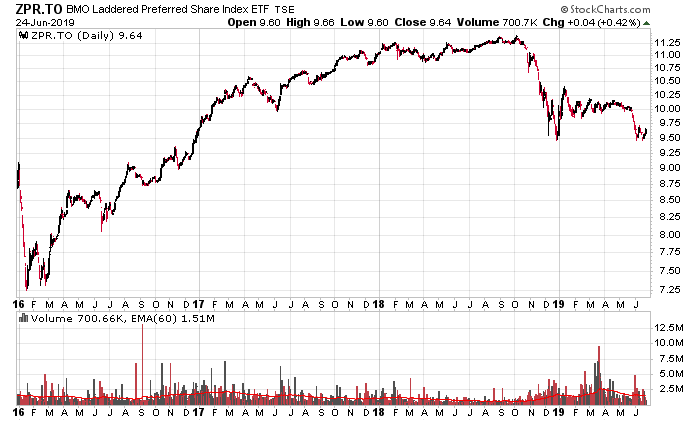

Early 2016 was a good time to invest in Canadian preferred shares, and there was also a lot of carnage in the equity market at the time. Five-year government bond yields bottomed at 0.48% in February 2016, and you can see the damage it did to the preferred share market – ZPR is an ETF that tracks 5-year rate resets:

What is interesting is a well-timed entry on the bottom (not completely clairvoyant, but say $7.50/unit) and an exit anytime between October 2017 to 2018 would have netted a total return that exceeded the TSX with less risk. Of course, you can’t determine those preferred shares will do better than the TSX when you’re sitting at your computer console in February 2016!

Today’s investing environment has plenty of parallels – the 5-year interest rate has dropped to 135bps from 240bps back in October. If 5-year yields continue to drop further, there is a high degree of likelihood that preferred shares will also be sold down to levels seen in 2016.

The question is getting the timing correct.

A lot of retail investors get burnt by buying into a relatively high yield product thinking it is safe. While the yield itself may be safe (it has been awhile since I can recall a dividend suspension in the Canadian preferred share marketplace beyond Aimia and some really garbage split-share corps), the capital is most certainly at risk. It looks like a very easy leveraged trade on paper when margin rates are 2.5% and you see a financial instrument at 5%, but how much pain can you take when the yield goes to 6%? 7%? You’ve just lost nearly 17% and 29% of your capital, respectively.

Using a real example, investors in Brookfield Preferred Shares series 30 (TSX: BAM.PR.Z) back in September was trading at par, had a near-guarantee 4.7% yield, and a rate reset of 2.96% over the 5-year government bond rate. Some enterprising chap sees margin rates at 2.5% and decides to invest $50,000 cash to buy $100,000 of BAM.PR.Z. Now they’re sitting on $23,000 in equity plus $3,500 in accumulated dividends and they would have surely received a margin call (or would be very close to one). How much of the population out there is leveraged to preferred shares in this manner and are feeling nervous? How many will hit the sell button to take the tax hit and move away from this “guaranteed leveraged return”?

Ideally when they all want to cash out, that’s the time to get in. Doesn’t quite feel time yet.