I’ve been on radio silence lately. There hasn’t been much to write about although I am noting the ‘vapour equity’ market has seen considerable supply pressure this month.

The peak of the dot-com boom (at least as far as the stock market was concerned) was in February of 2000 when the Nasdaq peaked to 5000 and you had a whole avalanche of initial public offerings, the most notable one was the IPO of Palm (which was owned by 3Com at the time).

After that it went pretty much downhill as valuations were not supported and liquidity was sucked out of the markets. Old-value stocks (a good example being Berkshire, but pretty much any company with genuine profits that had nothing to do with fibre optics, dot-com networking or e-commerce) managed to keep their value, and in many cases some thrived in the ensuing carnage.

Investors in 2000 that kept their portfolio away from the previous high-flyer sectors would have survived to participate in the next run-up (which, in the USA, was anything related to real estate). Indeed, a successful investor across multiple market cycles must know which sectors to avoid at any given time – clearly taking permanent capital losses (anybody invest in Pets.com? EToys? CMGI?) depletes your ability to invest going forward.

We fast forward to today, where technology, software and anything related to Covid (virtual work facilitation, vaccines, etc.) is plummeting.

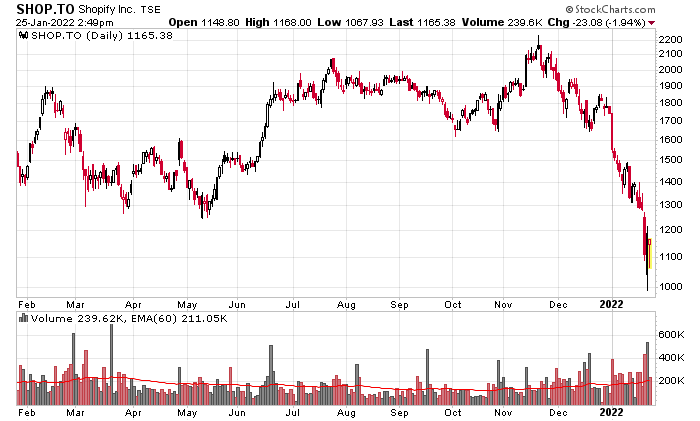

There is a lot to review, but I will keep things to Canada. There’s a lot more going on in the USA (e.g. anything that ARKK owns, for example). Anyhow, the most prominent casualty is the high-flyer Shopify (SHOP.TO), which used to be the #1 ranking in the TSX index, but no longer! They’re now back to #3 below Royal Bank and Toronto Dominion.

In the span of 2 months, they traded at a peak of CAD$2,200/share and are now down to about CAD$1,100, which is a peak-to-trough of 50%. Anybody invested in the company since June of 2020 would have lost money. Imagine if you had bought shares of this thing at $1,800 and now a third of your capital has vanished…

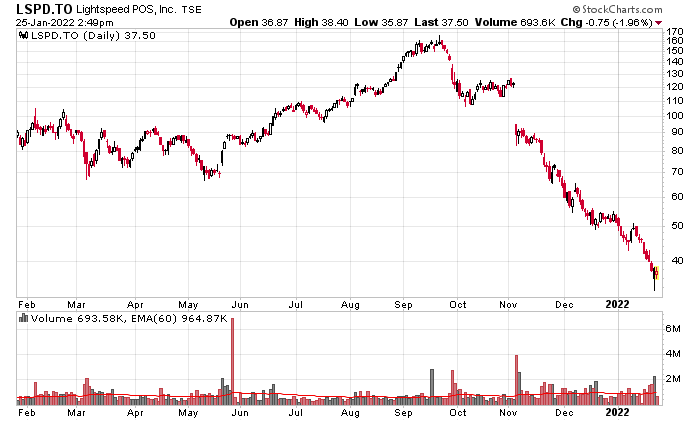

Another high-flyer has been Lightspeed POS (LSPD.TO):

The peak-to-trough ratio here has been even more extreme – from $160/share to about $37 today – a 77% drop.

