The past week was relatively interesting.

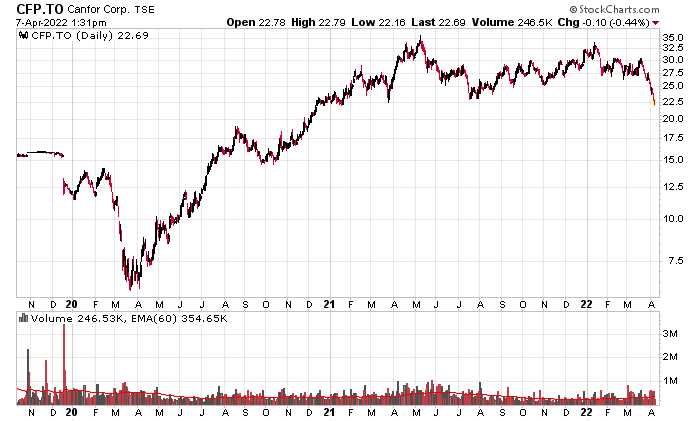

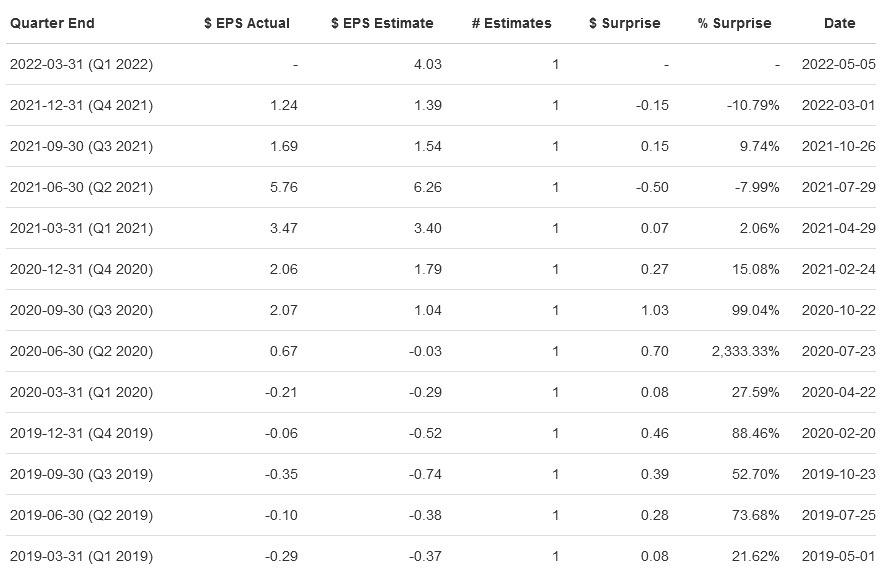

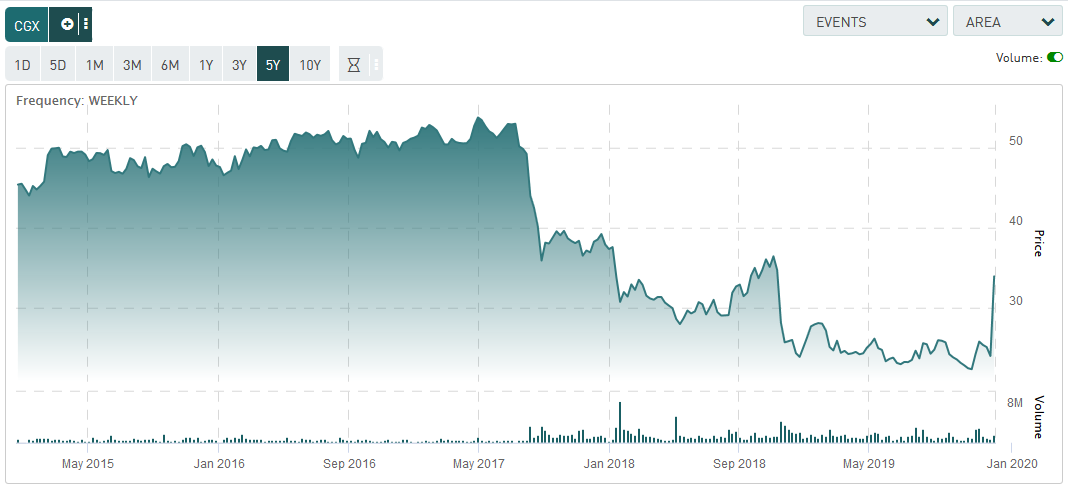

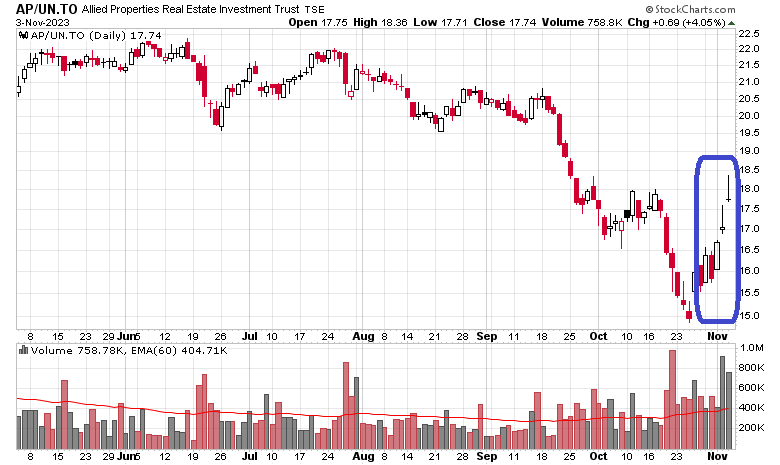

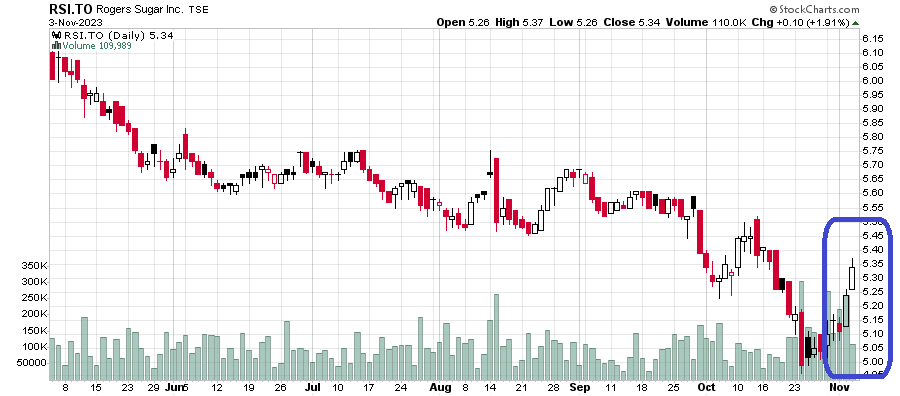

The 10-year bond yield went down about 0.25% from the beginning to the end of the week. Likewise, the long part of the yield curve also dropped (prices rose) and a whole flurry of the usual interest rate sensitive subjects got taken up VERY sharply. I’ll just give a few of them, but you get the idea – these four are from very different industries:

(But also take a look at REI.un.to, CAR.un.to, etc. – also dramatically up over the past few trading days).

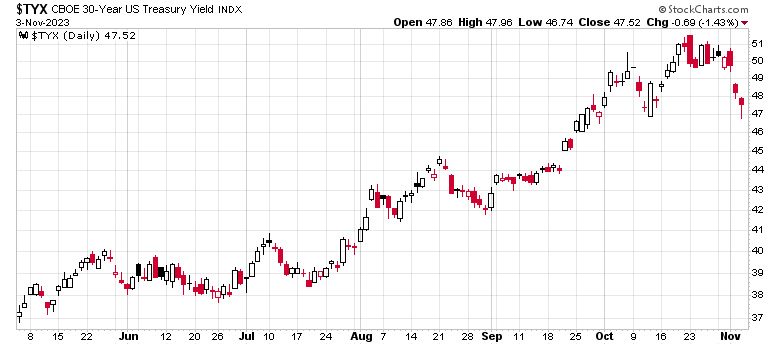

REITs, lumber, sugar, and fast food. All of these are yieldly and leveraged. Don’t get me started on other components of the fixed income markets either, but I’ll throw in the 30-year US treasury bond yield:

There is a cliche that in bear markets, bull trap rallies are the sharpest. This is usually the case because short sellers are a bit more skittish than in the opposite direction.

