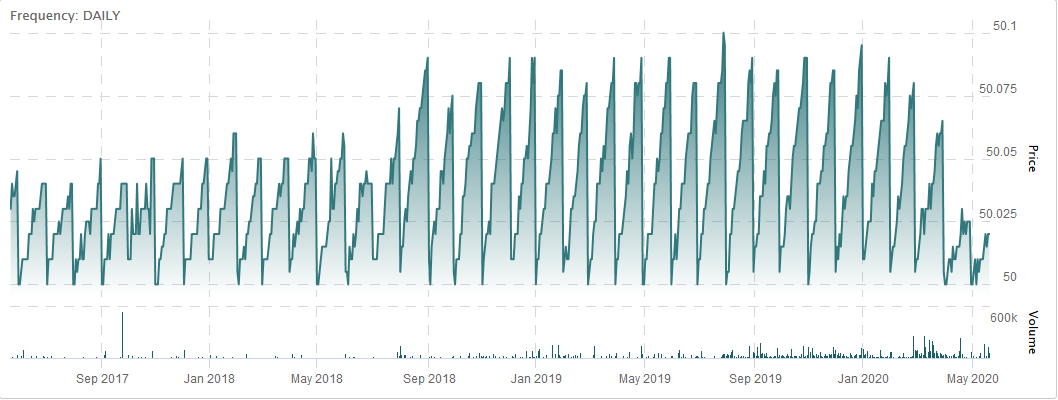

A year ago, if you had spare cash in the brokerage account, it made sense to dump it into a cash-parking ETF such as (TSX: PSA) and get your 200 basis points of yield while you waited to make a decision on your capital.

You can see the effect of the decrease in interest rates from the Bank of Canada:

Now cash in this instrument yields 65 basis points, minus a 15 basis point MER, leaving a net of 0.50%. Might as well keep it in zero yielding cash instead of bothering with the hassle.

I found it amazing to know that despite the decrease in interest rates to nearly nothing, that PSA’s assets under management is still $2.2 billion! The managers are being paid $3.3 million to administer a savings account.

I note that one of their competitors, (TSX: HSAV) had to decrease its management expense ratio from 18bps to 8bps. Its gross yield pre-MER is 75bps on a $313 million net asset value.

Might as well keep it in liquid cash at this point. Who knows if the market maker will decide to have a heart attack and you can only liquidate with a 25 cent spread at the worst moment?

Nice post, Sacha. CMR is another one. I keep my funds at EQ Bank actually – pays a 2% interest and CDIC protected upto 100K!

Or you can play the HISA game. I know many snicker at those +2% interest rates, but a few keyboard strikes maybe twice a year will get you that. I’m getting 2.8% on my USD and CAD for 6 months at Tangerine. Last year I got 3% on my CAD & USD for 6 months. I don’t remember the last time I have averaged under 2.5% for cash for the year…..

I don’t believe in margin….have never ever used it except this long weekend when I had to transfer USD to TD….with 2 day settlement now it can cost you a days interest:)

Hi Sacha,

Is there any precedent to market markers having a heart attack and it trading at a 25 cent spread? I Imagine this wouldn’t occur on a cash ETF.

“Chandhok says spreads should only widen if there are technical difficulties, if the fund tracks volatile or illiquid markets, trading of an underlying security is halted, or if it’s difficult for a market maker to hedge a position. These situations make it difficult to trade the underlying securities and determine their prices.”

None of these would apply to cash ETFs.

I looked at PSA and HSAV’s trading on March 23rd (the worst day of this CoronaCrisis) and their spreads were one penny with ample liquidity at all times. Certainly this is one data point against my ‘liquidity’ argument in that it would appear you could get a clean liquidation, short of a global halt on the exchange (remember that one day where the TSX vomited and had to close down after two hours of trading in the morning?) These are remote scenarios, I agree.