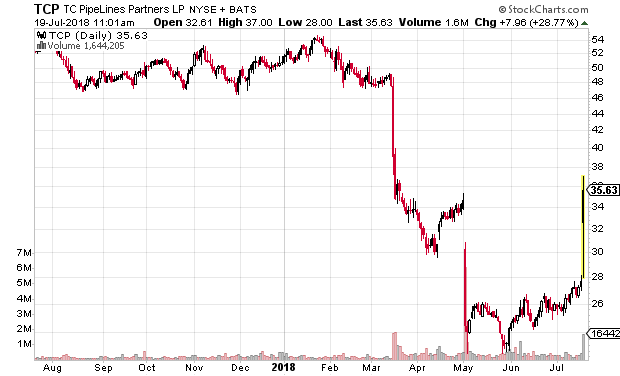

Today was a very interesting day for TC Pipelines MLP (NYSE: TCP) which is the USA MLP arm of TransCanada Corporation (TSX: TRP).

They were heavily impacted by a March 2018 FERC ruling concerning the calculation of regulatory revenue rates for oil and gas pipelines – essentially they were not allowed to incorporate the income tax expense of their unitholders into their rate calculations. Not surprisingly, the stock crashed in March (along with most other MLPs) and when TCP announced the subsequent consequence in their next quarterly report (May) they crashed even further. It is fairly evident by the stock chart when these moments occurred:

Today, the FERC partially backpedaled on this change announced in March for natural gas pipelines only (nothing mentioned on oil pipelines). According to my read of the commissioner’s details, they came to the conclusion that the underlying natural gas pipeline legislation had technical issues which did not allow them to enforce the previous order. Putting a long story short, they came to the conclusion that this change would be considered retroactive rule-making and hence they did not have the authority to implement the change. They provided a mechanism where gas pipelines could voluntarily consent to changes in exchange for the commission to not review their rates within a certain time period, but I doubt MLPs will exercise this if such changes are adverse.

This is effectively a reversal of the decision unless if Congress decides to intervene in the matter. Considering the perpetual dysfunctional mess in Congress and them not touching the underlying legislation to correct this matter, this is a huge victory for natural gas MLPs.

Finally, the rationale for TCP MLP dropping from $50 to $25 in the first place has completely evaporated – although interest rates have increased somewhat (causing some headwinds in the MLP price due to simple spreads over the risk-free rate), one can make an argument that the price should be restored close to previous levels. In other words, there is an argument to be made that the price should go even higher.

The FERC ruling does not appear to affect crude oil pipelines (this is a very loaded sentence).

The disclosure I will make is that I own call options in TCP, which bypasses messy taxation issues of foreigners owning USA MLPs.

========================================

Addenda:

Very quick valuation notes, TC Pipelines (NYSE: TCP)

Units outstanding: 71.3 million

General Partner: (TSX: TRP), owning approx. 23% of the entity

Distributable cash flows, 2015/16/17: $290/313/310

GP/Incentive Distribution Rights: 2% below $0.81/quarter, 15% to $0.88/quarter, 25% above $0.88/quarter

Top-line Revenues/Equity earnings (2017): US$446 million.

Debt: $2.3 billion, staggered across various term facilities/bonds. Refinancing available, will pay slightly more interest in rising-rate environment when rolling over debt. YTM on May 2027 unsecureds: 4.7%

Paper napkin valuation: $310 million / 71.3 million units, $4.35/unit, $35@12%, $42@10%. Does this warrant a 700bps or 500bps spread over debt? Historically was trading around $45-$50 (MLP sector was ‘more sexy’, perceived as ‘ultimately safe’, etc.)

Previous distributions were $1.00/quarter, but post-FERC, reduced to $0.65/quarter, citing debt ratios and anticipated reduction of revenues.

Nice call. But I don’t know if the retail investor are sophisticated enough. These things usually just trade according to yield. It was trading at about 7.5% before the crash ($4 distribution / $53 price); with distribution of $2.6, this would imply the thing is ‘fairly valued’ – unless the management raise the distribution back.

Yeah, those K1 are a bitch…..I’ve been in and out of AMZA and MLPQ (No K1) over the last year for some nice gains…..I prefer to trade them then hold them….. for now.

@Will: Yeah, I felt like writing about it but I can’t give away all my leads on the site although certainly somebody reading my last quarterly report could have had a pretty good idea what I was looking at.

TCP will probably still use this as an excuse to de-leverage (at $2.60 with existing cash flows they’ll be able to repay north of $100M in debt a year), but we will find out their plans at the beginning of August with their quarterly report. I would think there are enough institutional investors to look at actual financial statements of the entity (they are almost one of the easiest to read out of any industry I can think of). One thing for certain is that it is unlikely that TRP will want to re-absorb TCP.

@Marc: Did you know with the Trump tax reform that the IRS, upon enacting regulations, can demand brokers withhold 10% of sales of MLPs as a withholding tax? They have not made this pronouncement yet, but you can be sure it is coming…

Trading today (down about 10%) I’d describe purely as profit-taking. There is a huge amount of future cash flow that underlies a higher valuation. This is probably the best usage of fundamental analysis – knowing what range of values represents fair value when there is hugely volatile trading.

spread on option seems to be huge. ever consider SSF through IB?

@Marc: Did you know with the Trump tax reform that the IRS, upon enacting regulations, can demand brokers withhold 10% of sales of MLPs as a withholding tax? They have not made this pronouncement yet, but you can be sure it is coming…

Sacha….I did not know that, I wonder how that will work with MLP etf’s and cef’s?

@Will: Thought of SSFs but the options had a 30 cent bid-ask spread which wasn’t terrible. Looking at the SSFs history for the near month series, they’re an 18 cent spread. Quite frankly either way to get Delta (as long as you don’t overpay for the options if you go that route) without owning the common was the point. Quite frankly I haven’t used SSFs and see that distributions are treated as corporate events (i.e. price adjusted for the dividend) which in theory should be baked into the option pricing.

@Marc: I would think the ETFs, as long as they are American entities, would not be subject to this. However, don’t take this as legal or financial advice!

Option spreads as of the last couple business days have really blown wide open. Looks like the market makers are simply going hands-off here, possibly until their August 2nd report.

Implementation of the 1446f is currently suspended but the 10% withholding is crazy

[…] July 19, 2018 the FERC provided some clarifications with respect to the future billing rates of natural gas […]

[…] EEP was a dumping ground for some US-based assets for Enbridge and a logical candidate for the MLP structure. This has become less “politically correct” in the financial realm as now the US has enacted a significant corporate tax decrease and also the FERC rulings that I have been writing about earlier. […]