A moment of market history was when the Hunt Brothers attempted to corner the market on silver (Silver Thursday), which occurred from 1979 to 1980.

If the article is accurate, the Hunt Brothers at one point controlled a third of the world’s privately available silver supplies, primarily using futures contracts.

The collapse of the scheme occurred when the highly leveraged Hunt Brothers could not post sufficient equity to keep their margin loan going.

Fast forward 44 years and we have the situation with Microstrategy and Bitcoin, which appears to be an analogous situation.

On March 11, 2024 via Form 8-K, Microstrategy announced they had purchased 12,000 Bitcoin, during the period between February 26, 2024 and March 10, 2024, for $822 million, mostly with the proceeds of an $800 million convertible debt offering (0.625% coupon, maturing March 15, 2030, convertible into equity at $1498/share). After this filing, Microstrategy owned 205,000 Bitcoins purchased at a cost of $6.91 billion.

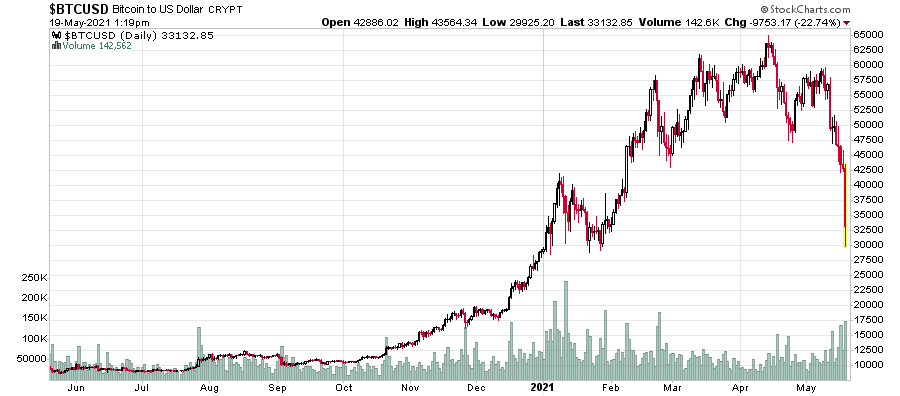

I will note this date range of the purchased Bitcoin appears to line up exactly with the rise from $53,000 per Bitcoin to around the $67,000 we see today:

This wasn’t enough.

On March 15, 2024, Microstrategy closed another convertible bond offering, $525 million (0.875% coupon, maturing March 15, 2031, convertible into equity at $2327/share). Unlike the previous offering, this offering claimed to be used for general corporate purposes and the purchase of additional Bitcoins.

With the stock price (after a 15% drop as of the writing of this article) at about $1,500 a share, they are obviously continuing to leverage themselves to the hilt in order to keep the price of Bitcoin high. The liquidity of Bitcoin itself is somewhat questionable – throwing $820 million into Bitcoin over 10 trading days is enough to spike it around 30-40% in value. Microstrategy is clearly trying to keep as much gasoline onto the Bitcoin fire as it can, as its market valuation is tied to the hip with it. The primary owner and chairman, Michael Saylor, is dumping stock like crazy while the going is good.

My only question is when will this house of cards collapse?

The answer is strange – it depends on whether the stock collapses. It may not happen soon. The looming debt maturity was going to be in 2025 with a $650 million convertible note, but it is likely that it will be converted at approximately $398/share. The next looming debt maturity are the 2027 notes, which has a conversion price of $1432/share, which is much closer to the current stock price.

As long as the company can keep the stock price up and be able to avoid raising cash (presumably by selling Bitcoin!) in order to pay for the maturity, this can go indefinitely.

The cycle would be: issue equity or convertible debt financing -> purchase bitcoins -> raise the price of bitcoins -> higher MSTR stock valuation -> issue equity or convertible debt financing

The question will eventually be settled by somebody with deeper pockets than Microstrategy that decides to short enough Bitcoin and also Microstrategy stock to get an even larger payoff in the subsequent collapse. They would need to force Microstrategy to sell its Bitcoin.