Sacha,

How do you think the oil party will play out, with 50% of lost US production has been recovered (pre covid peak of 13.1 mbbl/d to trough of 9.7 mbbl/d and now sitting at 11.5 mbbl/d) and super majors are going for the shale again. You see it over soon with another round of massive boom (volume wise, if not price)/ bust or players become better at managing prices in a goldilock where everyone makes decent money.

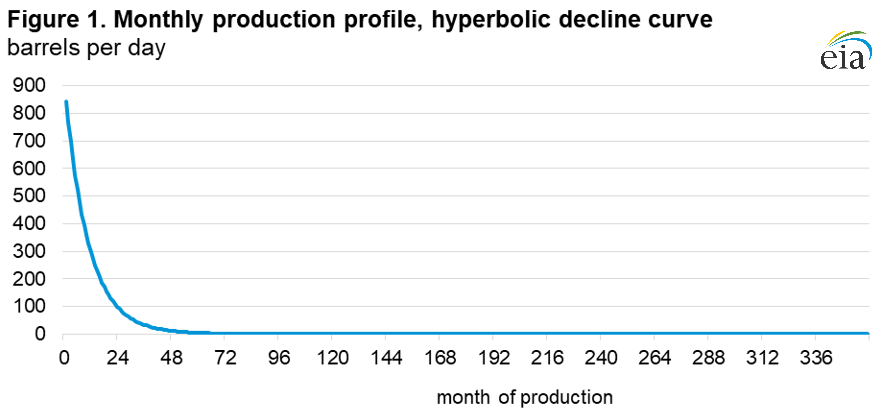

I don’t have much insight on what’s going on in the rest of the world. However, in the USA to maintain it will require a gigantic amount of capital investment and aside from the Permian Basin, most of the top tier geology has been tapped out. When you have 30% decay rates on 10 million barrels/day of production, each year you need to replace 3 million, and that’s a steep order.

You’re up against production declines like this:

What do I mean by “top tier geology”? When looking at a drill map that looks like the following (this is in the Bakken shale in North Dakota):

This is pretty much tapped out on the northwest of this specific map. I’ve seen other maps made elsewhere of entire regions being completely saturated like this.

Just like when picking fruit in an orchard, you go for the low hanging fruit first, and this is what happened in the resurgence of USA shale drilling over a decade ago. Now the geology has been tapped out – you can’t mine these areas again. They will still produce, but at much, much lower rates than the initial drill. Some of Peyto’s monthly reports get to this in detail.

Canada’s oil sands and in-situ (steam-assisted gravity drainage) projects have much better decline profiles. In addition, from what I can tell, our companies are being unusually conservative these days in terms of expanding capacity, especially these days when expanding capacity would be wildly profitable. While we do not have the power to move markets like OPEC, the apprehension is also faced elsewhere in the world, especially when there is gigantic amounts of ESG pressure (see: Exxon board election).

There will be a bust, but not right now. Demand is stronger than ever and the ability to meaningful ramp up supply is constrained. Any meaningful price drops in fossil fuels at this point will be on the demand side (the economic bust scenario), but even in 2020 when the world shut down for a couple months due to Covid, demand was estimated to be about 91 million barrels daily, down from about 100 in 2019.

I will also note that the measuring barometer of oil, the US dollar, should be taken into consideration. Everybody these days is forced to be a macroeconomist to properly invest in these crazy times.