Quite a few things going on.

1) With the rejection of the Canfor offer, the stock went from $15 to $12, but recovered to $13 as I’m writing this. Many investors are probably engaging in the Canadian version of Buffett-following, which is “if Jim Pattison thinks it’s worth buying at $16, surely buying at $12 or $13 isn’t that bad.”

I do agree with general market sentiment that Canfor was lowballed, but the forest industry is cyclical and most definitely we are in the low part of the cycle. When things will emerge again remains to be seen. The good news with Canadian lumber is that it is one of our few economically competitive exports and doesn’t require a pipeline to transport. In addition, environmental groups have shifted their political focus in the last couple decades from antagonizing forestry to fossil fuels, which gives them some breathing room (for now).

In British Columbia, hardly a month goes by without hearing some news about mill shutdowns and the like. The industry is really suffering right now. The renegotiation of NAFTA and expiration of the previous softwood lumber agreement (October 2015) did not help matters at all.

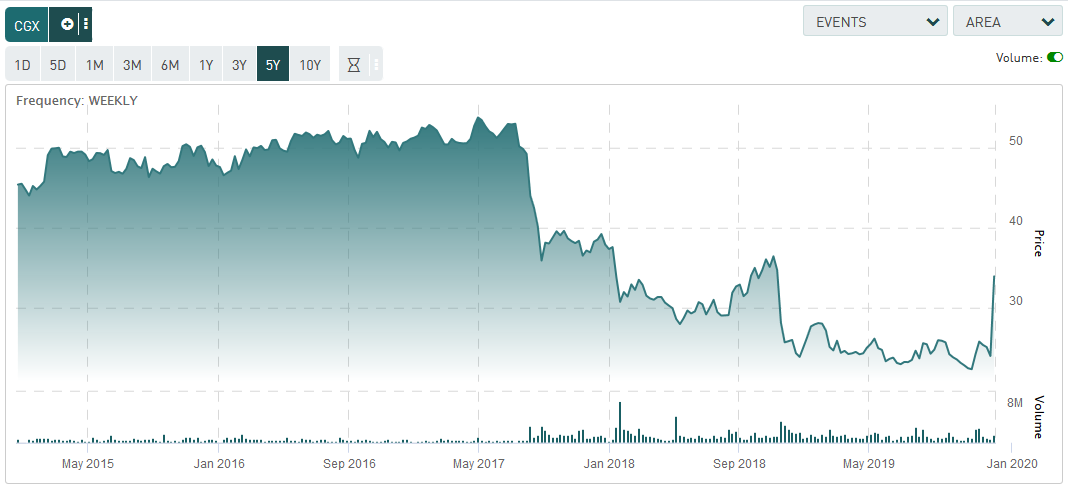

2) Cineplex (TSX: CGX) getting taken out at CAD$34 is a gift to CGX shareholders. A British firm, Cineworld, apparently has too much money and has spared Cineplex owners from taking future losses. As you can tell by the tone of this paragraph, I did not perceive Cineplex’s future business chances as being particularly rosy. The business did have value but not at the price they were trading at. I’ve written about it a few times in the past and will leave a chart here for historical purposes:

3) Another takeout which I thought would go through was HBC (TSX: HBC), which (at $10.30) was withdrawn by the proponents (Baker Group and others, 57%), and a subsequent $11 offer by another significant minority shareholder group (Catalyst, 17.5%) was rejected by the shareholders offering $10.30. This is a gigantic corporate governance mess, but what was interesting was the posting of all the real estate appraisals on their investor relations site. Get some commercial quality information for free!

4) I’ve actually been active taking small stakes in various companies in late November and December. The range of companies is widely varying. For the first time in quite some time, I’ve deployed some capital south of the border.