The problem with having a huge amount of anticipated growth baked into your stock price is that the expectations become incredibly difficult to achieve.

High expectations result in high stock prices.

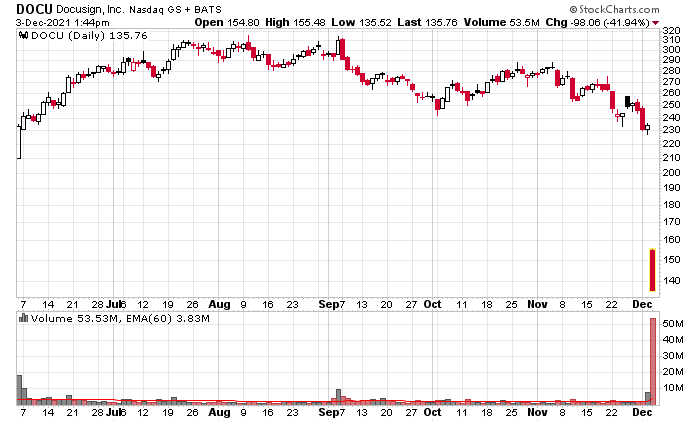

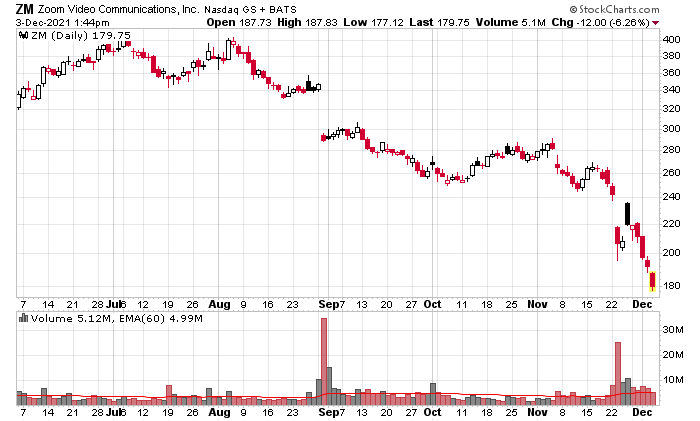

I’ll post the charts of two of these companies which are household names – Zoom (Nasdaq: ZM) and Docusign (Nasdaq: DOCU):

We will look at Zoom first.

At its peak of $450/share, Zoom was valued at around $134 billion. Keeping the math incredibly simple, in order to flat-line at a terminal P/E of 15 (this appears to be the median P/E ratio of the S&P 500 at the moment), Zoom needs to make $9 billion a year in net income, or about $30/share.

After Covid-mania, Zoom’s income trajectory did very well:

However, the last quarter made it pretty evident that their growth trajectory has flat-lined. Annualized, they are at $3.55/share, quite a distance away from the $30/share required!

Even at a market price of $180/share today, they are sitting at an anticipated expectation of $12/share at sometime in the future.

Despite the fact that Zoom offers a quality software product (any subscribers to “Late Night Finance” will have Zoom to thank for this), there are natural competitive limitations (such as the fact that Microsoft, Google and the others are going to slowly suck away any notion of margins out of their software product) which will prevent them from getting there.

The point here – even though the stock has gone down 60% from peak-to-trough, there’s still plenty to go, at least on my books. They are still expensive and bake in a lot of anticipated growth which they will be lucky to achieve – let alone eclipse.

The second example was Docusign. Their great feature was to enable digital signing of documents for real estate agents, lawyers, etc., and fared very well during Covid-19. It’s an excellent product and intuitive.

They peaked out at $315/share recently, or a US$62 billion valuation. Using the P/E 15 metric, the anticipated terminal earnings is about $21/share.

The issue here is two-fold.

One is that there is a natural ceiling to how much you can charge for this service. Competing software solutions (e.g. “Just sign this Adobe secure PDF and email it back”) and old fashioned solutions (come to my office to scribble some ink on a piece of paper) are natural barriers to significant price increases.

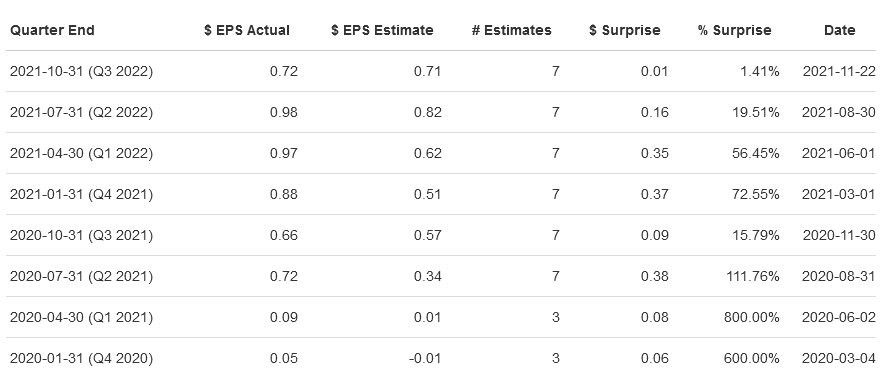

Two is that the existing company doesn’t make that much money:

Now that they are reporting some earnings, investors at this moment suddenly realized “Hey! It’s a long way to get to $21!” and are bailing out.

Now they are trading down to US$27 billion, but this is still very high.

There are all sorts of $10 billion+ market capitalization companies which have featured in this manner (e.g. Peleton, Zillow, Panantir, etc.) which the new investors (virtually anybody buying stock in 2021) are getting taken out and shot.

This is not to say the underlying companies are not any good – indeed, for example, Zoom offers a great product. There are many other instances of this, and I just look at other corporations that I give money to. Costco, for example – they trade at 2023 anticipated earnings of 40 times. Massively expensive, I would never buy their stock, but they have proven to be the most reliable retailer especially during these crazy Covid-19 times.

As the US Fed and the Bank of Canada try to pull back on what is obviously having huge negative economic consequences (QE has finally reached some sort of ceiling before really bad stuff happens), growth anticipation is going to get further scaled back.

As long as the monetary policy winds are turning into headwinds (instead of the huge tailwinds we have been receiving since March 2020), going forward, positive returns are going to be generated by the companies that can actually generate them, as opposed to those that give promises of them. The party times of speculative excess, while they will continue to exist in pockets here and there, are slowly coming to a close.

The super premium companies (e.g. Apple and Microsoft) will continue to give bond-like returns, simply because they are franchise companies that are entrenched and continue to remain dominant and no reason exists why they will not continue to be that way in the immediate future. Apple equity trades at a FY 2023 (09/2023) estimate of 3.8% earnings yield, and Microsoft is slightly richer at 3.2%. Just like how the capital value of long-term bonds trade wildly with changes of yield, if Apple and Microsoft investors suddenly decide that 4.8% and 4.2% are more appropriate risk premiums (an entirely plausible scenario for a whole variety of foreseeable reasons), your investment will be taking a 20% and 25% hit, respectively (rounding to the nearest 5% here).

That’s not a margin of error that I would want to take, but consider for a moment that there are hundreds of billions of dollars of passive capital that are tracking these very expensive equities. You are likely to receive better returns elsewhere.

Take a careful look at your portfolios – if you see anything trading at a very high anticipated price to cash flow expectation, you may wish to consider your overall risk and position accordingly. Companies warranting premium valuations not only need to justify it, but they need to be delivering on the growth trajectory baked into their valuations – just to retain the existing equity value.