Hat tip to Tyler for getting this on my radar. I’ve personally been following Reitmans (TSX: voting stock RET, non-voting stock RET.A) on-and-off for the past decade or so. Not that I’ve been a purchaser of women’s clothing but financially it is a typical story of the decline of a fairly benign women’s fashion retailer facing the steamroller of competitive marketing and the internet.

Fortunately for Reitmans, they are highly un-leveraged. As of May 4, 2019, they have $122 million cash and zero debt. As Tyler pointed out, IFRS 16 had a disproportionate impact on the reporting of their balance sheet – I will point out any accounting system does not change the actual economics of a company’s operations (other than covenants and restrictions that are governed by the stated accounting values!).

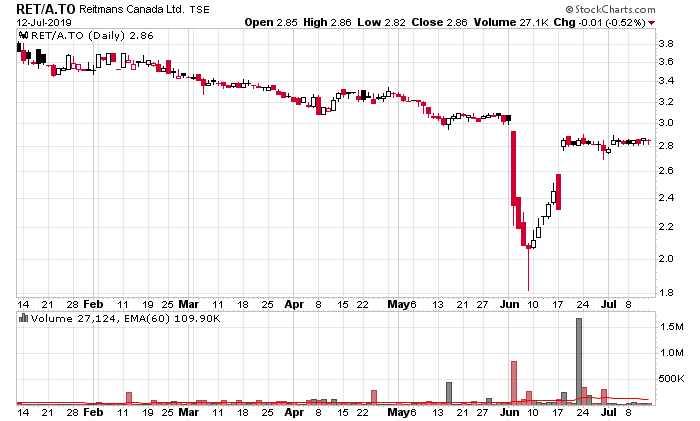

On June 3rd, RET announced their quarterly results, which were less than inspiring (sales down, margins down, cash drain increased from the previous year’s quarter) and their stock tanked. There was a panic sale before somebody with larger pockets decided they wanted to accumulate shares in the low 2’s.

On June 17, RET announced a substantial issuer bid (SIB) for CAD$3/share of up to 15 million shares of RET.A stock. There were 49,890,266 shares outstanding, so the 30% SIB is not a trivial amount – and also nearly 40% of the cash on RET’s balance sheet. The voting stock has 13,440,000 shares outstanding and this will be untouched – directors and insiders have 56.9% control of these shares, although if you want to be a muzzled voting partner, the stock does trade a few thousand shares a day on the TSX.

Shareholders have until July 26 to figure out whether to tender.

The SIB was filed on SEDAR, but I will spare you the trouble and attach it here.

I always find these documents interesting to read, specifically the background of the transaction. Merger documents also have to include the timeline of discussion and negotiations. For RET’s SIB, it is as follows:

During the spring of 2019, senior management of the Corporation was approached by a significant unrelated Shareholder indicating its desire to realign its portfolio and to sell all of its Shares. As a result, such members of senior management and the Board of Directors began engaging in preliminary discussions concerning possible strategic activities and opportunities that may be in the best interests of the Corporation and could provide enhanced liquidity for all of the Shareholders. Among the alternatives discussed was the possibility of pursuing a substantial issuer bid to repurchase a portion of the issued and outstanding Shares.

“a significant unrelated Shareholder” is not defined in this document, but my first guess is Fairfax.

I’m sure another alternative was trying to find a buyer for the company, but this would require the control group agreeing to it.

In May 2019, following discussions with senior management of the Corporation, certain independent members of the Board of Directors seriously considered the possibility of pursuing a substantial issuer bid and the alternatives thereto. Given the Corporation’s significant cash on hand and marketable securities portfolio, certain independent members of the Board of Directors and senior management of the Corporation considered that, in light of the trading price of the Shares, the low return from its investment in marketable securities and interest rates earned on the cash balance, a substantial issuer bid would be a good use of the Corporation’s funds and sought preliminary advice from Davies Ward Phillips & Vineberg LLP, legal counsel to the Corporation, in order to further consider and evaluate the possibility of making an offer to repurchase a portion of the Shares.

The key word is “certain” in “certain independent members of the Board of Directors”. Clearly this was not a unanimous decision.

The rest of the document is bureaucracy to adhere to MI 61-101 and is not terribly juicy.

Taxation (hat tip to Fred for this one)

This is for Canadian residents.

A Resident Shareholder who sells Shares to Reitmans pursuant to the Offer will be deemed to receive a taxable dividend on a separate class of shares comprising the Shares so sold equal to the excess, if any, of the amount paid by Reitmans for the Shares over their paid-up capital for income tax purposes. Reitmans estimates that the paid-up capital per Share on the date of take-up under the Offer will be approximately $0.66. As a result, Reitmans expects that a Resident Shareholder who sell Shares under the Offer will be deemed to receive a dividend. The exact quantum of the deemed dividend cannot be guaranteed.

Careful – if you tender your shares, you will receive a deemed dividend of $2.34/share! Fortunately your capital gain will be reduced (in most cases, one exception is if you just bought the shares before/after 30 days of the final disposition) by said amount, which will lessen the tax bill somewhat. Unfortunately, almost all shareholders of RET are sitting on loss situations – so in order to take full tax advantage of the situation you would need to be able to offset 3 years’ prior capital gains, or future capital gains. Otherwise, you are taking a very large tax hit to tender your shares.

Putting on my individual CPA tax advisory hat, in general, if your desire is to dispose your shares of RET, you should ask yourself whether taking a dividend with a relatively large capital loss (the tender route) or a relatively small capital loss with no dividend (sell in the open market) is better for your personal taxes. RET.A shares are trading at around $2.85 presently so going through the open market approach will involve surrendering a potential 15 cents per share, offset with the tender route uncertainty that at a minimum, only 30% of your shares will be tendered.