For the first time in ages, the Royal Canadian Mint ETR (TSX: MNT) is trading within a percentage point of its net asset value – prior to this it was trading at a significant premium.

This could be because the price of gold, at least as measured in US dollars, has declined from a high of about US$1,950 during the election to US$1,800 today and suddenly gold is no longer in vogue. It is difficult to prescribe what causes price decreases in gold, but given its perception of a “when everything goes to hell” metal, my guess is that the fallout of the presidential election is alleviating to those that went into gold.

Another solution espoused by monetary doomsday proponents is the purchase of cryptocurrencies.

Here is my current theory of how things will end up.

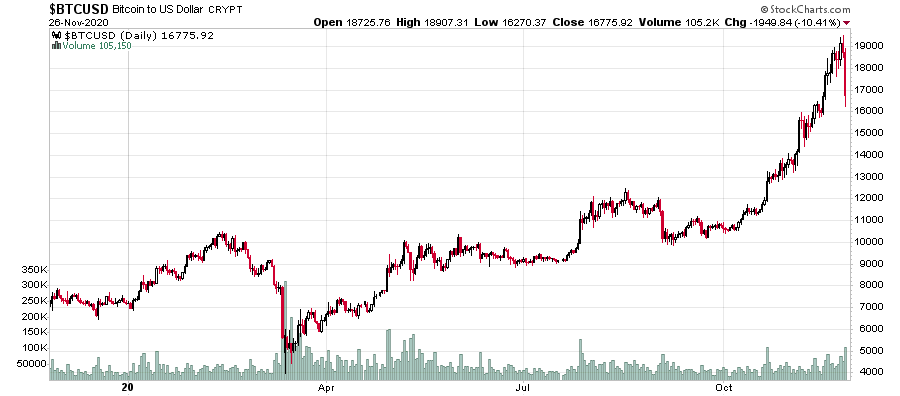

You’re going to continue hearing more and more about Bitcoin until the last dollar has been sucked up into this global Ponzi vacuum – it’s up about US$1,000/coin today. The price is going to continue to rise because of forced buying (ETFs) and rampant speculation (easy access through financial apps that can be loaded on anybody’s smartphone). You’re going to hear your friends, neighbours, etc., get into the action, and you will be aggravated to hear about fortunes made because they bought half a bitcoin and it went up ten-fold in a month, while you are just sitting on your boring shares of Fortis and Enbridge, clipping quarterly dividend coupons at a hundred times less magnitude.

The disparity in performance going to drive a lot of people insane. Literally insane. Seeing your friend pull up to your doorstep in a Lambo (“Look! I sold some bitcoin!”) while you’ve just made an extra value meal in dividends fuels a lot of psychological resentment. After finishing drag racing on the freeway in your friend’s Lambo, picking up your Big Mac and fries at the McDonalds drive-through with your dividend cheque, you both will then go home and buy some more bitcoins.

All I can suggest to keep your sanity is to go to the library (assuming your local branch hasn’t been shut down by the COVID scourge) and get some history reference books on what happened during the Dutch tulip bulb mania. This is the closest analogy I can think of to the current situation. One difference between the 17th century and today’s era is that in today’s era, things move much, much faster, including Lambos vs. horse carriages. This includes price movement and capital mobility. The Tulip Bulb mania took about 3 years to form, and the crescendo went over about four months of trading. With bitcoin, I would not be shocked that the initial collapse will be a price drop of over 50% in a 1 week period. It will be massively disruptive.

You will also hear at the same time after this price collapse a bunch of people saying this is the greatest chance to get in of all times.

Most people in finance have some knowledge of the Tulip Bulb Mania. However, many less people (including Wikipedia) have a historical knowledge of another great pyramid scheme which brought down the country of Albania in 1997. This made for a very fascinating study although there were few references to it in English. Another difference is that Albania wasn’t exactly a rich country at that time, so the absolute amount of capital sucked into this scheme was relatively limited by comparison, while Bitcoin has a nearly global audience.

History is repeating again, right before your very eyes! What a time to be living.

How do we begin to model this?

Unlike Tulip Bulbs, which trade in discrete quantities, Bitcoin is divisible in units of 100 millionths of a bitcoin, which means anybody will be able to get into the game – with Tulip Bulbs, the purchasing power of one bulb at its peak was massive, which limited the ability for people to get in (they had to put up margin collateral). With bitcoin, anybody with a cell phone and a bank account can get in.

There are about 18.6 million bitcoin outstanding at present, with a good chunk of this (at the onset of creation) apparently not used, and with people losing coins here and there. At US$19,000/coin, the market capitalization of the entire bitcoin set is US$350 billion. I think you can now make a good argument this could go a lot larger before the bottom falls out on this one. I initially thought the market cap of bitcoin would be roughly restricted to the largest cap companies trading on the public exchanges (currently, this would be Apple at around $2 trillion) but for a true mania, shouldn’t it go higher? There’s clearly room to head up to $100k/coin. The question is – how much cash will this suck up before demand stops?

Kind of makes my earlier predictions half a decade ago of a $10k ceiling to be pretty ridiculous, but then again, I never knew Bitcoin would be the vessel of the next tulip mania. Times really haven’t changed.