This is a very different trigger to a market crash because there is a gigantic element of a change in psychology, all in a very short period of time. The psychology (everything is cancelled, stay at home, don’t go to work, etc.) leads to cultural change, and there is demand to be seen to “do something”, to quell the panic. The psychology is causing the economics to change, which in turn causes the market to change.

When you have a massive dislocation in psychology, coupled with a cultural shift, and disruption in the economic landscape, it is no wonder there is huge volatility associated with it. If you get the medium term correct and don’t get cashed out in the process (i.e. be a victim of a massive margin call), things should go reasonably well if you’re invested in one of the privileged sectors that actually have to do something with the functioning of the overall economy (this means if you own cruise ship stocks, needless to say you’re in big trouble).

The cruise industry will recover to a degree, but it will take a lot of time, and there will be have to be a ton of marketing spent on how the ‘new’ ships being constructed actually have air filtration systems, sanitation standards, and aren’t cesspools of shared viral contamination. This will take years. I do not see a quick recovery in this industry.

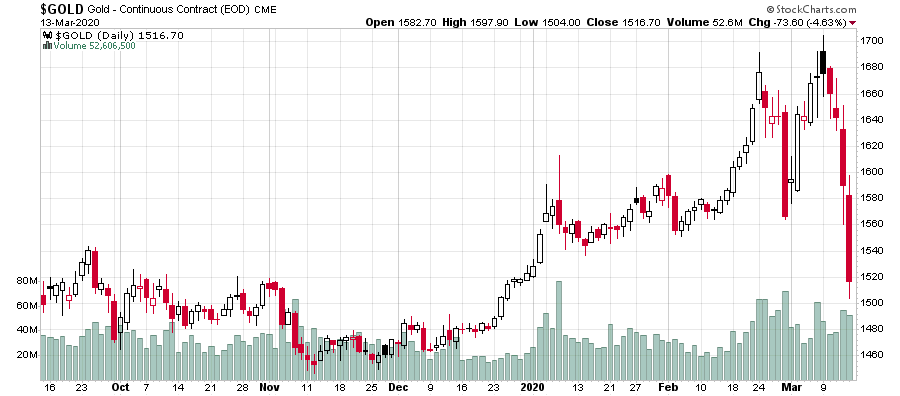

Central banks and the federal reserve can fight a financial crisis by perpetuating an “extend and pretend” strategy, where credit is available for anybody and everything that wants it. This is the playbook that is going on right now – you are going to see the financial markets being drenched in liquidity like that which has never been seen since the 2008 economic crisis. We are talking about trillions of dollars in availability. You see on FRED how there is 2.5 trillion outstanding in treasury securities bought by the Fed? That’s going up. Like to around 5 trillion. This is the equivalent of the Federal Reserve dropping short term interest rates to something like negative 4 percent (this is just a ‘gut feel’ number, not a scientific amount). It is a playbook that is going to cause incredible mass distortions when this finally gets sorted out. Nobody is talking about the S&P 500 going to 4000 at this point but in the medium term once all of this liquidity goes somewhere, that’s exactly what is going to happen, conveniently in time for Donald Trump’s re-election.

This liquidity, however, is useless if it doesn’t get to the companies that have short-term liquidity issues (debt rollovers, credit facilities that are about to expire and/or facing covenant defaults given the impending revenue drops) – but this will be arbitrated somewhere in the continuation of “extend and pretend”. But the root cause is a gigantic change in psychology perpetuated by a virus. A financial crisis is caused by some large players that are unable to pay their bills. The Federal Reserve can solve this by giving them money, but they cannot re-program people’s brains into believing a virus won’t kill them.

(As I was writing this, I see the Federal Reserve has just dropped interest rates to zero, ahead of their scheduled policy meeting this Tuesday/Wednesday, coupled with a coordinated press release by various global banks regarding the available of US dollar swaps).

The Federal Reserve has very good tools for fighting a financial crisis. But this is not a financial crisis we are facing – the financial crisis is a result of what is actually being faced, which is a psychological crisis, the perception that there is a virus out there that is going to kill us all. Unlike a scenario where an asteroid is detected to be hitting earth in a year and we are all going to die no matter what, this Covid-19 scenario does have some silver linings:

1. The world’s best minds right now are working on medications to combat this, and the usual 10-year timeline from pre-clinical, to Phase 1, Phase 2a, 2b, and Phase 3 clinical testing, followed by an FDA review panel, will be shortened down to something like a month or two (even if this medication offers the most peripheral clinical benefit, there will be a massive placebo effect that will have a real psychological benefit);

2. I’ve read mixed messages whether Coronaviruses naturally fade away in the spring (as does typical flu season bugs, noting this analogy does not directly apply), but if so, we are approaching it;

3. Most people that get Covid-19 exhibit mild to no symptoms.

4. Even those people that do get really bad symptoms have significant risk factors which would suggest their vulnerability (age 65+, heart/lung conditions or diabetes, but in any instance, it involves people with reduced cardiovascular/respiratory capacity) – these people are the ones that should be really, really careful;

5. And yes, the vast majority of us (we are talking 99.9%+ of the world population) will survive this, and even those that get Covid-19, around 98% or so will survive it, and over 99% if you get it and you’re under the age of 60.

