I am pretty convinced that the purpose of a lot of IFRS edicts is to make financial statements unreadable. The introduction of IFRS 16 adds two lines to most companies’ balance sheets and while mildly annoying (mentally one has to make a provision for lease-heavy companies that the amortization of the lease asset/liability is akin to a lease payment and make sure not to perform apples-to-oranges comparisons when looking at EBITDAs), the biggest pain has to be IFRS’ tenancies to use mark-to-market fair value adjustments whenever such data is available.

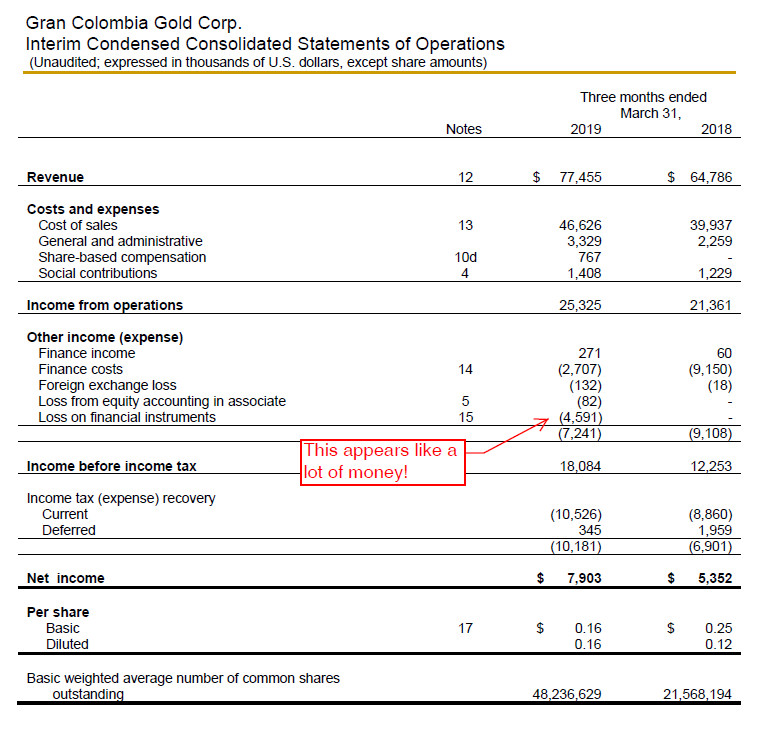

As an example, I am going through Gran Colombia Gold’s (TSX: GCM) last quarterly statement and the income statement is getting to the point where it is almost unreadable.

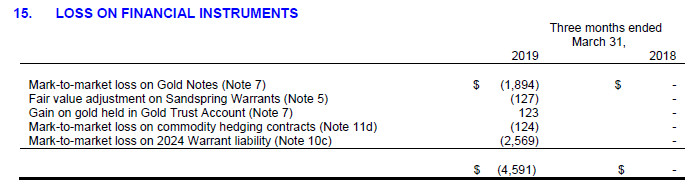

For example, under “Other income (expense)”, the entire $4.591 million under “Loss on Financial Instruments” consists of fair value adjustments. For an untrained eye these would seem quite relevant in that one would perceive the company is ‘paying’ more in financial expenses than is actually the case. From an analytical perspective, these fair value adjustments are irrelevant.

I’ll break down this even further, which is covered by the rules of IFRS 9.

$2.569 million of the $4.591 million consists of a mark-to-market adjustment on the fair value of warrants the company has outstanding.

When the company issued the warrants in conjunction with a notes offering, they issued 12.151 million warrants which were publicly listed on the TSX (TSX: GCM.WT.B). The warrants are convertible at CAD$2.21/share.

Let’s step back and remember the following law of accounting:

Assets = Liabilities + Equity

In a sane world, these warrants should reflect equity (the warrants in no circumstances can ever reflect a drain on the assets of the company). However, in our brave new IFRS world, they are a liability because they represent value that has not been set at a fixed price by the company. GCM reports in US currency, so therefore the warrant liability in Canadian dollars is a floating obligation and thus needs to be re-valued every quarter!

Once the door was open to expensing stock options, the logical progression is that any issuance of like instruments (such as warrants) need the same treatment.

Since the warrants are publicly traded, the fair value of the liability can be recorded using the market price. This needs to be updated quarterly.

The warrants at the end of December 31, 2018 were worth $13.8 million. On March 31, 2019 they were worth $16.4 million. Therefore, the company “lost” $2.6 million and this has to be reported on the income statement as a financial expense.

This expense, in no manner, reflects an actual cash expense. Nor does this expense affect the valuation of the company in any respect. This “expense” does not impact the taxes the company has to pay.

What it does, however, is really skew any ratios that may need to be calculated. For example, if you have an excessively high non-cash expense due to a fair value adjustment, it would serve to understate your net income, or make your apparent tax rate higher than it actually is.

Perhaps this is why most people do not read financial statements anymore – they’re becoming more and more difficult to read.

However, opportunity exists in complexity – if computer programs that are designed to screen for fundamentals do not factor in irrelevant expenses such as these fair value adjustments, companies that appear to be losing money on the income statement could be undervalued by the market as standard stock screens will report them as less profitable than they actually are. I’ll leave it at that.