I have discussed cash ETFs before (tickers: CASH, PSA, CSAV, etc.) and they are all fairly cookie-cutter – they invest cash into banks and distribute interest income.

A unique product is HSAV, which is a corporate class cash ETF, which means that investors functionally receive their gains in the character of a capital gain instead of interest income. It charges an MER of 8bps higher than “regular” cash ETFs, but this is more than offset by tax savings in non-registered accounts.

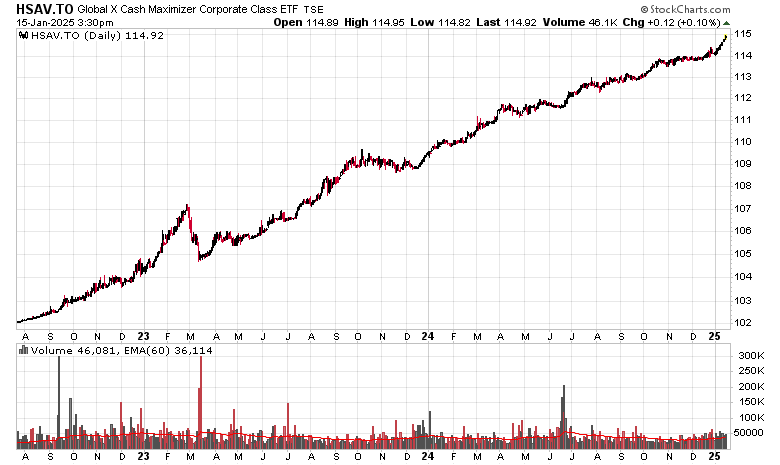

Quite some time ago the ETF sponsor decided it would no longer sell units of the ETF because the accumulation of assets would exhaust their ability to write off expenses amongst the whole ETF class. As a result, the market price of the ETF has always had a floor price (where the ETF would repurchase units below NAV) but there was no theoretical ceiling.

The premium to NAV has oscillated between close to NAV to ridiculously high premiums above NAV and these swings have been quite unpredictable.

Currently the premium to NAV is about 90 cents (NAV at $114.03 and market price of $114.93 as I write this), which represents approximately 101 days of interest accrued – i.e. if you invested at $114.93 and the price collapsed to NAV immediately, you would have to wait 101 days before the ETF broke even.

You can generally see the moments where HSAV has traded well above NAV by looking at the trendline – noting that as Bank of Canada interest rates have decreased over the past half year that the slope of the increase of the NAV has correspondingly decreased:

What was an interesting time was in the winter of 2023, where the ETF was trading over $2 over NAV and this was over 5 months’ interest – anybody investing in this ETF at 107 (late February 2023) had to wait about five months before they could break even.

I don’t know how much higher this can go, but it really makes you wonder who is bidding up what should ordinarily be a very boring ETF!

I will also note the US currency counterpart (TSX: HSUV.u.TO) is trading a couple pennies above NAV and has only rarely exhibited this characteristic of trading more than a month of interest above NAV.