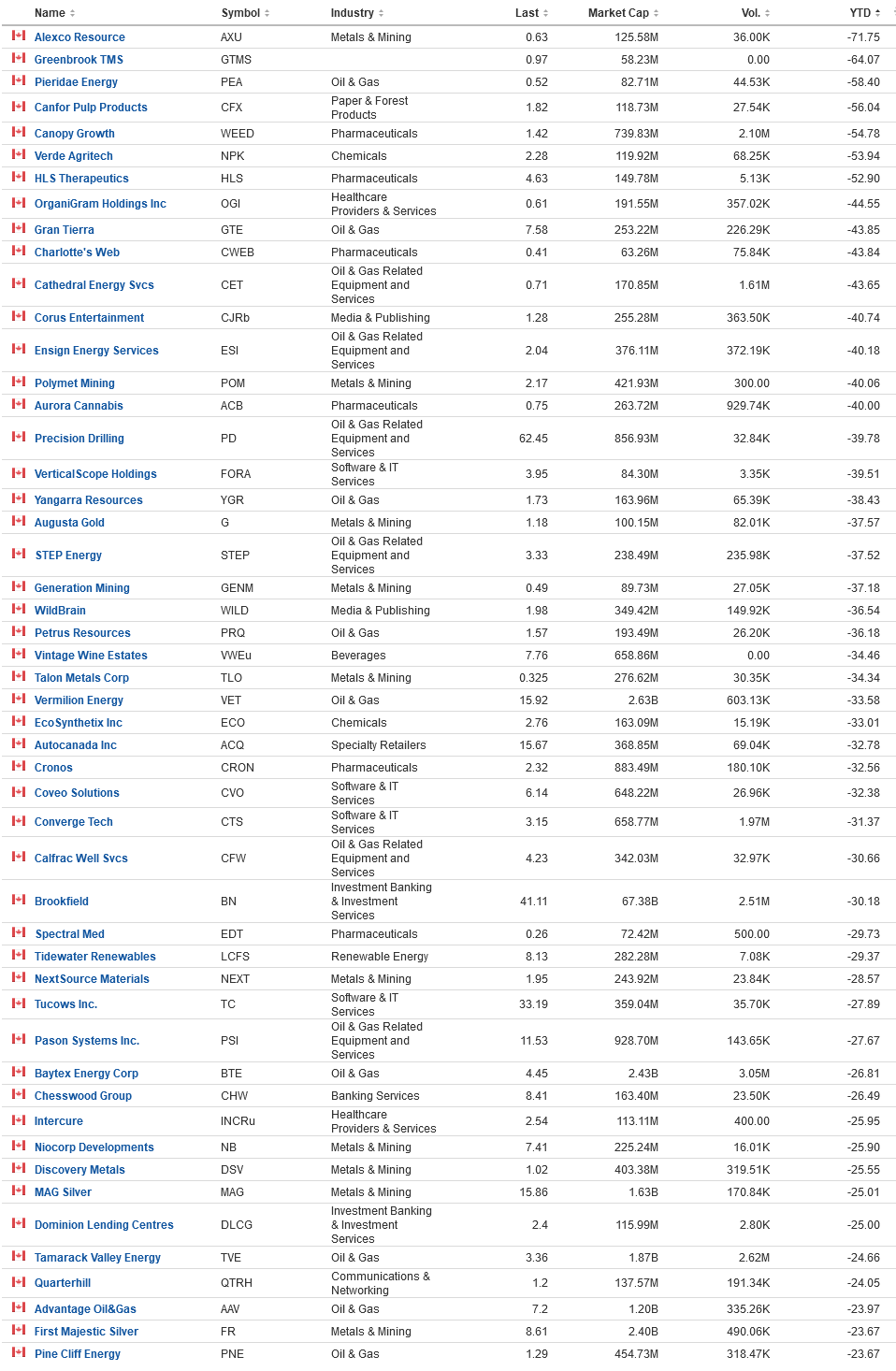

Rank ordering year-to-date, losers on the TSX, with a minimum market cap of $50 million:

What strikes out at me?

