If you were holding preferred shares in Just Energy (TSX: JE.PR.U), you don’t want to be reading this announcement:

Just Energy Group Inc. (“Just Energy” or the “Company”) (TSX:JE) (NYSE:JE) announced today that it has amended its senior secured credit facility to increase the senior debt to EBITDA covenant ratio from 1.50:1 to 2.00:1 for the third quarter of Fiscal 2020. In addition, the Company has amended the covenants on its senior unsecured term loan facility to increase the senior debt to EBITDA covenant ratio from 1.65:1 to 2.15:1 for the third quarter of Fiscal 2020. Both changes are effective only for the third quarter of Fiscal 2020 and the covenants will revert to the prior levels following December 31, 2019.

In connection with the amendments, the agreements governing both facilities have been changed to restrict the declaration and payment of dividends on the Company’s 8.50% Series A Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Shares (“Series A Preferred Shares”) until the Company’s senior debt to EBITDA ratio is no more than 1.50:1 for two consecutive fiscal quarters. Accordingly, the Company is suspending, with immediate effect, the declaration and payment of dividends on the Series A Preferred Shares until the Company is permitted to declare and pay dividends under the agreements governing its facilities. However, dividends on the Series A Preferred Shares will continue to accrue in accordance with Series A Preferred Share terms during the period in which dividends are suspended.

Preferred shares proceeded to trade from $17 the day before to closing at $9.88, a 42% drop. The common stock, which paid out its last dividend in June 2019, traded down about 16%.

I did remark about Just Energy on September 1, 2019 that “Balance sheet is a train wreck, company is exploring a recapitalization, and the business model itself is highly broken. Good luck!”, but specifically, their big problem is this:

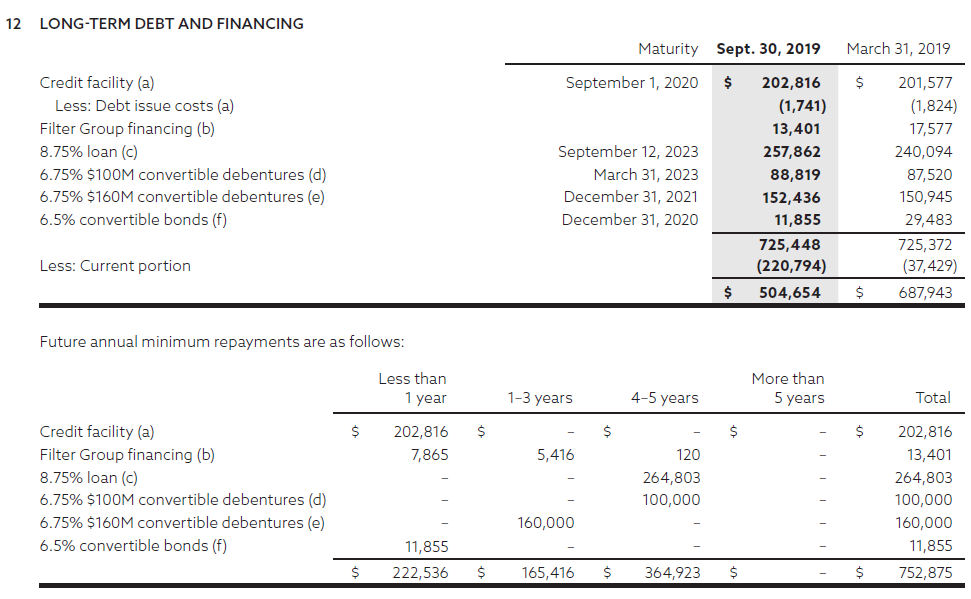

About $222 million is due for refinancing in the year 2020, with the lion’s share the first-in-line secured credit facility that has $203 outstanding.

It is pretty evident by the covenant amendment that the third quarter expectations (noting that Just Energy has their fiscal year-end on March) is not going to have a good quarter. They’ve bought themselves a little bit of time to negotiate with the senior secured creditors, but suffice to say, this one is trading low on all fronts (common, preferred and debentures) for a good reason – a recapitalization is probably in order.

