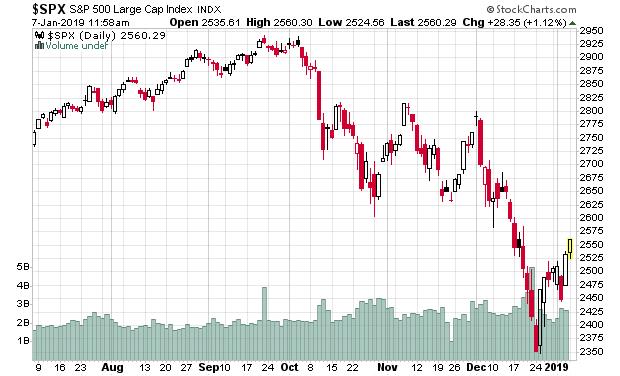

Life looks rosy again in the financial markets!

So going from the “the world is about to end” mantra in December, we’re back once again to sunny skies.

In particular, interest rate futures are projecting a rate cut later this year, which is a complete turnaround to events just three months ago.

So as a result, almost anything with a yield has been bidded up since the beginning of the calendar year.

It’s as if everything that has been thrown away in the previous rising rate environment is now back in vogue again. It’s like the proverbial crowd rushing out of the exits in December, only to rush back in January?

Very fascinating.

Surprise is the blows out job report be interpreted not being interpreted as a negative? ie. Rates going to rise!!!

I guess people believe in the power of Trump of strong-arming the FED like he did to everything that was in his way so far.

We will see how central banks react.

The market is shizophrenic. MAXR loses less than 5% of revenue 85% of which can be recouped via other hardware. Gets clipped 38%.

Hardware insured for $183 Million. Book cost $155 Million

FFH new 3 year low??????

What is a “no nothing investor” to do.

BTW thanks CM for yeilding 5.26%

MAXR has a serious issue with its debt. They have a ton of it. It’s a real shame that the old MDA gets blown up this way.

Companies that do international relocations like this don’t fare very well. I was stupid enough to lose some capital a few years ago when this happened (look at IMRIS if you want to re-open bad wounds – I should have just sold it immediately after they announced relocation but was too ignorant).

Also MAXR is one of those companies where you can’t use EBITDA – unless if you anticipate the company is no longer going to be firing up satellites into space, the “DA” is a really really really material part of the financial statements.

FFH should do reasonably well if they can price insurance properly. They made a bold bet on the S&P 500 hedging and the CPI-linked derivatives which both completely busted, but I can see why Prem made the arguments he did. It cost them a bit of capital and so I don’t think the market appreciates their capital being used as a gambling vehicle until it actually works (e.g. 2005-2008 mortgage crisis). If you want harder core value, ELF also looks attractive, but be cautioned that ELF is one of those types of stocks that you’d want to hold knowing that you’re going to entering into a 10 year coma.

Re ELF – do you have any additional thoughts on this one? Is the thesis basically that book value grows 6-8% per year and there’s some upside potentially if P/B goes from 0.5x to around 0.6x-0.7x?

Thanks,

John

Hey John, yes that is 80% of the thesis. The other bit you missed is that about $400 of book value is Empire Life, a life insurance operation which has been posting ~12% ROE lately. It is carried at book value on ELF’s balance sheet, but as a public company or to an acquirer Empire Life is worth somewhere between 1.4x-1.9x book value. So the true value of the assets could be upwards of $1700 while trading at $760. Duncan Jackman has been a seller in the past (sold E-L’s P&C business when he took over) so it’s not that farfetched he could realize this value some day.

You can “win” by ELF rerating to 60%-75% of book (though it has traded at a premium to book value in the past) or you can “win” from a big value realizing asset sale. In the meantime you have the approximately market return in book value growth to tide you over until those happens or Jackman takes it private at 90% of book (speculation on my part, but evidence points to this).

I don’t own any shares of ELF but valuation-wise the argument would be a closer convergence to book value on top of a profitable business that builds on book value. This stock is not for those seeking action, however – it is probably the most low-profile business I can think of in the billion+ market cap space.

Thank you both for your responses. That makes sense, seems the thesis is quite similar to the one for Morguard Corp.