Bombardier is the company that just keeps on giving scandal after scandal after scandal. I had reported on their Q2-2018 results that things were finally on the upside, the C-series disposition from Airbus was proceeding and hence the cash drain would abate, and they could finally look forward to subsequent cash generation. I expressed that all was well.

Nope!

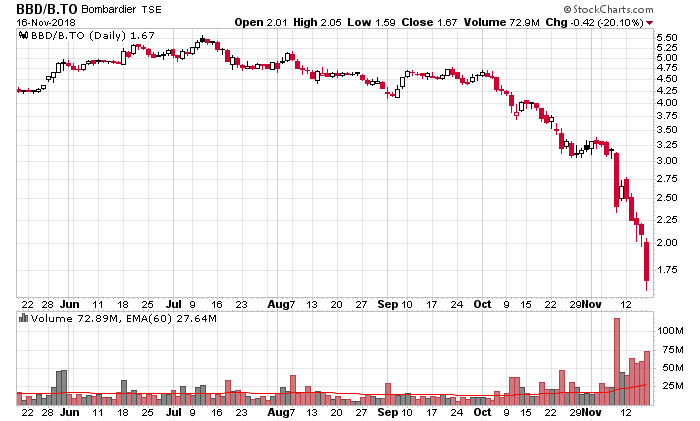

Their Q3-2018 quarterly report wasn’t a complete disaster (but make no mistake: it was a significant deviation from what management was projecting in the previous few quarters), but the market subsequently annihilated everything – shares are down 64% since the beginning of the quarter. Preferred shares are down about 25%. Bond yields are up about 350bps (January 2023s, 6.125% coupon, went from par to about 90 cents on the dollar). I have not seen this amount of market carnage as a reaction to a quarterly report in quite some time.

Then Bombardier announced that the Quebec Securities Commission (Autorité des marchés financiers) will be investigating them for insider trading relating to their automatic share disposition plan. I’m rather ashamed to admit I knew more about the USA version of this (SEC Regulation 10b5-1) compared to the Canadian securities regulations, where Ted Dixon (owner of CanadianInsider.com) writes a very educational article on the matter.

This added further fuel to the selling fire – what the heck did Bombardier executives know on August 15, 2018 that was likely coming down the pipeline? What sort of institutional manager would want to be caught holding shares in such a dysfunctional organization, potentially with unethical executives that were trying to unload their shares at nearly the top? Everybody rushed to the exits and the consequences are pretty obvious.

There are a few reasons why the quarterly report was perceived as horrible other than the inside trading scandal. Indeed, one could infer from the stock price since October that outsider groups knew what the heck was going on.

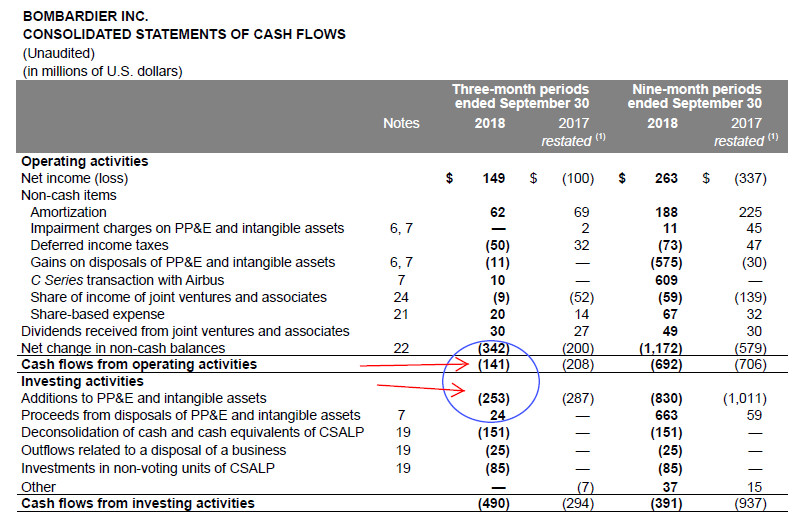

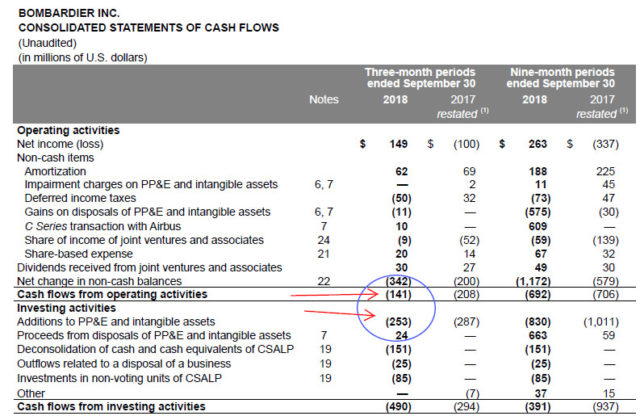

One is that while the company is reporting profit from an accounting perspective ($149 net income for the quarter!), it is burning cash like no tomorrow:

Bombardier’s balance sheet is not in good shape either – while they do have sufficient cash to work with in the next year, their debt maturity profile is looming – US$850 million due March 2020 (this is just 16 months away!) and $2.3 billion in 2021. They will need to become cash positive in order to be able to give the market enough confidence to roll over the debt. In light of them selling off business divisions, it leads one to wonder what is going to be left that will be able to produce such cash.

Finally, what likely set the market most off is this paragraph:

Bombardier is targeting to achieve free cash flow generation in the range of $250 million to $500 million, which is anticipated to be offset by the $250 million restructuring charge mentioned above, as well as a $250 million contingency to reflect the working capital volatility as the Company progresses through its intense growth phase at Business Aircraft and Transportation. Accordingly, free cash flow guidance for 2019 is targeting breakeven plus or minus $250 million.

