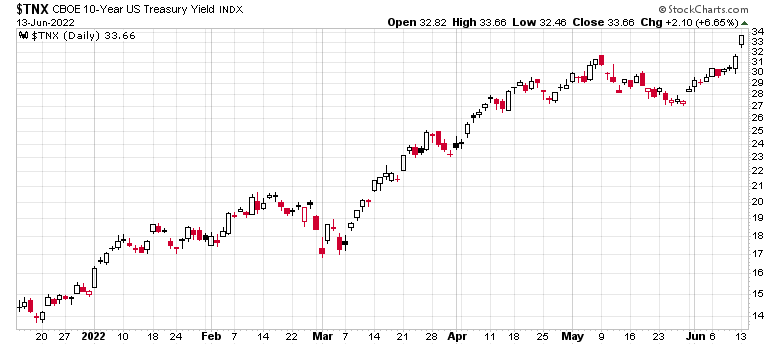

The rules change in a tightening monetary policy environment. We saw shades of this in the second half of 2018 when the US markets started to vomit over QT and increasing interest rates, and to a lesser degree this happened to Canada.

Recall that the S&P 500 in 2019 very roughly averaged price levels that are about 25% below where it is currently trading at. When factoring in monetary debasement, one can surmise that a “2019 neutral” level would be somewhere around 3,500 but this was with much better economic conditions, coupled with a justification for a sky-high P/E ratio due to extremely low interest rate levels. The average 30-year bond yield in 2019 was lower than it is currently trading at. A more realistic level, all things being equal, would be around the 3000-3200 level (20% lower than present).

Fast forward to 2022 and we are seeing shades of late 2018 – although of course the big difference is that in 2018 central banks could reverse course because inflation back then was at a manageable level. The mandate for higher interest rates is omnipresent with the latest CPI print out of the USA at +8.6% and the latest CPI snapshot in Canada will be released in June 22 and indications definitely suggest it will be up there.

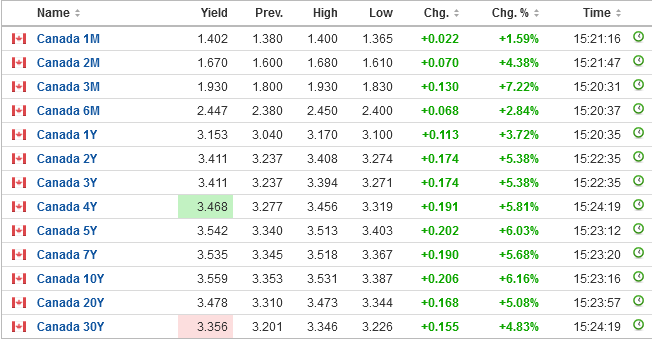

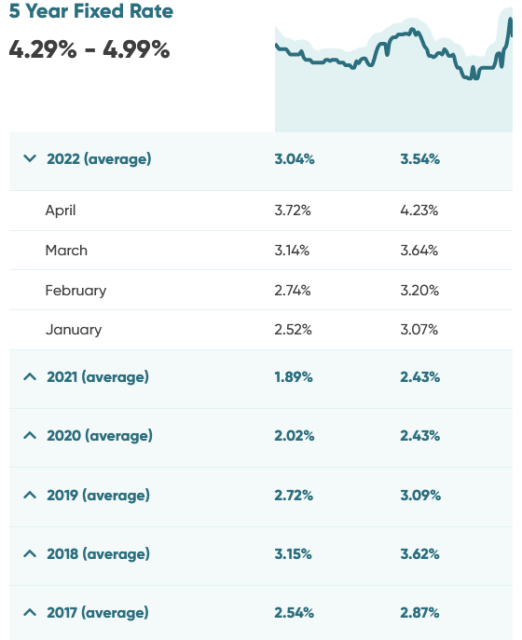

What is particularly damaging in Canada is the spike in mortgage rates. This is going to kill credit in the real estate market:

The 5-year fixed rate is the most common form of mortgage, and from June 2017 (2.4%) to June 2022 (4.3%) is a 190bps increase.

What does this mean in reality? Let’s say in June 2017 you took out $1M in credit financing at 2.4%, with typical terms (25-year amortization). At the end of June 2022 you would be sitting at an $845k balance after making $53.2k yearly payments.

You go and renew this $845k balance at 4.3%, for a 20-year amortization, and you will be paying about $59.5k/year for the next five years – about $528/mo out of your pocket.

Credit has gotten much more expensive. People can mitigate this with a variable rate mortgage, but the Bank of Canada has made it crystal clear that short-term rates will be going higher. For how much longer – who knows. There are conceivably scenarios where if central banks can not get a hold of inflation that short-term rates will be going considerably higher than the so-called “neutral” rate target of roughly 3%. If this occurs, variable-rate mortgages will be under increasing stress.

The point of the above exercise is that unless wages increase dramatically, available credit to be dumped into the real estate market is going to be more expensive and this will be depressing the prices of housing going forward. Since construction is a significant component of urban economic activity, this activity will likely be slowing down as a result – once projects complete, that will be it.

The disaster scenario is that unemployment will spike and you start seeing waves of selling due to foreclosures. It is a scenario that is the big fear for Canada’s mortgage insurers (CMHC and formerly Genworth, now Sagen owned by Brookfield) where you start seeing underwater mortgages. The Bank of Canada is clearly looking at these economic scenarios and I do suspect there is an element of a “Macklem put” in play here – the country simply cannot afford to have a mass collapse in real estate pricing.

Negative economic reverberations would hit the commodity markets as well and higher rates will be triggering this. This is going to make equity picking in the commodity market much more trickier than it has been in the past 24 months.

Even if raw commodity prices take a 25% dip from present prices (e.g. spot WTI from $120 to $90, spot natural gas from $9 to $6.75, etc.), most Canadian (edit one day later: forgot to include a very important word here: ‘energy’) equities are still well positioned to make historically large amounts of free cash flows. However, sustaining capital expenditures will inevitably get more expensive and profitability will diminish, albeit will still be ample. There is likely going to be price volatility as the market grapples between the notions of total returns (their total returns will likely be much higher than companies in other sectors), coupled with pricing in a potential future downslope of raw commodity pricing – essentially pricing the walking down of the futures curve. December 2022 oil is $107.50 as I write this, while December 2025 oil is $74.75. Clearly if spot demand is higher, then existing producers are able to claim the surplus and hedging becomes expensive.

However, the capitalization of future profits (as determined by existing market prices) will continue to gyrate. For companies that are actively involved in share repurchases, these dips are probably more welcome opportunities and shareholders will inevitably be staying at least afloat while the rest of the market continues to tank. However, capital appreciation from this point is not going to be easy – most of the returns will be of the total return type. As I illustrated with an earlier post about Birchcliff, I don’t believe that an investor should be banking on share appreciation, but rather they will be receiving a high dividend stream – in the case of BIR, a healthy double-digit return of cash at the current market rate of $11.75. As raw commodity prices fluctuate, you will see this deviate up and down and this will make for a difficult price environment where, as the title says, the next 10% is going to be very difficult. Getting out of debt and holding ample supplies of cash is going to make people feel very comfortable in this environment.