My suspicion is that the bears on the long side of the bond market got a bit too complacent.

The calculation of the risk-free rate is a very strong variable in most valuation formulas. If you can sustain a 5% perpetual risk-free rate, there is no point in owning equities that give a risky 4% return. The price of the equity must drop until its yield rises to a factor above 5% (the number above 5% which incorporates the appropriate level of risk).

So what we see here is the strong variable (risk-free rates) moving down and hence the valuation of yieldy and leveraged equities rising accordingly, coupled with some likely short squeeze pressure on the most leveraged entities.

There are likely powerful undercurrents flowing in the capital markets – the tug-of-war with the ‘higher for longer, inflation is here to stay’ crowd competing with the ‘Economy is going bust, the Fed has to lower rates!’ group.

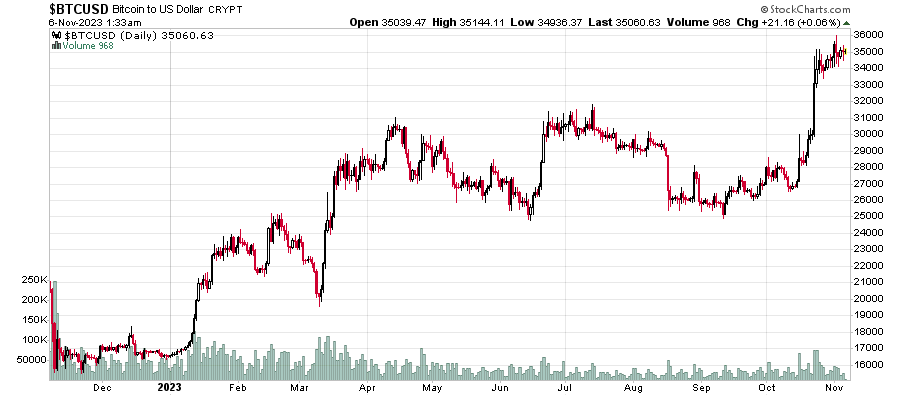

The last chart, however, I must say was not on my bingo scorecard for 2023 – Bitcoin is up over double from what it was trading at the beginning of the year:

I should have just pulled a Michael Saylor and gone 150% on Bitcoin. Go figure.