I unintentionally made an investment in an AI company. You can read my original thesis on May 27, 2020. Like most companies around that time, it was trading heavily down during the Covid crisis. Indeed, my intentions were everything other than investing in AI at the time.

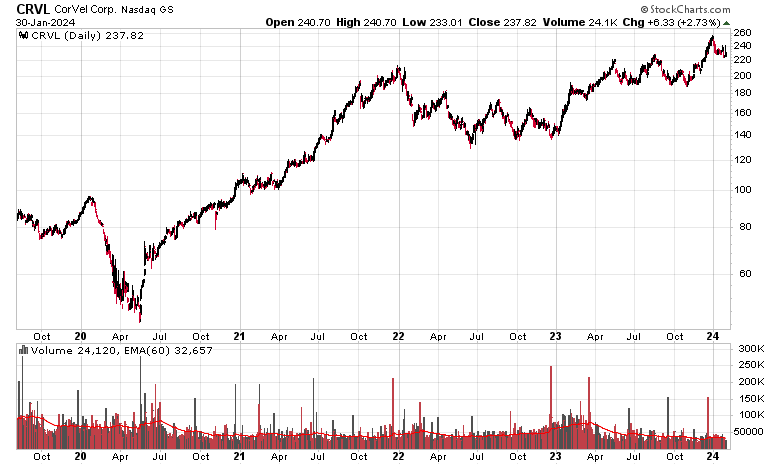

Fast forward nearly four years, the stock has rocketed upwards to valuations that are difficult to rationalize.

The company is operated by a reclusive management and they have very terse press releases. They quit doing their no-question conference calls (which gave slightly more colour to their business operations) after their January 2023 quarter. No analysts follow the company, there are no EPS estimates, and almost nobody knows that this company has a huge competitive advantage in its niche.

Amusingly, I have noted they have been using the two-letter “AI” phrase in the last few press releases.

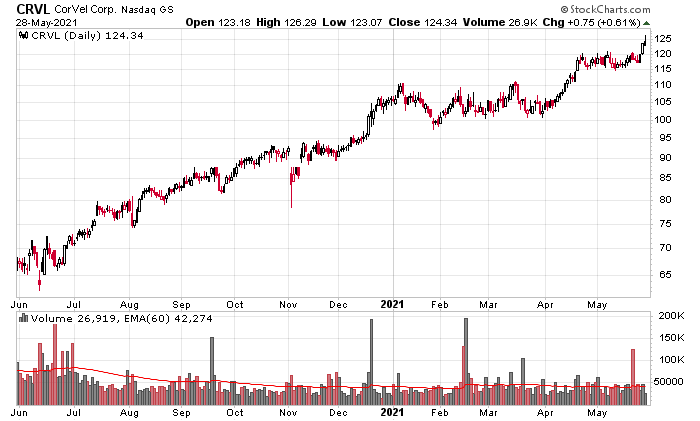

On May 27, 2021, they first used the words “artificial intelligence” in their press release:

CorVel Corp. applies technology including artificial intelligence, machine learning and natural language processing to enhance the managing of episodes of care and the related health care costs. We partner with employers, third-party administrators, insurance companies and government agencies in managing workers’ compensation and health, auto and liability services. Our diverse suite of solutions combines our integrated technologies with a human touch. CorVel’s customized services, delivered locally, are backed by a national team to support clients as well as their customers and patients.

January 31, 2023:

The Company has also continued work in the area of digital transformation. Most recent efforts have focused on enhancing CorVel’s document repository system with AI-centric technologies. The advancements being implemented automate the extraction and codification of critical data, which can then be leveraged dynamically within systems. The development roadmap for the quarter and beyond includes increased automation and augmentation, which will further optimize bottom-line results and outcomes.

May 25, 2023:

In other areas, CorVel is moving forward quickly and intentionally, using generative AI in a closed-source data environment. The technology will be incorporated into CogencyIQ® service offerings and has extensive benefits. Most importantly, generative AI will elevate the work of claims professionals and allow more time to be spent interacting directly with injured workers. The reallocated time will ultimately improve the experience of injured workers and enhance partner outcomes.

