I wrote about Just Energy (TSX: JE) last December after they suspended their preferred share dividends and were obviously awaiting a recapitalization.

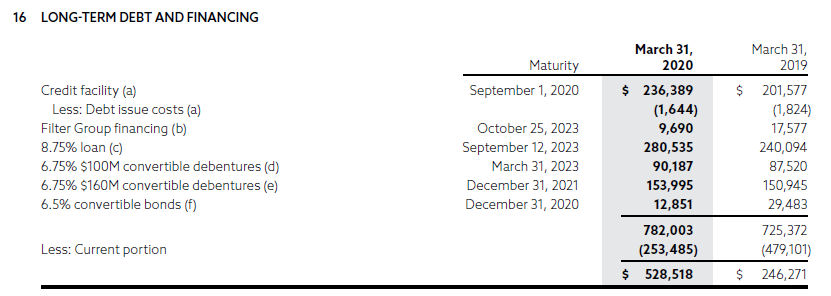

A memory refresher on their debt structure:

A couple days ago the proposal came out.

Given all of the classes of debt, this is a messy proposal to read through all the relevant terms. It involves a debt/preferred share conversion, a 33:1 reverse split, and then a follow-on offering of equity.

* Exchange of C$100 million 6.75% subordinated convertible debentures due March 31, 2023 (TSX: JE.DB.D) and C$160 million 6.75% subordinated convertible debentures due December 31, 2021 (TSX: JE.DB.C) (the “Subordinated Convertible Debentures”) for new common equity;

* Extension of C$335 million credit facilities by three years to December 2023, with revised covenants and a schedule of commitment reductions throughout the term;

* Existing senior unsecured term loan due September 12, 2023 (the “Existing Term Loan”) and the remaining convertible bonds due December 31, 2020 (the “Eurobond”) shall be exchanged for a New Term Loan due March 2024 with initial interest to be paid-in-kind and new common equity;

* Exchange of all 8.50%, fixed-to-floating rate, cumulative, redeemable, perpetual preferred shares (JE.PR.U) (the “Preferred Shares) into new common equity;

* New cash equity investment commitment of C$100 million;

* Initial reduction of annual cash interest expense by approximately C$45 million; and

* Business as usual for employees, customers and suppliers enhanced by the relationship with a financially stronger Just Energy – they will not be affected by the Recapitalization.In total, the Recapitalization will result in a reduction of approximately C$535 million in net debt and preferred shares.

Translated:

1. Convert C$260 million of convertible debt into equity

2. Convert US$117 million par of preferred shares = ~CAD$160 million in equity

3. Add CAD$100 million in equity financing

4. Convert ~CAD$15 million in the “Eurobond” to equity

This is where they get the bulk of the CAD$535 million figure from – from the publicly traded JE.DB.C/D and JE.PR.U securities.

None of the other tranches of debt receive a haircut – instead, they get extended. I will note that the holders of debt is that is the (unlisted) US$207 million unsecured term loan receives relatively preferential treatment in this recapitalization. The likely reasons for this: “The US$14 million draws were secured by a personal guarantee from a director of the

Company.”, and the fact that this tranche of debt was loaned from Sagard Credit, who is backstopping the equity offering.

The CAD$260 convertible debentures will be converted into 56.7% of the equity of the company, prior to the CAD$100 million equity financing.

JE this second is trading at 49 cents per share. At their existing market cap, JE equity is valued at $74.3 million. Convertible debt holders are being asked to convert CAD$260 million into $42 million of pre-diluted equity. This would also explain why the debentures presently are trading at about 18 cents on the dollar.

Preferred shareholders receive 9.5%, and this works out to 4.4 cents on the dollar. This class of shareholder is lucky to get anything.

The common shareholders will retain 28.8% of the company, and they should be even luckier to hold onto anything.

The convertible debentures are subordinated unsecured obligations of the company, which means that they are the lowest tranche of debt in the pecking order. However, the convertible debentures upon maturity can be converted into shares of JE with a standard VWAP clause:

The Corporation may, at its option, on not more than 60 days and not less than 30 days prior notice, subject to applicable regulatory approval and provided no Event of Default has occurred and is continuing, elect to satisfy its obligation to repay all or any portion of the principal amount of the Debentures that are to be redeemed or that are to mature, by issuing and delivering to the holders thereof that number of freely tradeable Common Shares determined by dividing the principal amount of the Debentures being repaid by 95% of the Current Market Price on the date of redemption or maturity, as applicable.

Presumably, if the convertible debentures were allowed to be exchanged for shares under this formula they would be receiving more than 56.7% of the pre-diluted equity. This is not allowed to happen because the senior creditors (the facility due on September 1, 2020) want to squeeze them out for a lot less.

This is what I’d call a fairly “unjust” recapitalization of Just. Caveat Emptor for those that were holding onto any of these securities! In particular, the purchasers of the February 22, 2018 offering of the 6.75% convertible debentures have realized an approximate 70% loss in their investment over the 2 years they’ve been holding it, which is fairly impressive.

No positions, never had any, do not intend on taking any either, and also commend management for ruthlessly taking out more retail capital – this is a textbook case.