However, we all look at these diagnosis/death curves of countries that are currently in full-blown panic mode (Italy being the prime example) where 3,000 people daily are getting confirmed with COVID-19; and coupled with a massive media attempt to instill panic and fear about how everything is all going to hell – cancellations, toilet paper taken off shelves, and just generally nutty behavior resulting from snapshots of the most extreme of extreme actions taken by people.

I’ve had to shut off or very purposefully moderate my own digestion of mass media news on Covid-19 because it is very difficult to mentally process everything that is getting thrown out there – there is just too much sample bias, and fake news, and the like. It causes panic and emotional feelings are precisely the opposite of what makes for good financial decision-making in the markets. Complicating the matters, however, is that one has to have a good pulse on the emotions of others in order to optimize these financial decisions – if you know that panic will spread even further, then it is rational to wait until that point to dive in.

Usually the VIX is a reasonably good barometer of this.

A comment on media, especially social media. Media invokes a process of social validation. When enough people see something enough times (gotta buy toilet paper!), they tend to believe it, and their behaviour changes in accordance with this, and this in itself is enough to cause a change.

My own personal n=1 sample (and also selection bias, and first-hand bias), you’d think that going to Costco it would have been a zoo, but going to the local Costco today, a Sunday at noon-time, things were shockingly orderly, the guy at the front gate gave me a lysol wipe to wipe down the buggy, and there was toilet paper available (which I did not buy), and the meats and vegetables were all there, and at the shopping exit, I was so shocked that the cashier’s assistant actually helped me unload the cart onto the conveyor belt. What the heck? You’d get the impression that there would be lines and lines to get in, let alone in-and-out like going through a McDonalds drive-through.

About the media – there is no way to build societal resilience against media-induced panic unless if you have a very centralized (read: government controlled) grip on the media, or the population has the mental capacity to consume it wisely (let’s face it – that’s definitely not happening).

This is probably how China and Singapore managed to get a good grip on Covid-19. Particular in the case of China, they didn’t mess around and just shut off everything for a period of time, turned on the mass censorship, and have the enforcement mechanisms to severely punish those that are non-compliant (i.e. lock them up somewhere). Singapore has the same mechanism – if you’re caught, you face severe penalties.

More democratic societies like South Korea and Japan also fared fairly well, but their societies have a certain variety of cultural immunity by virtue of being more collectivist, in addition to having to deal with things such as SARS and the like. They also seemed to be much more prepared in terms of medical protocols in place (for example, South Korea’s testing regime was very aggressive).

China right now is trying to figure out how to use this to destabilize the rest of the western world (as evidenced by the ‘we’ll withhold medical supplies if you forbid Huawei 5G equipment’, and of course the conspiracy theories affirmed by their diplomats about how the USA sent the Coronavirus to China). They’re playing with fire.

I have seen more emails from organizations about Covid-19 than I have ever seen about any public issue before in my lifetime. Organizations that you wouldn’t suspect that would be sending out such mass public emails are sending them, informing the public of what their strategies are. It is very unusual. Just as I was writing this post, RBC sent out an email saying “COVID-19: How RBC is helping our business clients”. This is about the 15th public service announcement I’ve received on the matter from various third parties.

In terms of the world economy, we are seeing borders being shut down. If any companies you own are depending on international trade, there will be exposure, but for the most part, it is people and not goods that are being prevented from crossing borders (this is the case in Canada/USA – I have no idea what’s going on in the EU). The USA is domestically a self-sufficient country in terms of its natural resources, and if it didn’t export a good chunk of its manufacturing capacity abroad, it would also be self-sufficient in terms of manufacturing (which could indeed be ramped up with time).

East Asia is also on high alert, but appear to be mostly through it.

The big geopolitical implication of Covid-19 is likely a forced acceleration of the rollback of globalization to some extent, and this will strongly affect international trade, at least in the short term. Countries with strong domestic economies will fare well (the USA should survive this well). Countries that have significant dependencies will be impacted. Canada, by virtue of having a huge shared border with the USA, should be able to piggy-back on the USA’s fortunes, but this is in spite of the tremendous incompetence we’ve seen in our government to date, rather than because of it. God forbid if the Russians actually invaded us.

What will we expect to see in the next couple weeks? More diagnosed people with Covid-19, more deaths, and more bad news from the media.

However, life will eventually have to return. People will have to go to work. The threat of the USSR launching nuclear missiles on us will be omnipresent, and just like that, the threat of Covid-19 will be accepted as an everyday risk in life, similar to a risk of getting run over on the street, getting cancer, or some other tragedy. The transition will require a change in psychology to get there, and when the media shifts, it will be fairly obvious when it occurs (and the markets, which have priced in this hysteria, will undoubtedly be lower than a 75-value VIX). But right now, panic is the big story. If you don’t get cleaned out on a margin call, at least in nominal dollars, you should do well.

Parameters for investment:

1. Avoid cross-border international exposure

2. Avoid domestic companies that do not have demand destruction (e.g. hotel REITs)

3. Avoid companies with short-term maturities/liquidity risk/covenants

4. Avoid oil producers (for now) – they’re going to get totally gong-showed in this one-two-three knockout session

5. Avoid “people-sensitive” industries that rely on foot traffic (retail, hospitality, sporting)

6. Consider: anything that would be the recipient of government stimulus spending

7. Consider: companies with recurring revenues (creativity software in particular comes to mind, e.g. I would think Autodesk/Adobe would do reasonably well, but these are the largest of large-cap examples)

Stay solvent!