I’m not a big believer in technical analysis, but the trendlines here are obvious:

Presented without further comment.

Canadian Finance and Economics

I’m not a big believer in technical analysis, but the trendlines here are obvious:

Presented without further comment.

Date: Monday, July 5, 2021

Time: 7:30pm, Pacific Time

Duration: Projected 60 minutes.

Where: Zoom (Registration)

Frequently Asked Questions:

Q: What are you doing?

A: Second quarter, 2021 results. Will discuss various portfolio on-goings and where I see things headed forward. This is in lieu of my typical lengthy quarterly report that I write up which I no longer make publicly available. There should be some time left for Q&A, so please feel free to ask them on the zoom registration.

Q: How do I register?

A: Zoom link is here. I’ll need your city/province or state and country, and if you have any questions in advance just add it to the “Questions and Comments” part of the form. You’ll instantly receive the login to the Zoom channel.

Q: Are you trying to spam me, try to sell me garbage, etc. if I register?

A: If you register for this, I will not harvest your email or send you any solicitations. Also I am not using this to pump and dump any securities to you, although I will certainly offer opinions on what I see.

Q: Why do I have to register? I just want to be anonymous.

A: I’m curious who you are as well.

Q: If I register and don’t show up, will you be mad at me?

A: No.

Q: Will you (Sacha) be on video (i.e. this isn’t just an audio-only stream)?

A: Yes. You’ll get to see me, but the majority will be on “screen share” mode with my web browser and PDFs from SEDAR as I explain what’s going on in my mind as I present.

Q: Will I need to be on video?

A: I’d prefer it, and you are more than welcome to be in your pajamas. No judgements!

Q: Can I be a silent participant?

A: Yes. I might pick on some of you though. Bonus points if you can get your cat on camera.

Q: Is there an archive of the video I can watch later if I can’t make it?

A: No.

Q: Will there be a summary of the video?

A: A short summary will get added to the comments of this posting after the video.

Q: Will there be some other video presentation in the future?

A: Most likely, yes.

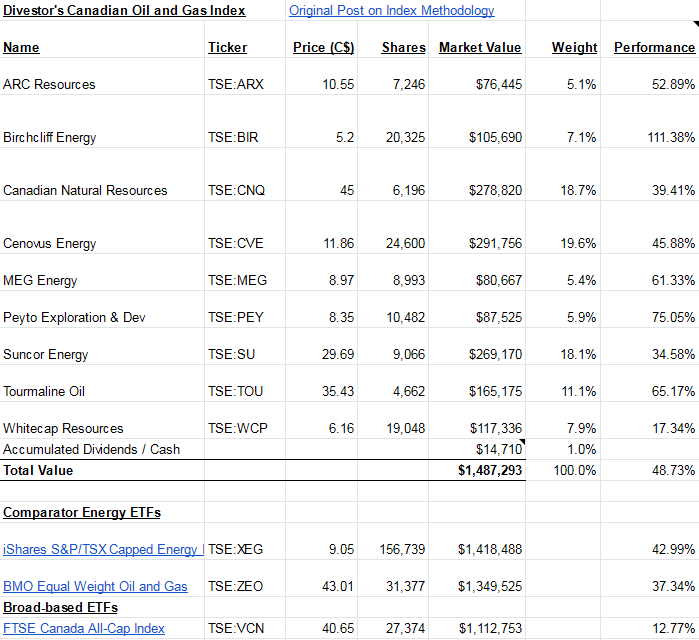

Initial Post (February 5, 2021)

The Divestor Oil and Gas Index has done pretty well since inception. It is up 48.7%, compared to 43.0% for XEG and 37.3% for (the more pipeline-heavy) ZEO.

Birchcliff Energy has been the big winner in the index so far, likely due to the fact it is a pure unhedged natural gas producer, and natural gas has been on fire lately. AECO has spiked above CAD$4/GJ in the recent few days.

The underperformer has been Whitecap Resources, which is likely due to technical factors concerning the recent acquisition of TORC and NAL (which involved stock swapping). With those acquisitions, however, they will be able to increase their drilling inventory considerably for future expansion, while others on the list (the large 3) will be more constrained on growth.

For historical context, read my December 2019 post on Arch Coal where I give a primer on coal mining and discuss Arch Coal.

This is a short briefing update on the renamed company, Arch Resources (NYSE: ARCH).

My timing from the December 2019 post was a bit botched up – indeed, at one point I exited the entire position (during the Covid crisis) but later took a very healthy position at lower prices than they are trading at today. It is a large but not gigantic position currently. I am expecting it to get larger by virtue of appreciation.

