I am going to review my writings of April 5, 2020, still a time when nearly 95% of the population was locked in their homes about fears of SARS-CoV-2. Of course, with any prognostications, you will get some right and get some wrong, but the material issues of the fallout of Covid-19 I got completely correct. There is a bit of back-patting in my current post but let’s take a look:

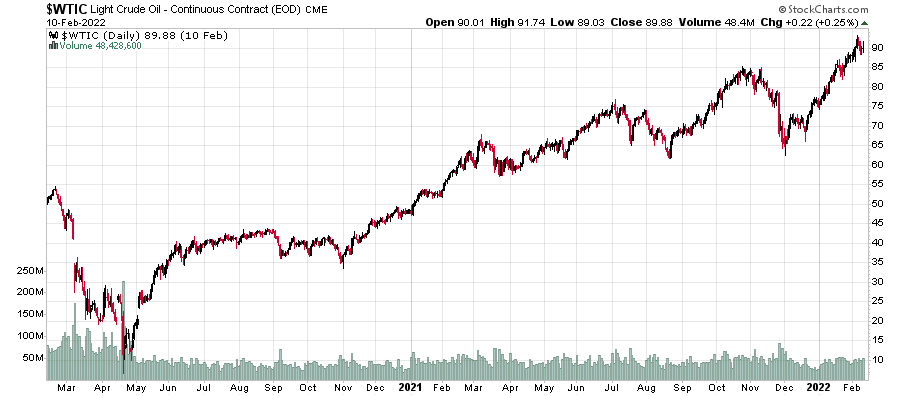

Oil in about nine months, maybe six or eighteen will skyrocket. The longer that oil is under $30/barrel, the further the bounce is going to be on the other end when supply/demand dynamics results in a supply imbalance. It probably wouldn’t be the worst of ideas to buy long-dated crude oil futures (December 2022 at US$38.75/barrel?).

Check! This is happening presently. By most accounts October-November 2020 was the non-panicked low for spot crude and after that it has been a pretty good ride up.

The after-effects of this [effective debt monetization] during the 2008-2009 economic crisis came in the form of asset inflation, but this time it will be different. With trade lines cut, it is pretty obvious that there is going to be some high-grade consumer inflation that will be coming. Not now, but in a year’s time, this will be a dominant message, especially with the pending increase in oil prices. Note this is not going to be Weimar Republic inflation, but it will be at rates that we will not have experienced in a long, long time. As a result, interest rates must rise.

My predicted timing was a little faster than reality, but this one is coming to roost. However! In a future post, I’ll give some colour to this.

Despite how dysfunctional the economy may seem to be, equities are going to be the only game in town, especially in a monetization situation. It will confound people that there will be such a disconnection between the stock market and the underlying economy

Check. Bonds, to put it mildly, have offered sub-par returns, and if you had invested in longer durations, you are in the red.

The statistic of “deaths” needs to differentiate between “deaths due to Covid-19” versus “deaths with Covid-19”. There is no practical way that these statistics will be obtained.

Check. The application of this has been totally manipulated for political communication purposes. Initially, it is deaths with Covid-19, and later on, some revisions of “because of Covid-19” when the message suits it. Don’t get me started on manipulations of cause-and-effect claims of vaccination statistics (efficacy and safety).

I always like to think of a “parallel world” example, where you see people lining up to get into the grocery store that are spread two meters apart, versus not having these measures in place – will the death and/or transmission rate truly be impacted in either scenario? Of course, ethics prevents double-blind testing, but I would think the effectiveness of some measures to enforce “social distancing” are completely for show – similar to some procedures that you see around airports in the name of security.

I think the (much attacked, just because the truth really hurts!) Johns Hopkins paper on non-medical interventions pretty much tells the story here. One paper does not constitute a proof, but from the spectrum of governmental responses (ranging from full-blown isolation to relatively open society), the course of the outcome inevitably is the same – you might be able to isolate in a cabin in the woods, but as soon as there is one instance of contact, good luck! (Antarctica, Kiribati Island) – SARS-CoV-2 cannot be contained in any semblance of a normal society. It’s out there, and you’ll get it eventually.

My opinion at present is that the current route that most world governments have taken on Covid-19 will cause more collective damage with stress and economic turmoil (and subsequent spinoff consequences of such) than caused by Covid-19 itself. Political pressure likely forced most democratic governments to shut down, while autocratic ones can put on a semblance of ‘back to normal’ just strictly through misinformation, like how China is basically getting back to work despite there being cases of Covid-19 (the one or two they report is just symbolic, while the actual numbers involved are likely much more). Their “confirmed case” count is likely understated by a magnitude of 10, but came to the conclusion that a lockdown was doing more harm than good.

While my prediction was completely correct that the response to Covid-19 will cause much more damage than the virus itself, the mistake I made here is the implicit assumption that governments (especially authoritarian ones) wanted to move past Covid-19 as quickly as possible. It has become a political tool in many jurisdictions.

And finally…

This might sound a little crazy, but I can see the S&P 500 heading to 4000 before the end of the year.

It was around 2500 when I posted this. Predicting a major index will rise 60% in 9 months is the definition of insanity. Indeed, this was an incorrect call, but it did get up to about 3800 by years’ end.

My main point here, other than a bit of chest-thumping, is to successfully invest you need to have some sort of idea where things are headed, and also know if this is a consensus opinion or not. My opinions in early April 2020 were very much out of consensus at the time and the logical course of action were to proceed on it with a “real world economy”-heavy portfolio.

It’s been almost two years since all of this mania has occurred, and the world is changing once again. In an upcoming post, I’m going to describe what I call “the turn”.

Agreed…My most profitable 2 yrs by a long shot

Chest-thumping well earned Sacha. With a similar investment approach, although somewhat more accepting of gov’t initiatives taken, 2021 was second only to 2008 for me.