The traditional financial metric has the P/E ratio being some amount over the risk-free rate.

For example, if the long-term government bond yield is 5%, then the equity valuation would be a premium over this, say 8%. The spread is the risk you take for an equity investment compared to a guaranteed payout on government debt.

The above example means you’d pay 1/8% = $12.50 for each dollar of cash flow, or also a price/earnings of 12.5.

This is a gross approximation, and does not take into a myriad of factors, especially future earnings growth/decline over time and the balance sheet condition (leverage distorts the above calculations).

As a most trivial example, Microsoft, which can be reasonably anticipated to be around for the indefinite future, is estimated to earn $10.66 in their fiscal year ended June 2023. If this extrapolates forever, at the current $300 share price, you are getting a 3.6% return, or 28 times earnings.

Considering the 30-year government bond is 2.7% at present, this is not much of a premium to take risk. Obviously there is some anticipation of earnings growth at Microsoft (at a minimum, one can expect them to be able to raise prices for inflation).

Either way, investors are accustomed to buying non-high flying companies at reasonable valuations, say 9 to 30 times earnings, depending on the perceived stability and earnings power of the company.

However, in the cyclical industries, the earnings factor over time is very volatile. Nothing exhibits this better than commodities.

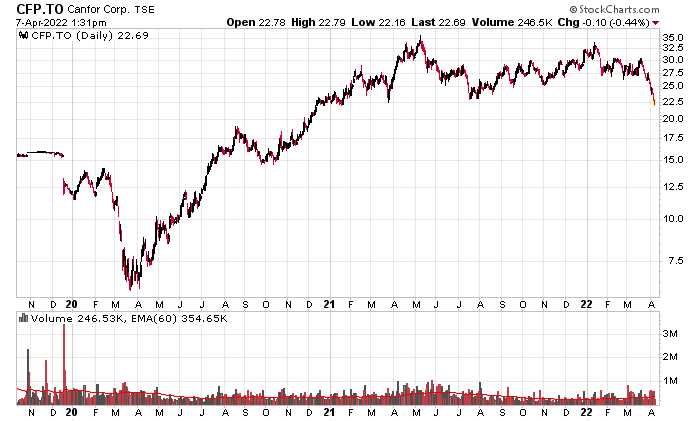

Canfor (TSX: CFP) is a good example of this.

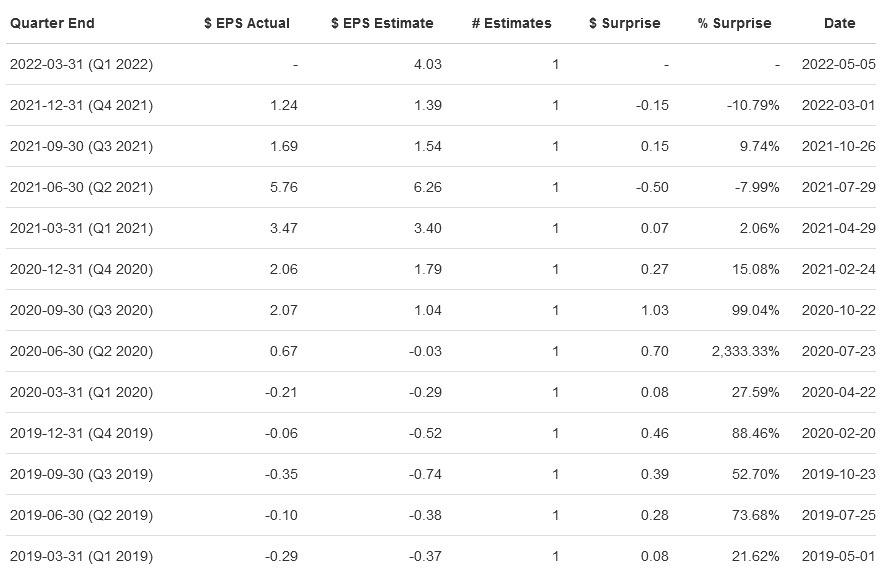

We take a look at their historical earnings, which is extremely choppy:

Just on the basis of historical earnings, if you took the past four quarters, Canfor, at $22.69, is trading at 1.87 times earnings, or a 53.6% earnings yield!

Of course, things are not that easy in commodity-land. There was an obvious windfall opportunity in lumber in the aftermath of Covid-19.

Despite that, analysts are projecting a 2023 earnings of $5.08/share, which is still 22%.

The issue is that this is a stale estimate. If raw lumber prices continue to drop, this estimate will surely drop, along with the share price. Indeed, the share price itself is a reasonable signal that this estimate is likely high.

The other factor is the duration of the earnings. Cyclical companies are, by definition, ones that go through boom-bust cycles as investment kicks in and supply starts to flood the market. The lumber market in this respect is a lot quicker than some other resources that require half a decade to open up infrastructure.

If this level of earnings is projected to last further in time, then the current price will rise. Conversely, if the earnings deflate quicker than expected, the share price will drop.

Either way, it is gut-wrenching to sell a company that seemingly is trading at such a low multiple. Sometimes, selling at a low single digit multiple is a correct decision!

However, unlike the much more stable Microsoft, an investor is rewarded much more for getting the earnings picture correct for a cyclical company – correctly projecting the future in an earnings-volatile environment is much more rewarded.

Does this mean that Canfor, at 2x or 4x or whatever, is a better investment than Microsoft because it is so seemingly ‘cheap’?

This brings me to the original question on the title of this post – what is a good earnings multiple?

The answer is there is none.