This will be a rambling post in no particular order.

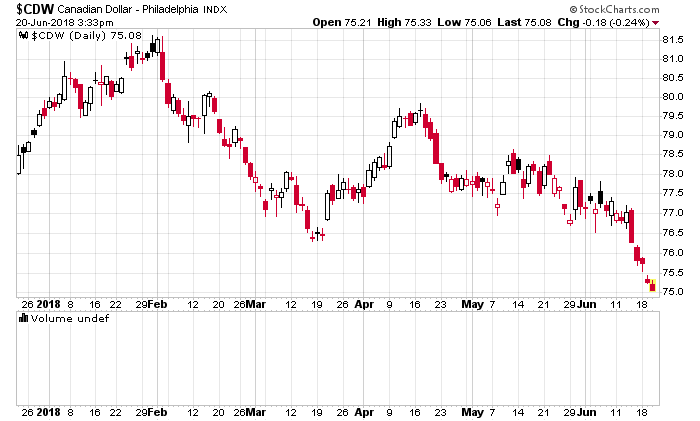

1. The Canadian dollar has tumbled with Donald Trump beating the war drums on the trade portfolio:

This will keep going lower and lower until the Government of Canada realizes that a lower currency doesn’t mean you’re more competitive when you’ve basically killed your own industry. Normally there is correlation between oil prices and the Canadian dollar but this linkage has now been considerably more muted because of WTIC to Alberta oil differentials. Investment has been flowing away from Alberta/SK oil and everything is on maintenance mode.

This will clear the way, however, for the Bank of Canada to raise interest rates another quarter point.

Domestically, this is going to be a disaster for general Canadian standards of living. It seems to be that our largest urban export is continuing to be real estate.

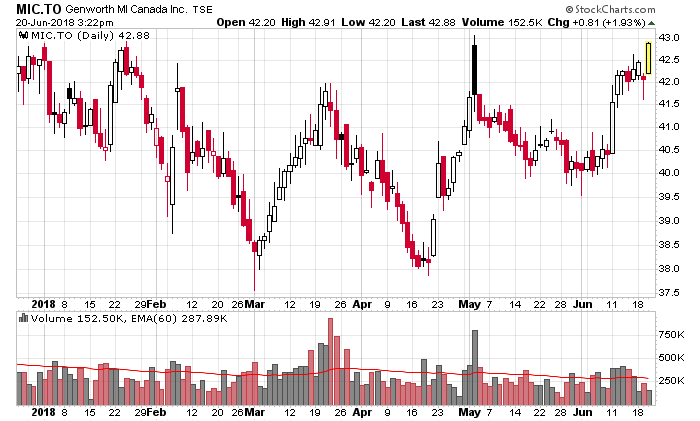

2. Speaking of real estate, bearish market participants in Genworth MI are going to face a short squeeze:

I’m not sure why anybody would want to use Genworth MI as a proxy for Canadian housing when there are so many more other investment vehicles to express this sentiment, ones that are trading well above book value and are making nowhere close to as much money as Genworth MI is on their insurance portfolio.

I’ll send a “hat tip” to Tyler, who writes infrequently at Canadian Value Stocks, for the brief mention of my continuing analysis of Genworth MI. The best analogy I can give is “picking up hundred dollar bills in front of a steamroller” instead of the usual cliche of “picking up nickels”. Genworth MI is claimed to be poised to have a giant collapse, but the variables required to make that happen seem distant at this point in time. Hint: Pay attention to China.

3. Speaking of real estate, the most hyped investment seems to be mortgage REITs and also residential REITs. The cap rates received by purchasers are incredibly low. Example press release linked here, key quotation in the first paragraph:

Northview Apartment Real Estate Investment Trust (“Northview”) (TSX:NVU.UN) today announced that it has agreed to acquire a 623 unit portfolio of six apartment properties (the “Acquisition Properties” or the “Acquisition”) from affiliates of Starlight Group Property Holdings Inc. (“Starlight”). The aggregate purchase price of the Acquisition Properties is $151.8 million (excluding closing costs), representing a weighted average capitalization rate of 4.5%.

A 4.5% cap rate? Do I even need to open a spreadsheet to know that the purchasing side of the transaction is wholly reliant on capital appreciation of the underlying properties for this to make financial sense?

The big favourite in this market is Canadian Apartment Properties (TSX: CAR.UN) and they probably can’t even believe how much their equity has traded up over the past year. They did a secondary at $35.15/unit and probably feel like idiots since just three months later they’re trading at $43/unit.

We drill down into their financials and see that from the last quarter, extended to 12 months, their normalized funds flow through operations (recall that accounting rules will add gross amounts of volatility in REITs due to mark-to-market rules when properties are re-appraised and this difference will be added or subtracted from income, making standard income statement comparisons incomprehensible without going through mental gymnastics) results in a net yield of about 4.3%.

An investment in CAR, therefore will expect to receive 4.3% plus the variable components of changes of rental amounts, property values, financing and operating expenses, and vacancy rates. Will these variable components be enough to give a rational equity investor a higher rate of return as surely nobody would want to take equity risk for a measly 4.3% gain?

