amount of cash flows.

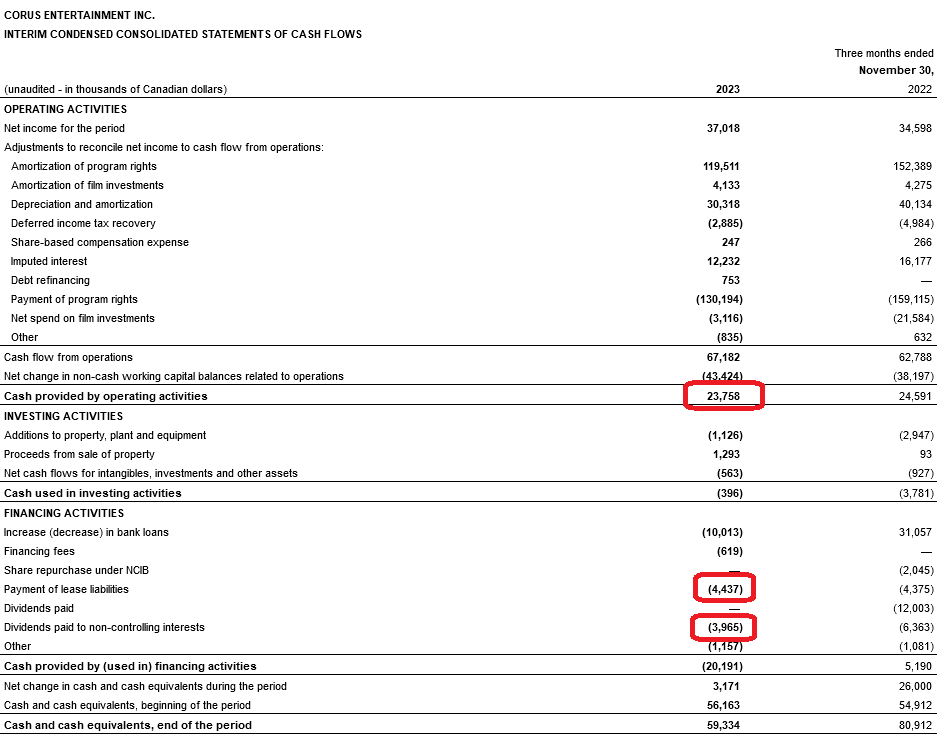

They released their fiscal quarter results on January 12, 2024 and the following was their quarterly cash flow statement:

I’ve circled some relevant numbers. The key parts are that they have huge capital requirements to acquire program rights (this part makes the EBITDA look very attractive!) but these costs are necessary and increasing; they also have non-controlling interests which get claims to dividends that ordinary shareholders do not receive.

When netting this out, you have about $15 million in effective cash to work with. Management has a very strange interpretation of “free cash flow” which I won’t get into here.

This effective cash is contrasted to the $1.08 billion debt they have. Management is very fortunate to have $750 million of this at much lower fixed rates (5% and 6%) due 2028 and 2030 (the rest of it is in a credit facility) but needless to say, this leverage coupled with non-controlling interests do not leave the prospect of equity returns to be very good given the melting ice cube. The fixed rate debt is traded on the open market at a 13% yield to maturity at present.

There is some residual clout in ‘traditional media’ and Corus does still reach a lot of television sets and radios across the country. Perhaps some deep-pocketed individual will want to take control for strategic/political and not necessarily financial reasons.

The entity does appear to be more viable if they got rid of about half their debt.