I talk much more about finance than accounting on this website, although I am a professional accountant. A good analogy is math and physics – people in both fields tend to understand the other, more so than the difference between chemistry and biology.

Effective this year, companies will have to adopt IFRS 16, which governs accounting for leases.

Other than enriching accounting consultants that will have to dig into the structures of leases of various firms, this will have a material impact of the reported assets and liabilities on a company’s balance sheet. New students of accounting will also have one more layer of complexity to memorize at exam time, while textbook manufacturers will undoubtedly be happy.

Specifically, the distinction between an operating lease vs. a capital/finance lease is removed and instead all leases will have an asset and liability component. The asset of the lease (the item which you are buying the rights to use) will be depreciated over time, coupled with an interest expense component for the financing cost of the lease, with a depreciation charge to reduce the asset value.

From an investment perspective this changes the character of “EBITDA”, where companies that heavily use operating leases would previously have expensed such costs (typically in operating expenses), while after IFRS 16 is implemented, they will suddenly find their EBITDAs increase because the lease cost will have strictly an interest and depreciation component. They are still expenses, but the characterization of the expense is now changed. This will be an accounting windfall for companies that traditionally are valued on EBITDA metrics.

So if you find it annoying how companies use EBITDA as a proxy of profitability (which it could be given the right assumptions – but most companies abuse the EBITDA number to inflate the perception of their profitability), after IFRS 16, good luck! Just remember, you can only live on after-tax cash flows and not EBITDA!

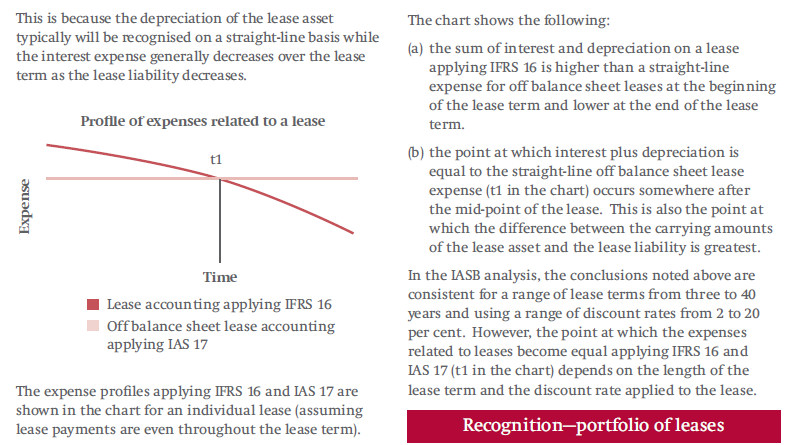

The other strange implication of the rule is that once a lease is initiated, it will initially be more expensive at the beginning of the lease, and less expensive later in the lease as the embedded interest expense of the lease declines. So let’s say you lease a million dollar jet for 10 years, your expense profile, depending on your cost of capital component, on year 1 would be $125,000 while on year 10 would be $75,000 even if you fork out $100,000/year to use it. Investors have to add one more layer of effort to separate what is happening on the income statement with what is happening on the cash side of things. (Even this example is not quite correct – the lease asset may be $1 million, but the liability is going to be bigger since nobody will want to lease a $1 million jet for a $1 million stream of cash).

You have to love these accounting standards that make life even more complicated for the layman in the name of increasing accuracy. Currently, an investor could look at the notes on the financial statements to understand what a company’s future lease commitments were. One-shoe-fits-all accounting sounds great in principle but it has the consequence of making financial statements more difficult to read and understand between companies even though the goal is to make them directly comparable.

[…] convinced that the purpose of a lot of IFRS edicts is to make financial statements unreadable. The introduction of IFRS 16 adds two lines to most companies’ balance sheets and while mildly annoying (mentally one has […]

[…] un-leveraged. As of May 4, 2019, they have $122 million cash and zero debt. As Tyler pointed out, IFRS 16 had a disproportionate impact on the reporting of their balance sheet – I will point out any […]