Great post – in general I’m not a fan of most Cdn REITs (valuation, appraised values being incredibly subjective/often optimistic, IFRS rules = capex capitalized rather than expensed, reliant on capital markets/debt refinancing to pay dividends, etc.).

For the apartment REITs in particular, I’d suggest that ~4.5% is probably reasonable for current market cap rates (see Minto Apartment REIT prospectus: GTA is sub 4%). Maybe the whole apartment/CRE asset class is overvalued, even in the private markets. But I agree that the formula is the cap rate (4.5%) + NOI growth (2-3%?) – capex (1% of value?) = ~5.5-6.5% return, with the rest being leverage and change in valuation (hard to predict impact of this).

What return would you require from something like this? >6% cap rate? Do you like of the Cdn REITs (Summit seems interesting)? Thanks

I would want to expect something higher than 6% for equity risk. Maybe a pension fund manager that can’t move around a few billion dollars would be happy with it, but I think one can do much better on risk-reward than 6% elsewhere (the most brain-dead examples being something like Power Corp or some other stable financial that has a P/E of 10 or less – or even fishing for preferred or sub debt that’s yielding that much or higher). There just seems to be an implied expectation that real estate valuations will continue to rise. Maybe that’s the case since people are still pouring into Vancouver, Toronto, etc., but eventually the interest headwinds and the economy will go south and this will have to impact valuations.

I’ve been eyeballing MRT.UN but can’t shake off the feeling that it’s just a dumping ground for Sahi. Maybe I should just gamble everything on LRT and pray for a McMurray comeback. But otherwise I don’t really see anything compelling in the entire sector at present. Maybe Alberta will stage a comeback and there are some obvious contenders in that scenario.

You’re bang on about real estate pricing expectations. Toronto/Vancouver CRE right now is about the best in all of North America (lowest vacancy rates, lowest cap rates, high rent growth). Not that much supply coming online either, so maybe there’s room to run still, barring recession, but doesn’t seem like it can go on for 3+ years. Any thoughts what could cause a change in valuations?

Apparently Sahi thinks rates have bottomed so isn’t too aggressive on buying stuff. Selectively selling off non-core stuff I think. (Won’t sell core cause won’t be able to buy it back ever…).

Haven’t dug too much into Summit just yet but based on the PIRET/Blackstone deal, industrial’s the hot market right now. Tailwinds from ecomm, some pressure on land values from the resi market, portfolio’s weighted to ON and QC. Rent growth could be above market expectations + valuation is fairly cheap compared to replacement cost.

A new student housing reit, alignvest, is coming up too – think it further confirms your point in the original post.

Canada does seem to be in trouble. Housing (all forms) has grown to represent ~50% of national wealth (from ~25% at the turn of the 20th century). How does a country create sustainable prosperity for its people when it turns so inward and puts so much capital to economically useless purpose? Yes, housing creates its own industry and creates economic activity in the formal and informal sectors but beyond the basics of providing shelter and safety, its hard to argue that incremental capital would not be better placed in … oh … maybe pipelines and other wealth creating infrastructure. Cap rates of 4-5% might be emerging as the long term norm in this sector.

“Any thoughts what could cause a change in valuations?”

A rise in unemployment comes to mind (which starts the trend of people cutting everything else back so they can finance their mortgages, until they are forced to sell). This would be correlated with a slowdown in the construction industry.

I would also think that if population growth (which is mainly via immigration at present) decreased, we would see price declines. I’m not sure how strong the correlation is between population growth, unit supply and price, but I would expect it to exhibit R^2 of at least 0.5-ish…

But immediately, nothing on the horizon. Maybe those sub-5% cap rates are justified?

on the real estate side I am far more interested in MEQ or MRC. Both trading at a discount and run by smart people.

Sacha – thanks. Agreed on unemployment. Supply story is good and so much of the economy is tied to housing, don’t think anything changes unless housing slows down further.

Philbert – good call, I’ve actually been looking at MRC this week. Seems cheap, but I feel like I might be missing something. The discount almost never gets down to <60%. Is it driven by the retail exposure (more write-downs on the retail coming?)? And then second, I can't think of reasons that would cause the discount to narrow / affo to grow?

Dream moving assets around….is time coming Sacha…are we going to lose our preferred?

@John: Suspect it is partly retail motivated, in addition to Calgary exposure (although the Alberta discount is likely to drop in the coming years). I tend to keep REI.UN as my ‘bellweather’ focus on retail rents. I find it incredible they are trading under book (but do not find them compelling value at the moment).

@Marc: Is the DREAM over? We’ll see… still think it is not terribly rational of people to be paying for the prefs what it is trading at the moment.

@John – as to MRC’s AFFO i have no idea. NAV could be narrowed by Rai taking the company private or even by growing the dividend (though that does not seem to be his priority). I suspect either his death or him taking the company private will be the most probable catalyst to close the NAV gap. I just like the smart way the company is managed, and the safety that the large NAV discount provides.