The market was anticipating a free cash flow generation without any major asset sales, or any “contingency” for “working capital volatility”, or especially any “restructuring charges”. When reading their management discussion and analysis piece, the references to “EBIT minus special items” becomes quite redundant and the market is quite tired of seeing “special items” becoming simply recurring features of the financial statements (which doesn’t make such special items so special – they represent actual costs of business).

What is left of Bombardier (looking at 9 months, ended September 30, 2018 financials):

Business Aircraft – $356 million EBITDA, spent $617 million in capitalized expenses (net these two – this is a $261 million cash burn) – can they actually turn this around and make money?

Commercial Aircraft – Divested the Q-series Turboprops, and sold the C-Series to Airbus – Bombardier is still on the hook for liabilities from the C-Series in 2019 (i.e. a cash burn).

Here is the schedule of payments for the C-Series disposition:

Bombardier will fund the cash shortfalls of CSALP, if required, during the second half of 2018, up to a maximum of $225 million; during 2019, up to a maximum of $350 million; and up to a maximum aggregate amount of $350 million over the following two years, the whole in consideration for non-voting units of CSALP with cumulative annual dividends of 2%. Any excess shortfall during such periods will be shared proportionately amongst the Corporation, Airbus and IQ, but in the latter case, at its discretion. As of September 30, 2018, the Corporation invested $85 million in CSALP in exchange for non-voting units of CSALP. Subsequent to the closing, Airbus rebranded the C Series aircraft as A220.

An $85 million cash drain in the first 9 months of 2018, if repeated in 2019, will result in another $113 million cash going out the window. Is the C-Series going to make money? Wikipedia generally has very good reporting of various aircraft purchase orders (Airbus A220 orders, Boeing 737 MAX orders).

Transportation – $613 million EBITDA, spent $107 in PP&E and intangibles (which I had to manually add from 3 quarterly reports – they don’t give you this number cleanly) – which is a $506 million cash inflow – the only profitable cash source the company has right now.

Complicating matters is that Bombardier sold 30% of their transportation division to the Caisse de dépôt et placement du Québec (for $1.5 billion), but it has an embedded call provision where Bombardier can repurchase its share back in 2019 at a minimum 15% return for the CDPQ. Where will they get the cash?

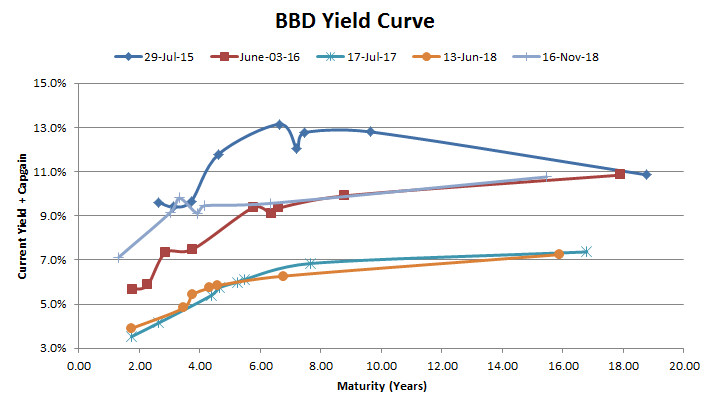

Before, the solution was obvious – float another bond offering, but this market is now on the cusp of being prohibitively expensive:

The near maturity is still at par (roughly 7.75%) but going further on the term structure is going to cost Bombardier significantly – if they decide to do this, it will have to be a secured bond offering.

If you can believe anything management says anymore, they claim 2020 will have $750 to $1,000 million in free cash flow. On the low end of this range would make it about 35 cents per share (noting they have a bunch of warrants outstanding to buy Class B shares at $2.21/share which are no longer in the money). If they can achieve this FCF forecast, then they look awfully cheap.

Of course, the market doesn’t believe them. I don’t either. I do think they will muddle their way through this, as they always have.

The real issue, to summarize, is that Bombardier is facing a classic liquidity vs. solvency problem – they could use a couple billion dollars right now, but can’t find any cheap sources of it other than doing these asset sales (Q-series jets, their aircraft training unit, etc.). They have always seemed to be on the verge of generating cash, just like Charlie Brown being able to kick the football.

Financially, looking at their preferred shares – BBD.PR.B is trading at 9.6% (noting that if you believe the Bank of Canada will raise rates another 0.25% it is a slightly better bargain), BBD.PR.D is trading at 10.0% and BBD.PR.C is trading at 9.2% (implying slightly that the company will exercise its conversion rights and redeem the preferred shares for stock, which at their current share price will be 12.5 shares of BBD.B per preferred share). There is a very real risk, however, that Bombardier will find itself out of cash and this would result in a suspension of preferred share dividends. This obviously would not be good for preferred share prices, nor would it bode well for the company’s ability to refinance debt. A yield-focussed investor could also get 8.8% on the December 2021 bond issue (8.75% coupon, trading at 99 cents on the dollar) and not worry about a dividend suspension (albeit this is interest income and not eligible dividend income which has a tax impact).

I hold a small amount of BBD.PR.C shares which I picked up back in early 2016 when they were trading at yields in the teens. I did unload some at higher prices in 2017. I did not think I would see them trade like this again, but here we are again.

December 6 will also be Bombardier’s “investor day”, and you can be sure management will try to promise the skies once again and assure investors that the entity will generate cash.

As this catastrophe is hitting the company at the end of the year, there is going to be a lot of window dressing and tax loss selling of the stock. I can just imagine how somebody having a heavy equity holding of this feels at the moment – disgust. Fortunately my position in the preferred shares were minimal, but it still doesn’t feel good to see this much capital evaporate at once.