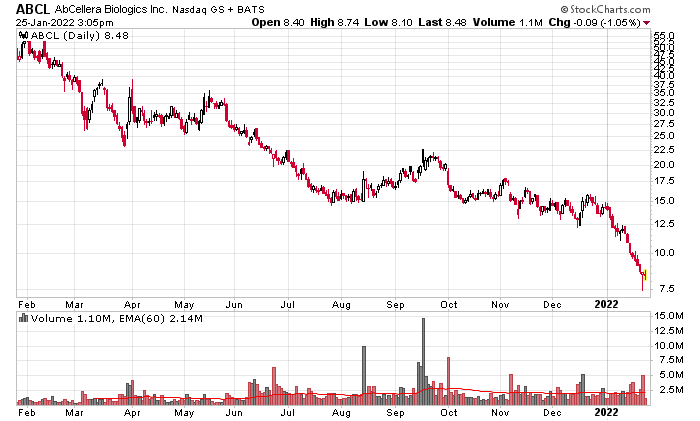

Another highly touted IPO was AbCellera (Nasdaq: ABCL) – a Canadian company that IPOed on the Nasdaq. They went public at US$20/share and traded as high as US$70 on the day they went public, but since then it has been a decline down to $8.50 today – nearly a 90% peak-to-trough loss.

Looking at some other recent TSX IPOs we have, starting September 2021:

CPLF

PRL

QFOR

DTOL

EINC

CVO

Bringing up the charts of all of them, it’s not a pretty picture. One other notable broken IPO I examined in the past was Farmer’s Edge (TSX: FDGE) and they are down about 85% from their IPO. Another one which I didn’t write about but was an obvious avoid in my books was Eupraxia (TSX: EPRX) which I have to commend the underwriters for vomiting out that firm to unsuspecting retail shareholders.

There’s a few lessons to take home here, but one obvious lesson is that just because something has dropped by 50% or 80% doesn’t mean it is still ‘cheap’.

Many of these high-flyers that make headlines are trading at ultra-premium valuations. Take Shopify – down 50% peak to trough. While the company makes money it is still nowhere near a reasonable multiple of its existing market valuation. An investor is still paying a huge premium for assumed future growth – and the company has to exceed this in order for an investor to get a payout (never mind a dividend!).

Even in the case of companies like Lightspeed that are down 80%, it is very difficult to determine whether an investor will be seeing any returns at the end of the day – they are still losing money in their operations.

Many people got their start in investing during the Covid-19 era. A lot of them caught the right stock at the right time (e.g. Gamestop) and probably started having dreams of trading their way to riches. Without the underpinnings of understanding the fundamentals of companies, inevitably these hordes of retail investors simply traded companies on the perception of sentiment rather than any earnings power. Without having a general idea of an entry and exit point, one could rationalize GME at $100, $200, $300, etc., or Shopify at $1,500, $1,700, etc., and are effectively trading blind. One can also make a similar argument for cryptocurrency markets – functionally a zero sum game.

A good question for these new traders is – do they have the discipline to get out? Or will they try to hold on and “break even”? Or will they average down as these high-flyer shares crash back down to earth? If the 2000-2003 model is similar this time around, there will be a lot of people that will be holding onto ever depreciating shares and the current wave of hype will come to a close.

Keep in mind the simplicity that math offers – if something goes from $100 to $50, there is a 50% decrease in value. If you purchase at $50 and it goes down to $25, the result is the same – a 50% loss (and if you were starting at $100, that’s a 75% loss). In many of these cases the companies’ trajectory will head to zero, and it doesn’t matter what “discount to the 52-week high” you purchase the stock at, you will face losses if/when it heads to zero.