Canfor Pulp (CFX) – What a miserable industry pulp and paper has been over the past four years. Their profitability last decade has been quite good, and then 2019 hit and that was it. Now they are closing down core assets in British Columbia (their Prince George mill is a considerable producer). Most of their production is destined for export to Asia and the USA, and if there is ever a poster child for how BC is a high-cost jurisdiction to conduct forestry, this one is it. CFP owns 55% of CFX. Contrast this with Cascades (TSX: CAS) which the common stock continues its usual range-bound meandering (remember – they were one of the prime recipients of demand for toilet paper during the onset of Covid-19!). If there is any sense of regression to the mean on CFX, however, it would be a multi-bagger stock. The question would be – when? Solvency is not too particular a concern – they’ve got their lines of credit extended out sufficiently.

Verde Agritech (NPK) – A foreign fertilizer firm, notably one of their board members got cleared out of half of his position in the company on April 24th on a margin call. I have no other comments on this other than my professed non-knowledge about Potash and the fertilizer industry. I note that Nutrien (NTR) has been trending down for over a year.

Corus Entertainment (CJR.b) – They cut their dividend, and are realizing that their degree of financial leverage is really going to hurt their cash generation, especially in an industry that is becoming more and more questionable for advertising revenues (broadcast television). The risk here is obvious.

VerticalScope (FORA) – How they managed to get over a half-billion valuation when they went public is beyond me. Rode the 2021 “web 3.0” bubble for the maximum (right there with Farmer’s Edge and the like). Given the organic business is marginally profitable and unscalable at best, and given their existing debt-load, good luck!

Vintage Wine (VWE) – This is a US/Nasdaq entity, I don’t know why this went on the TSX screen, but I checked it out anyway. Sales issues (declining), cost containment, and a large amount of debt plague this company. However, if you shop around any of their wineries, they do offer a “Platinum Shareholder Passport“, where if you own 1000 shares (which is now US$1.08/share, not too steep), you qualify for “25% discount on any wine purchase made at Vintage wineries and web stores.”, which quite possibly might be even larger than a $1,080 investment, depending on how much wine you end up buying. Now that’s a non-taxable dividend you can drink to!

Autocanada (ACQ) – How the mighty have fallen. After blowing a considerable amount of capital on share buybacks (the latest substantial issuer bid at $28 – stock is now $16) in 2022, they are finally feeling the pinch of margin erosion, especially from their last quarterly report. There are macroeconomic headwinds in place here, in addition to a not inconsiderable amount of debt. On their balance sheet, they did something smart by financing a $350 million senior unsecured note financing in early 2022 at 5.75% at a 7-year maturity, but there is still $1.2 billion in other floating rate debt on the books, which needless to say is getting very expensive. Even worse yet is the impact when you have to pass these costs onto your customers in financing charges, so suddenly your Land Rover that was a low $799 per two week payment is now $999! At some point, customers walk away and then decide they want a Toyota Corolla, which is also inconveniently unavailable everywhere. See: Gibson’s Paradox.

… a bunch of Oil and Gas drilling companies are on the list. No comment – it is pretty obvious why.

Brookfield (BN) – A surprising name to see on the list. I have a “no investment in entities named Brookfield” policy simply because of complexity. There are so many interrelationships between the various Brookfield entities that I do not want to make it my full-time life to keep appraised with it all.

51 on the list was Aritzia (ATZ) – I have long since given up on predicting women’s retail fashion trends. I note that Lululemon (LULU) is still sky-high in valuation (forward P/E of roughly 30). Victoria’s Secret (VSCO) is trading at a projected P/E of 5. Aritzia has kept a relatively decent balance sheet (only material liabilities is the retail leases they have committed to) and the projected multiple is 20. If you can get into the minds of the clientele, you would probably get more visibility on the future sales of this company. How do institutions do it? Should I go stick out like a sore thumb and go outlet mall shopping?

Anything else strike out at you?