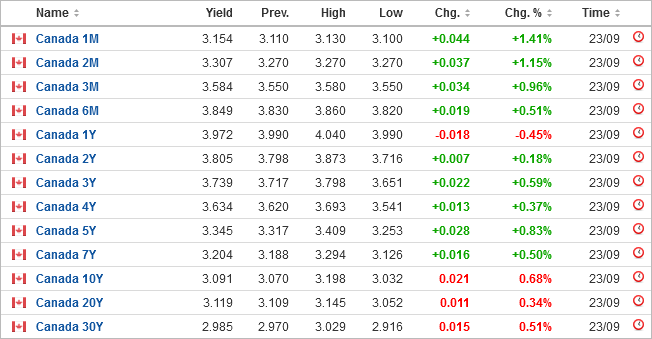

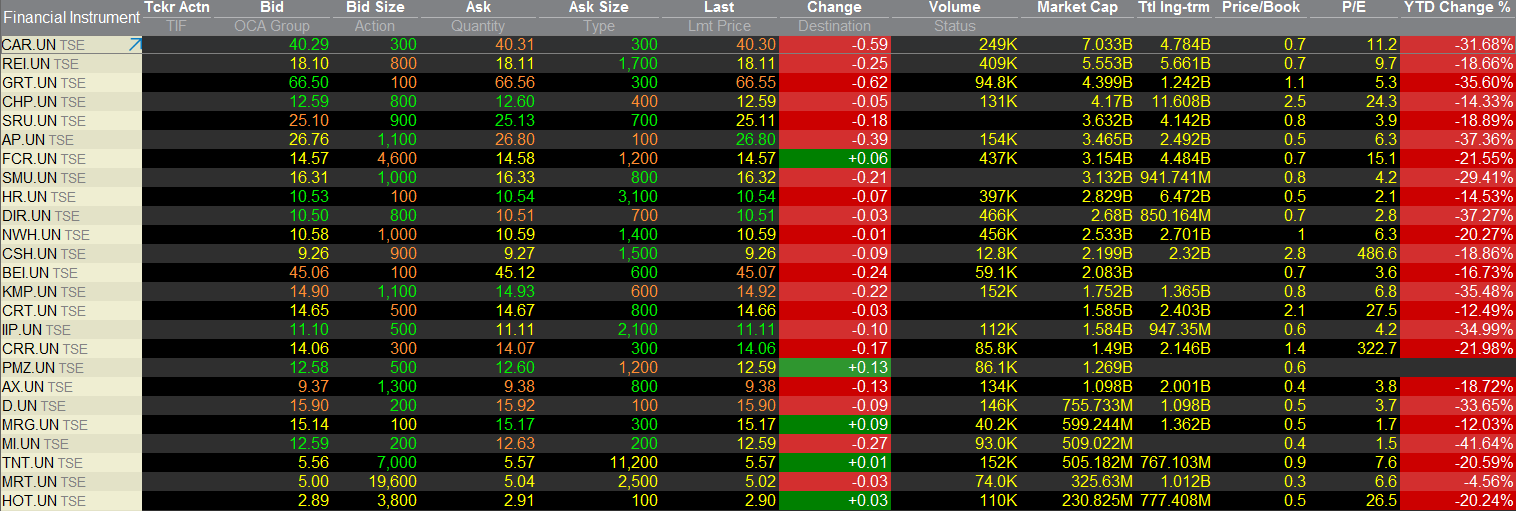

Here is a quick snapshot of most of the major Canadian REITs today. Pay attention to the very right-hand column, which is the Year-to-date performance of their units.

I’ll note that they are all universally down for the year.

Considering that such entities are heavily leveraged with debt to maintain the financing of their property acquisitions, this is not surprising. They are recipients of a double-whammy – higher interest rates will decrease their reported asset values (as they get appraised, they will drop), while at the same time, floating-rate debt will cost more, and any fixed-rate debt that renews will incur a higher financing charge. There is also the problem of what happens if the asset collateral declines in value to the point where the company cannot renew the debt.

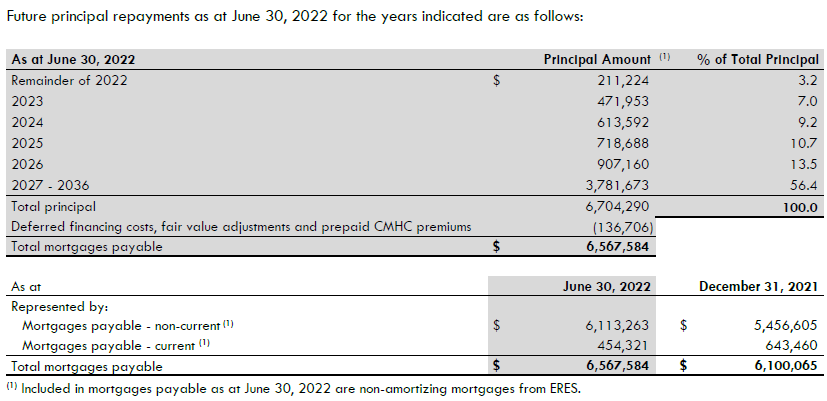

CapREIT (TSX: CAR.UN) is an interesting example. Looking at the June 30, 2022 snapshot:

* $260 million outstanding in floating rate bank loans

* They have $6.6 billion in mortgages payable, 99% of it at fixed rates. The average effective rate is 2.62%.

I’ll spare the agony of going through this in detail (page 45/46 of their MD&A) and just leave it here. Suffice to say, they’ve done a pretty good job insulating their interest rates for now. But they will have to renew these debts at higher rates, assuming the existing rate structure continues. A 1% rise in interest rates results in a $68 million increase in interest expense.

At the current financing arrangement, in the first half of the year CAR.UN made approximately $200 million in FFO, or about $400 million annualized. With 173 million units outstanding, this is $2.31/unit or a current price/FFO of 5.7%. Not a huge return over the risk-free rate.

Interest rates have risen from 0.25% to 3.25%, starting March 2, 2022. While it will not be an instantaneous increase in financing expenses for CAR.UN, it will continue to eat away at their bottom line, unless if they are able to raise rents to compensate.

In a country with one of the highest rent to income ratios for our urban centres, it will be very interesting to see how much higher rents can ratchet.

CAR.UN is nearly entirely residential. The same math works, albeit with different wrinkles, for the commercial, office and industrial REITs, the latter sector historically being in the highest amount of demand.

But as the strangle of higher interest rates persists, these REITs, all of which are very leveraged, will continue to see financing pressure, especially if they do not have the ability to raise rents to compensate.

One would wonder if we are entering into a bad recession how much demand there would be for things such as office space and how much pricing power there would be to open an office in an urban centre. This likely explains why office REITs like Dream Office (TSX: D.UN) have been massively hammered. I would suspect residential would do better than office REITs, but what happens to people when they are unemployed and can’t afford to live in the city? This probably explains our current government’s immigration policy, which is to bring in approximately 440,000 people a year for the next few years, most of which will come to the urban centres.

My other last comment is that I think the 32% drop in CAR.UN year-to-date is highly reflective of the overall state of the real marketplace in terms of residential real estate – just that in the land title markets, the bid/ask spread is so high for individual properties that this magnitude of price decrease has not registered yet. Sellers still want their November 2021 peak pricing, while buyers cannot raise their bids because they can’t get dirt cheap financing any longer.