The safety in the markets are in those companies that are producing sustainable cash flows. You will still take a considerable hit if the company in question is trading at a very high multiple. The maximum safety are in those companies trading at low multiples to cash flows and those that are not reliant on renewing excess amounts of debt financing. There isn’t a lot of safety out there, but astute readers on this site have picked up hints here and there as to what offers a degree of safety.

“Anybody invested in the company since June of 2000…”, maybe 2020? 🙂

Thanks for the correction. I don’t even know what decade I’m living in anymore it seems!

Great post!

From what I see on twitter, people will average down on these high flying stocks. In the past week, I have probably seen at least 10 tweets stating buying SHOP here is a generational buying opportunity. Buying the dip has been ingrained in people’s minds and I agree with you on retail “traders” getting into the markets during covid. They have never seen a market go down.

I think the problem today is inflation. The fed can’t back down but I don’t think they will raise rates aggressively enough to choke off inflation. Small raises here and there but that will cause inflation to get worse. Do you think they raise aggressively?

The amount they can move around is limited. The last time they tried this in 2017 it took them about a year and a half of quarter-point increases to crash the stock market. Back then they still had the luxury of not having to deal with too much CPI inflation. This time around things are much less favourable. I would view it more likely that they would start pulling out monetary excesses off the balance sheet in conjunction with quarter rate increases and see what happens. This is the reverse of what they tried in 2017-2018 (they raised the rates first in 2017 and then started to run the assets off the balance sheet in 2018).

But in either case, I see it difficult to see how they can avoid really plummeting the speculative end of the asset markets. It appears that QE and “modern monetary theory” has reached their limits.

… difficult to see how they can avoid really plummeting the speculative end of the asset markets

Preventing this outcome is not part of their mandate, except of course to understand the implications of the crash for general monetary stability. The Fed and other modern CB’s mandates are to protect faith/trust in the monetary system. They do this by being open and transparent and doing whatever it takes to prevent high inflation AND deflation. More recently, mandates have been expanded to include an eye to full employment.

Crypto and other mythological-liquidity-absorbing-silos have provided some usefulness to CBs. Time for them to crash out and leave us with free cash generating investments that are the subject of this decent piece.

I agree that’s what they should do but they will cave. Just look at the Bank of Canada today. You have inflation running at 7% and they will raise in March? lol They should be raising today.

The BOC today said that oil prices will fall because of backwardation in the curve lol. They don’t even understand the oil markets. Inflation is going higher!

Betting that the BOC doesn’t know what they’re doing is not a wise move IMO.

well, when it comes to the oil markets they don’t. Backwardation in the oil curve is bullish for oil prices.

To get inside the mind of the Bank of Canada and other CBs, I highly recommend Mark Carney’s book “Value[s]”. It is very current, including commentary about COVID and cryptocurrencies. It is a major tour of the history of money and the evolution of the current world order – namely fiat currencies backed by independent-but-constrained Central Banks.

not sure what that has to do with the oil market. Crypto’s are a massive bubbble

You suggested/intimated that the Bank of Canada doesn’t know what it’s doing and used the example that they don’t “even understand the oil markets”. I disagree. They know what they’re doing and they understand the various markets in as much as they can be understood. They have a tough job.

Here’s to Rogers Sugar! 🙂

Its still hard for me to believe FED will have the guts to allow stock market drop substantially by raising rates. Unless a black swan arrives (say, a military conflict far-far away), which could be a formal explanation for the robinhood plebs on why their effective investment strategy suddenly returns -50% since inception.

The M1 and M2 velocity are still at all time lows so I don’t see sustained inflation at this point as money isn’t moving around it’s mostly staying in bank accounts. This seems to me more of a one off price reevaluation equalling to the higher amount of money from covid stimulus. Roughly 40% increase in M2 (US) some of this will have to work its way into prices. If unemployment drops further than that could continue to put upward pressures on wages which would sustain inflation. Should be interesting to see how it all plays out. Maybe money supply and velocity mean nothing now and maybe it never did, who really knows?