August 1, 2023:

CorVel’s 1st generative AI initiative will be released in the September quarter. The release will reduce mundane, repetitive tasks and provide decision support at critical inflection points. This automation will add to the existing machine-learning tools with increasing capabilities within the system. The Company also views generative AI as an effective tool to mitigate labor challenges and provide guidelines for future generations of professionals. In the quarter, investments in the foundational systems and workflow processes continued to strengthen the results achieved with CorVel’s products and services.

October 31, 2023:

In the payables market, developments were made in both the revenue cycle management arm, Symbeo, and the treasury services department. At Symbeo, hyperautomation, a combination of AI, machine learning, and robotic process automation technologies, presents an expanded opportunity in the market. By using Symbeo’s payable solutions, partners receive the benefits of touchless digital invoices, AI enabled optical character recognition, a machine learning Document Classification model, configurable AP rules, and standard ERP integrations via Robotic Process Automation which provides faster invoice cycle times, lower total cost of ownership, and an enhanced user experience.

Finally, today, on January 30, 2024:

The implementation of generative AI initiatives has been proven to boost the efficiency and effectiveness of both the P&C and Commercial Claims teams. These updates have gradually reduced time spent on routine tasks, thus creating more time for essential activities that require critical thinking, directly impacting the user experience and results achieved.