Between then and now, other than Covid-19, the other major setback they hit was the regulatory blocking of the merging of their Powder River Basin thermal coal operation with Peabody Energy. This probably cost the company tens of millions of dollars a year in synergies.

It also turned out that they engaged in poor capital allocation. They bought back way too many shares in the 2017/2018 coal boom and were forced to tuck their tails behind their backs when doing some subsequent debt and convertible debt financings to fund the $390 million Leer South Project, but it appears that path is now clear and the need for future capital is gone.

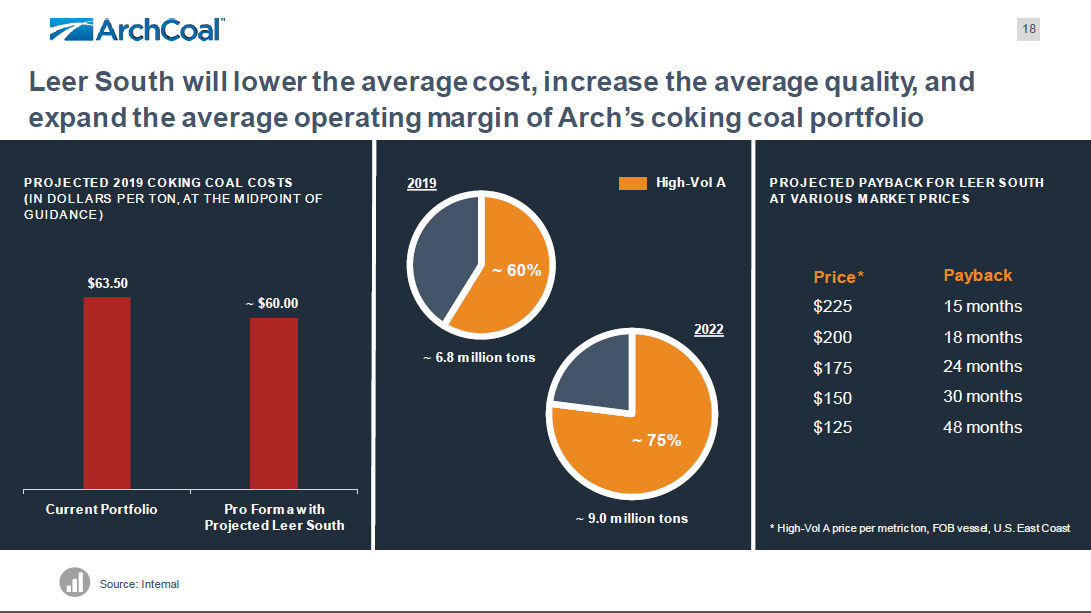

The reason for this is that the Leer South project is due to be operating in Q3-2021 and this project, at current met coal pricing, is going to make a ton of money. The project is anticipated to generate 4 million tons of High-Vol-A coking coal a year for the next couple decades.

Right this very second (partially instigated by the trade war with Australia), prices to China are around US$300/ton. Indirectly, demand from China will continue to suck supply from other suppliers of the world.

Because shipping tens of thousands of tons of material is not an easy feat, transportation logistics became a ‘weighty’ issue. There is a limited capacity to transport from an eastern inland mining area (West Virginia) to the west coast (typically Long Beach, CA), and then onto a freighter across the Pacific Ocean. The opportunities for westward export are limited (indeed, Teck is making a fortune doing this from Elk River mines in southern British Columbia). As a result, the prices that ARCH will be receiving will be well less than US$300/ton, but it will be significantly higher than the averages received in 2019-2020.

High Vol-A, from what I can tell, is around US$190 spot currently. At that price, Leer South, once completed, will contribute an incremental US$500 million or so at existing pricing to the entity, in addition to the existing metallurgical operation. This is crazy amounts of money. Also, by virtue of the entire coal industry being decimated, competitors will have to take their time to open up more met operations (looking at Warrior Met Coal (NYSE: HCC) here), so Arch will eat up the lion’s share of marginal met coal dollars.

There is a lag effect between when coal is mined and when it is sold – contracts and deliveries have to be signed quarters and years in advance, so the pricing seen on GAAP statements will not be see until well after the economic substance of such transactions is actually performed. You can sort of see this being factored in the existing share price (which is the highest it has been since the Covid crisis) but my question will be what sort of valuation the market will ascribe to the company when they generate around $15-20/share next year (current analyst estimates are $7.63). Ultimately it depends on how much this boom for steel production (the primary driver of metallurgical coal consumption) continues world-wide.