We are all forced to be closet macroeconomists and for that, I’d suggest reading Ray Dalio’s primer on money, credit and debt:

More specifically, the ability of central banks to be stimulative ends when the central bank loses its ability to produce money and credit growth that pass through the economic system to produce real economic growth. That lost ability of central bankers typically takes place when debt levels are high, interest rates can’t be adequately lowered, and the creation of money and credit increases financial asset prices more than it increases actual economic activity. At such times those who are holding the debt (which is someone else’s promise to give them currency) typically want to exchange the currency debt they are holding for other storeholds of wealth. When it is widely perceived that the money and the debt assets that are promises to receive money are not good storeholds of wealth, the long-term debt cycle is at its end, and a restructuring of the monetary system has to occur. In other words the long-term debt cycle runs from 1) low debt and debt burdens (which gives those who control money and credit growth plenty of capacity to create debt and with it to create buying power for borrowers and a high likelihood that the lender who is holding debt assets will get repaid with good real returns) to 2) high debt and debt burdens with little capacity to create buying power for borrowers and a low likelihood that the lender will be repaid with good returns. At the end of the long-term debt cycle there is essentially no more stimulant in the bottle (i.e., no more ability of central bankers to extend the debt cycle) so there needs to be a debt restructuring or debt devaluation to reduce the debt burdens and start this cycle over again.

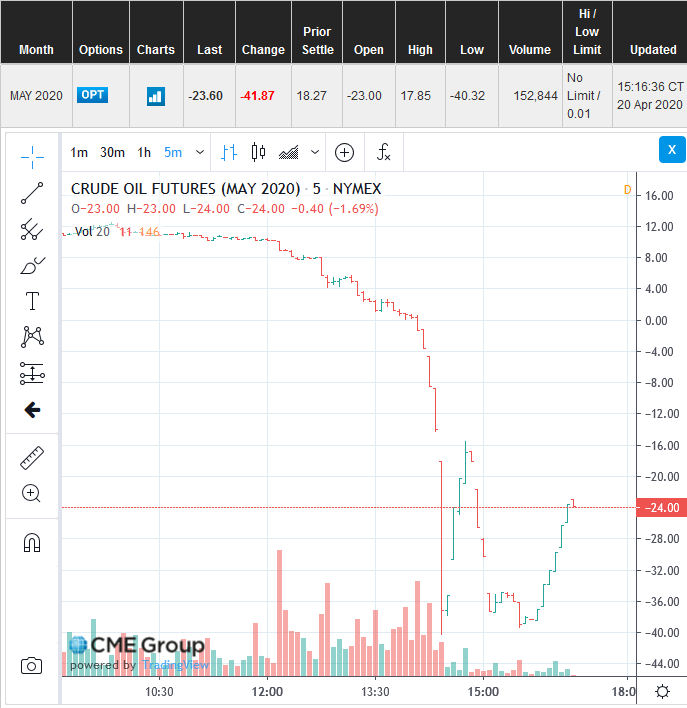

Does this remind you of anything that is going on right now?

With monetary policy at an effective zero bound (I don’t really care whether the interest rate is 0.25%, 0.75% or -0.5%, it is effectively zero and the negative bound is the ability to store paper currency underneath the mattress), the ability for central banks to stimulate the economy (without causing reams of economic damage with massive inflation) is effectively toast. The large recent failure was to not attempt a better normalization after it was perfectly evident the 2008-2009 economic crisis was passing, coupled with the US government not being fiscally responsible. In Canada, Harper was on the right track (he got the budget balanced and the Bank of Canada was able to escape the economic crisis with far less intervention than the US Federal Reserve), but Trudeau and the Liberals have done an exceedingly fine job of reversing this, and now Canada is basically in the same boat as the USA – central banks are employing quantitative easing as a last resort to stimulate economic activity.

The big difference this time is that when the government also mandates a shutdown of the economy, it doesn’t matter how much stimulus you put out there, the real economy is not going to respond. Why would a restaurant owner at this point in time make any investment at all when you have talks of COVID-19’s “second wave” and this can just start all over again?

The real interesting implications occur after one asks what the new currency will look like when it goes from fiat back to something that the public has confidence in. Will that be gold, or bitcoin (or some other crypto)? My big problem with bitcoin, and most cryptocurrencies in terms of them providing a “hard asset” is the dominance of the hash – most of the power in the network has been increasingly centralized to miner pools and it is getting to the point where the possibility and allure of collusion is effectively the equivalent of 51% of people deciding to steal the 49%’s capital.

I would deem it more likely that central banks will try to introduce a parallel currency.