In general, I’m not shocked that the market was valuing the yield on a financial product of a company that is in such precarious financial condition quite highly; the chase for yield blinds most individuals as the underlying framework as to what makes yields possible – cash flow and no imminent liquidity crises. These sorts of decisions that companies make are relatively foreseeable and why I do not have them in my portfolio.

The convertible debentures (TSX: JE.DB.C, JE.DB.D) came up on my radar today as a result. The company cannot suspend their semi-annual interest payment without it being an event of default, but right now the most likely outcome appears to be an equity conversion, and this is under the assumption they can come to some sort of arrangement to placate their senior secured creditor.

The most interesting part of this all is that the company also has a tranche of unsecured term loan facility (8.75% maturing on September 2023) which is partially guaranteed by a director: “On July 29, 2019, the Company drew US$7.0 million from the second tranche and US$7.0 million from the third tranche. These draws were secured by a personal guarantee from a director of the Company.” – this would certainly give this director an incentive to seeing the company not default on it!

I’m guilty, I was considering to buy JE several times in the past because of juicy dividends, but didn’t like their shady business, never checked their financials though. 🙂

Thanks for update!

Wow! I dodged a bullet – bought in Oct 2018 and sold in Apr 2019 – collected some dividends and got out pretty much at the same price as I got in…

Took a small bite of the 2021 debentures JE.DB.C today.

Gutsy, but that’s what you get paid 32% YTM for… assuming the “M” happens.

What are your thoughts on the Just Energy Preferred shares now? Here are some twitter thoughts on it: https://twitter.com/PythiaR/status/1205171502062194689 They are cutting costs and divesting some assets…

$200 million due in September still gives them a bit of time to work with. The convertible debentures are convertible into equity (95% of market value, noting no floor for share price) so they can deal with that by a very serious dilution of shareholders – if they did it would be preferential to the preferred shareholders.

This is clearly a high risk situation – why wouldn’t the people holding the credit facility just simply refuse to negotiate? Guess there will be more visibility coming after Monday’s report.

Reviewed their quarterly report (ending December 31, 2019), wow. Bled another $50 million cash roughly. Their secured credit facility is now $256 million, and they have a 1.5:1 senior debt/EBITDA covenant which stands to have a good chance of getting triggered when they do year-end.

The big loser here I think is going to be the consortium that gave them the US$250 million unsecured loan. I can’t see the senior secured creditors wanting to cede their ranking without extracting a huge price. The convertible debentures can get equitized and the banks won’t care – in fact, they’d prefer it.

Since the strategic review is expected to be concluded by June of 2020, I dont see how they can covert unsecured debs to equity. Atleast for the series that’s maturing on March 31 2023 as the conversion period is way after 2021. Which would leave this series at an advantage to the one that is maturing next year.

Thoughts? Thanks

The secured lenders are very unlikely to broker a deal that involves only one tranche of unsecured debt. If this doesn’t end up in CCAA, they negotiate a proposal where the unsecured debtholders (both groups) will be left with a little something in exchange for an expedited recapitalization.

I agree with you, from my previous experiences with corporate restructuring senior secured debt don’t care about unsecured obviously as long as they get their money back…. If this goes to bankruptcy… Dont you think that the underlying assets are worth at least the value of debt?

– Also from what I read it seems like all the unsecured debt is ranked pari passu i.e unsecured term and convertible debs. Do you think the same? would you justify 10 cents on a dollar as a good risk to reward ratio for bonds?

Can’t give you a precise answer but if I was the senior secured debtholder, I’d be viewing this one as a recovery less than par. Also they have a huge incentive to lowering the boom when they can – every day, those unsecured debtholders get paid interest… (I know it is accrued and paid out periodically but you get what I’m trying to say).

Thanks for your comments…I was planning to scoop some unsecured bonds at low prices but they seem to be worthless.

I simply cannot understand how commons and preferred shares are holding up here. There are also seems to be new experienced activist investor involved as of sept 2019…I think he made a mistake acquiring commons….they are worth less. I was also wondering if there was a thread for Husky pref’s on this amazing site.!

[…] wrote about Just Energy (TSX: JE) last December after they suspended their preferred share dividends and were obviously awaiting a […]