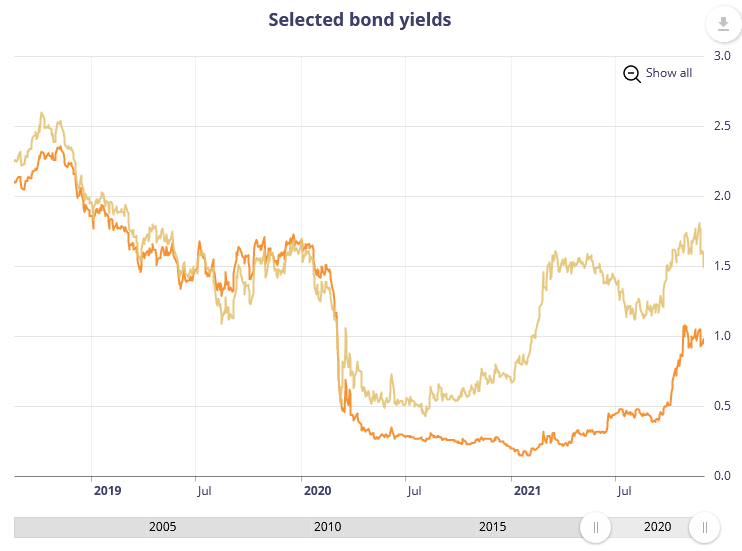

Light yellow line is the 10-year Government of Canada bond yield, orange line is the 2-year bond yield:

Over the past week, Omicron fears have triggered a huge demand for long-dated government debt, while central bank talks of tapering have pushed the front end of the yield up.

Indeed, when looking at the BAX futures, we have the following curve (for those that are unfamiliar, these are 3-month bankers’ acceptance futures, of which you derive the rate by going 100 minus the anticipated yield percentage, so a 98 would be equal to 2.00%):

BAX – Three-Month Canadian Bankers’ Acceptance Futures

Last update: December 5, 2021

| Month | Bid price | Ask price | Settl. price | Net change | Open int. | Vol. |

|---|---|---|---|---|---|---|

|

Open interest: 1,173,941

Volume: 145,981

|

||||||

| December 2021 | 99.455 | 99.460 | 99.460 | -0.005 | 136,604 | 34,223 |

| January 2022 | 0 | 0 | 99.380 | 0 | 0 | 0 |

| February 2022 | 0 | 0 | 99.220 | 0 | 0 | 0 |

| March 2022 | 99.080 | 99.095 | 99.105 | -0.015 | 242,041 | 25,545 |

| June 2022 | 98.660 | 98.665 | 98.690 | -0.030 | 185,438 | 16,971 |

| September 2022 | 98.335 | 98.340 | 98.360 | -0.025 | 167,920 | 15,778 |

| December 2022 | 98.125 | 98.140 | 98.150 | -0.015 | 144,759 | 17,816 |

| March 2023 | 97.985 | 97.995 | 98.010 | -0.020 | 107,855 | 13,145 |

| June 2023 | 97.865 | 0 | 97.890 | -0.020 | 62,554 | 10,228 |

| September 2023 | 97.795 | 97.840 | 97.820 | -0.025 | 69,061 | 6,586 |

| December 2023 | 97.510 | 97.820 | 97.805 | -0.020 | 38,357 | 4,960 |

| March 2024 | 0 | 0 | 97.780 | -0.005 | 12,729 | 386 |

| June 2024 | 0 | 0 | 97.775 | -0.010 | 4,613 | 181 |

| September 2024 | 0 | 0 | 97.790 | -0.005 | 2,010 | 162 |

The spot price is at 0.54%, while the December 2022 future is at 1.85%, which implies that in the next 12 months we will have a rate increase of about 125bps the way things are going.

The 2-year government bond is yielding 0.95% as of last Friday. Using expectations theory, this is roughly in-line, but functionally speaking, the inversion of the yield curve is going to signal some ominous signs going forward.

Central banks are engaging in the tightening direction because of fairly obvious circumstances – there are leading indicator signs of inflation everywhere (labour market tightness AND the inability to find quality labour both count; the first is easily quantified, while the second one is not, and is a very relevant factor for many businesses), input costs rising or even being completely unavailable, energy costs spiking, etc. With governments flooding the economy with deficit-financed stimulus, it is creating an environment where no realistic amount of money thrown at a problem can stimulate productive output.

My guess at present is that tapering and rate increases will go until the economy blows up once again – the evaporation of demand will be mammoth – when these supply chain issues are resolved, the drop-off in demand will commence very quickly. It will likely happen far sooner than what happened in the 4th quarter of 2018 (the US Federal Reserve started shrinking its balance sheet of treasuries at the end of 2017 and the vomit started occurring around October 2018). Indeed, you even saw hints of this economic dislocation occur in late 2019 – there was likely going to be an economic recession in 2020 even if Covid-19 did not occur. Covid instead just masked the underlying conditions, and stimulative monetary policy coupled with shutdowns of global logistics and labour disruptions was the subsequent excuse when fundamentally things were already in awful shape to begin with.

This means that portfolio concentration (other than not being leveraged up the hilt) should be focused on non-discretionary elements of demand.

These are not serious suggestions, but Beer (TAP), Smokes (MO) and Popcorn (AMC… just kidding!) will probably be the last industries standing among the carnage. Even McDonalds (MCD) will not be spared as less and less will be able to afford the $10 “extra value” meals as central banks continue to drain the excess, but Dollarama (TSE: DOL) will thrive.

The conventional playbook would suggest that commodities would fare poorly with a precipitous decline in demand, but this is one of those strange interactions between the financial economy and real economy where hard assets will initially lose value in the face of interest rate increases (this has already happened), but the moment the central banks have stretched the rubber band too hard and it snaps, commodities likewise will be receiving a huge tailwind.

2022 is surely to be a worse year for most broad market investors and the public in general. Returns are going to be very constrained and P/E expansion will be non-existent (other than by reduced earnings expectations!). Watch out, and hold onto your wallets. There will be few that will be spared.

Bank of Canada today reported a “status quo” interest rate release, there was some slight expectation of a mild tapering of QE; December 2022 BAX futures are still at 98.14 (1.87%) although they were 7bps lower yesterday.