…

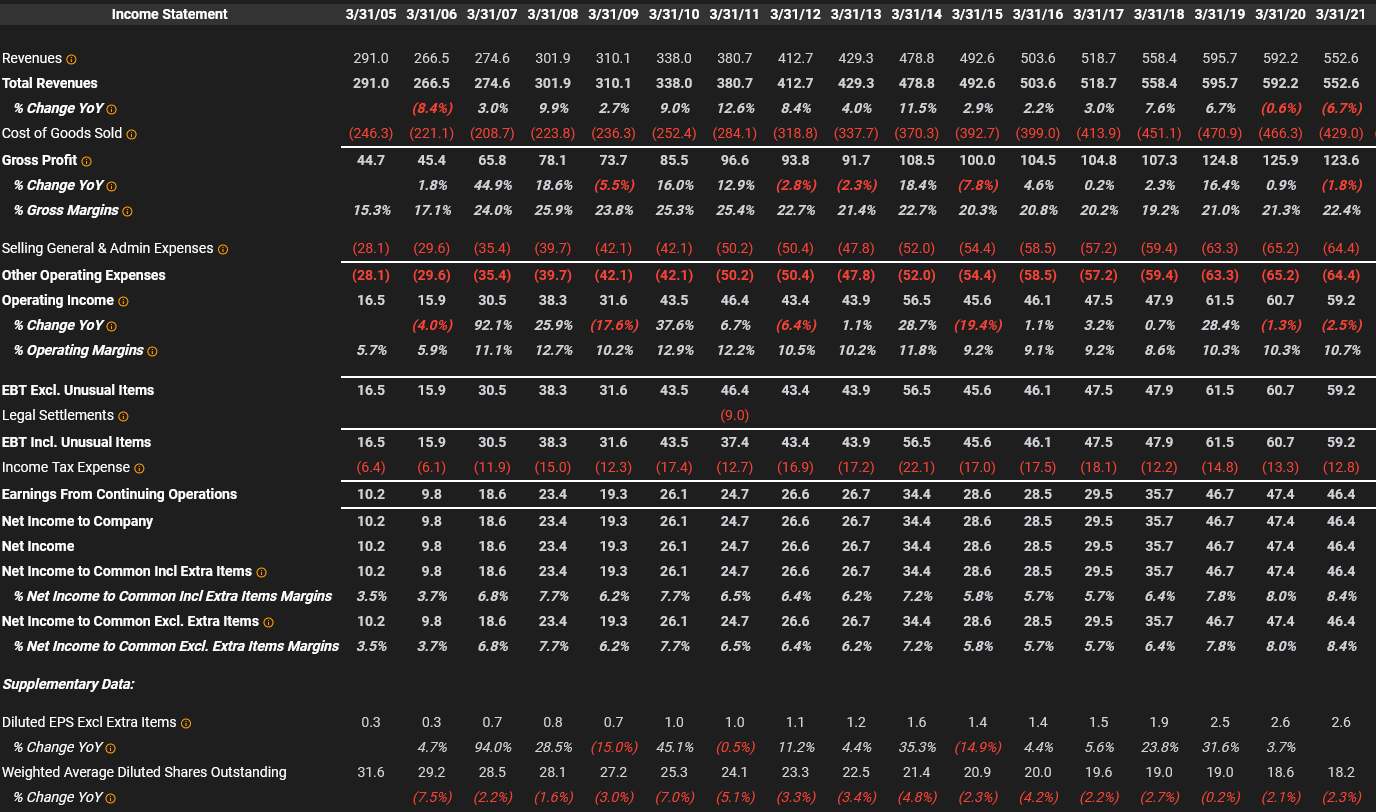

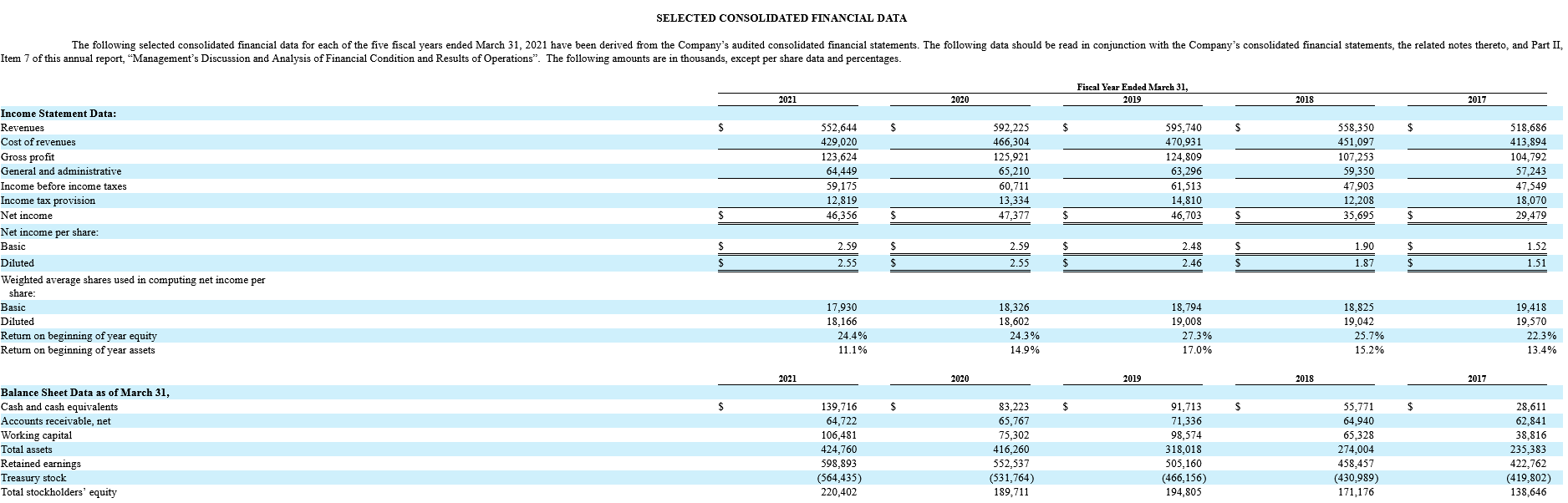

With today’s earnings release (the 3rd fiscal quarter for the company), we have a past 12-months EPS of $4.32/share. The company historically has been able to slowly increase its per-share earnings both through a combination of higher net income and also through the deployment of a significant share buyback program which has been running for a couple decades – the capital allocation strategy appears to be holding about $100 million cash in the bank and dumping the rest of the free cash flow into buying back shares. While the company has been able to reduce its shares outstanding by 139,000 shares from December 2022 to 2023, much of the $55 million spent was to offset prior option issuances. Needless to say, with the stock price as high as it is, those equity options are all entirely in-the-money.

Focusing on the $4.32/share, this gives a backward-looking P/E of 55, which makes Corvel the richest (highest valuation) stock I currently own. The valuation has me concerned, but I can easily see a scenario where for some reason the hype decides to bid it up even further. It is very difficult to predict these things. Who is to say that the capitalized value of their software technology is not worth well greater than the $4 billion market cap? Maybe some insurance giant wanting to internalize their own software operations (and de-licensing competitors) would be a strategic bidder for $8 billion in stock? My guess is about as good as anybody else’s.

While this is still a top-5 in my portfolio, I did pare a little at the 200 level to justify my sanity a little bit. But instead of chasing Nvidia, I will take solace in this – at least the company itself is set to generate cash for a very, very long time.