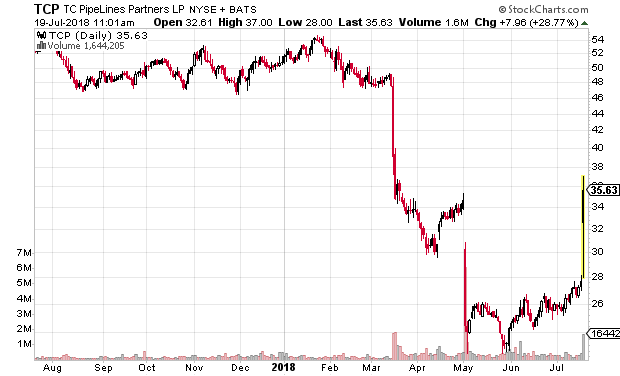

Both entities listed (NYSE: TCP, parent TSX:TRP, NYSE: EEP, parent TSX:ENB) got hit badly with the March 2018 FERC ruling. TCP got hit the worst (as measured by the percentage decline in market value) out of all of the MLP pipeline companies affected by the FERC ruling.

Initially in their Q1 release, they stated that the FERC ruling could have an adverse revenue impact of up to US$100 million. In light of their US$546 million in revenues in fiscal 2017, this was not a trivial impact. As a result, they dropped distributions from $4/unit/year (about US$292 million) to $2.60/unit/year (about US$190 million). This was a reduction of 35% in distributions.

The interesting element is that because it is structured as an MLP, the company can retain the cash and use it to pay off debt while the unitholders face the income taxes payable even though they never see the cash-in-hand (directly). Reducing distributions is a very effective strategy to paying down debt.

TCP’s MLP units were trading at about $48 before the FERC announcement. After the 35% distribution drop, the MLP units dropped more than half over the subsequent two months.

While there was an economic substance to the reduction in unit price (the FERC announcement did have a genuine impact on future distributable cash flows), the impact to the unit price was overblown (perhaps due to inflammatory language by the parent saying that TCP was “non-viable” and a sudden fear that they would not be able to obtain credit, etc.).

On July 19, 2018 the FERC provided some clarifications with respect to the future billing rates of natural gas pipeline MLPs and the taxation basis that they can charge customers. The stock market initially launched the unit price from $26 to $35, but that has tapered down as there is a realization that the new pronouncements are a partial backpedaling of the original March announcement.

Today, TCP announced their Q2 results and quantified the results of the revised FERC ruling to $40-$60 million. I’ve read management’s presentation and listened to the conference call for some additional colour. $40-60 million is still a significant amount of revenue to be lost, but not as bad as previously thought. There was still considerable uncertainty as to the exact number and also the future state of governance – the initial obvious route was conversion of the MLP to a C-Corporation, but now that does not appear to be attractive. The other obvious decision is a re-acquisition of TCP within TRP, similar to how Enbridge Energy Partners (NYSE: EEP) has a proposed re-acquisition by Enbridge back on the table.

Right now, pre-FERC, looking at 2017, TCP has revenues of $546 million (transmission revenues plus equity earnings), and about $445 million in operating cash flows (approx. $6.20/unit). Distributable cash is $310 million ($4.35/unit).

The impact of the FERC decision will start to hit the financial statements at the end of 2018, so 2018 will still be a relatively “clean” year. The excess of cash generated over distributions will be used to pay down debt – At the beginning of the year, the balance on their credit facility was $185 million, and on August 2, was paid down to $90 million. By the end of the year, it should be around $40 million or so. The coupon rate of this debt is very low (linked to the short-term US rate – about 3% at the end of June 2018) so there won’t be much of an interest expense savings.

The remainder of the debt profile of the company is at a low interest rate and can be extended without pressure given the investment grade credit rating (in 2019, $55 million, in 2020, $270 million, in 2021, $375 million, in 2022, $500 million).

Operationally, there are the usual concerns about smaller pipelines that have customer concentration risk (Bison expires in 2021, consisting of 17% of cash flows), but I do not see fundamental threats to USA domestic natural gas transportation.

Taking $50 million off of distributable cash results in $3.65/unit. At the market price of $30/unit, that’s a 12.2% total return on something that is in a very stable and predictable business. The $30 unit price appears to be a bit low and I suspect that TRP will attempt to re-incorporate TCP into it while the price is still relatively low.

Prior to all of this FERC business, six months ago (February 2018), TCP was trading at $50/unit and giving $4/unit distributions (8%) at roughly a 90% payout ratio. Now that the FERC matter has been settled somewhat, the market is currently pricing TCP at an 8.7% distribution level, at roughly a 70% payout ratio post-FERC (2019 steady-state amounts). The core business (natural gas transportation) hasn’t changed, so why the sudden doom and gloom? This MLP should creep up higher as regulatory matters get clarified. You’re not going to see TCP double to its previous US$50 glory, but I believe US$30/unit appears to be low.

(Note: TCP goes ex-dividend tomorrow, so you will see an immediate 65 cent drop in price from the currently mentioned $30 current market price when trading opens Friday).