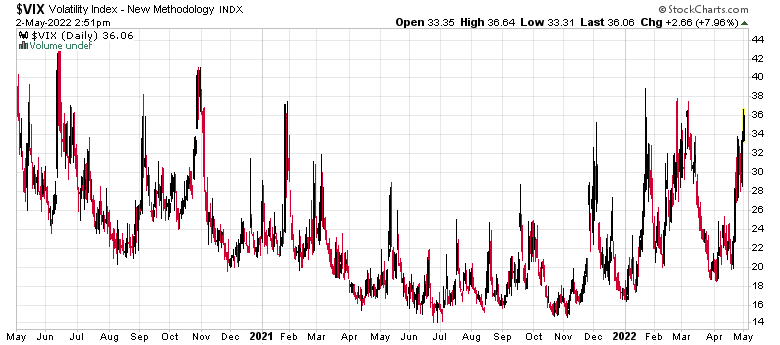

The jaw-boning of the central banks (every word out of the Bank of Canada and Federal Reserve are both to the tone of interest rates to rise forever) have finally had their desired impact – a suppression of demand in the asset markets, which will likely transmit itself to the overall economy, lessening inflation rates.

They’ll probably shut their mouths at some point in time when enough damage has been done. This is reminding me of the trading that occurred during the year 2000 in the Nasdaq – an incredibly volatile year, and the Federal Reserve at that time had the issue of how to withdraw its liquidity stimulus that it pumped into the market in 1999 (remember Y2K?).

Most of the technology starlings, including Shopify (TSX: SHOP), and the like are all sharply down over the past half-year. Psychologically speaking, for those that have held the stock anytime from April 2020 to today, they are now underwater. For those that bought in 2021, they are down roughly 75% on average. How much pain can they take before cutting out?

This is the challenge of investing in companies with projected cash flows in the far future – with Shopify, you have to take a shot in the dark as to when you’ll actually achieve a return on investment (i.e. the company generates positive cash flows which can be subsequently distributed to investors):

This re-rating of Shopify’s future non-earnings, coupled with the speculatively suppression of higher interest rates, clearly has had a very negative effect.

I am just picking on Shopify because it is Canadian, but this is also exhibited by all sorts of other technology darlings of the past. Today, for example, Palantir (PLTR) has been hammered 20%, on the basis of a very tepid quarterly earnings report (which more or less reported a break-even quarter which had all sorts of ‘adjustments’ to claim a positive free cash flow balance).

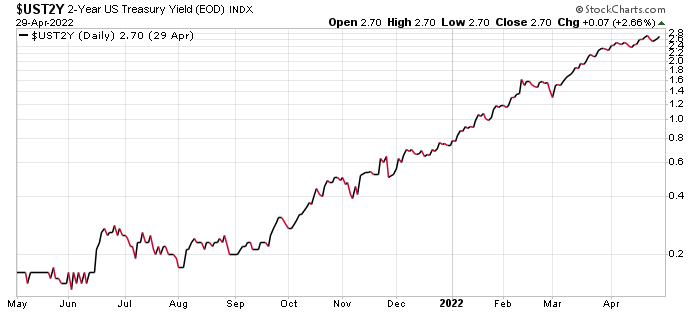

Don’t get me started on the effect of rising interest rates on cryptocurrency, where you’re going to have every investor on the planet realize that Bitcoin has a carrying cost (why hold onto BTC for zero yield when you can give your money to the Bank of Canada for a year and get 2.5% out of it for nothing?). You don’t hear too much about the scarcity of available Bitcoins these days! We’ll see if Michael Saylor at Microstrategy (MSTR) is forced to liquidate his stack of 129,218 Bitcoins and if so, that will be the margin call of the year for sure. One look at MSTR’s balance sheet and you do not need to be a Ph.D in corporate finance to figure out that his leverage situation is even more precarious than Elon Musk’s reliance on Tesla stock being sky-high.

In these environments, however, the best cliche used to describe things is that babies get thrown out with the bathwater. There are companies out there in the technology field which get lumped in with all of the ETF selling (go look at the holdings of ARKK here!) that do have value (beyond the obvious such as the Microsofts of the planet which will continue to have vast earnings potential due to their wide moats).

However, current free cash flows speak volumes. Companies trading under 5 times free cash flows are going to make mints for their shareholders by continued purchases of their own equity, and for those companies generating cash, shareholders should be cheering for continued lowering prices to generate excess future returns. Those that have prudently managed their balance sheets will be in a much better position to be opportunistic.

Finally, a word for those thinking that commodity investing is a one-way ride – in markets, nothing ever is! Yes, this includes Toronto residential real estate. There has been a lot of what I call ‘energy tourists’ and they have latched onto many of these stocks during earnings time (fossil fuel companies in Q1 have reported insane amounts of profits). There is an urge by many to over-trade and to shift portfolios away from quality into more speculative names (various < 50,000 boe/d with operations of more questionable characteristics) in order to torque up their return profiles. In a rising market, it is the lower quality companies that tend to exhibit the higher percentage gains, while in a flat or declining market, it is the quality firms that will have the sticking power. Stick with quality. It will let you sleep better at night in times like these, much more so than a pre-build contract for a 450 square foot Toronto condominium.