Canada’s political environment is really easy to model – whatever is in the best interests of Ontario and Quebec tends to become national policy, irrespective to the impact it has on jurisdictions west of Ontario.

Let’s look at the proposed national carbon tax, which will take the carbon tax from $30/tonne CO2-equivalent in 2020 to $170 in 2030:

2019 – $20/tonne

2020 – $30/tonne (+10)

2021 – $40/tonne (+10)

2022 – $50/tonne (+10)

2023 – $65/tonne (+15)

2024 – $80/tonne (+15)

….

2030 – $170/ton

To put this into context, at CAD$40/ton, a gigajoule of natural gas has a carbon tax of CAD$1.99/GJ applied to it. At CAD$170/ton, that is CAD$8.44/GJ. The AECO market price for natural gas at the moment (note, it is December when there is peak demand) is CAD$2.53/GJ. The projected carbon tax at the end of the decade will be over three times the commodity cost. Needless to say, this puts Canadian companies that rely on natural gas consumption at significant cost disadvantages over jurisdictions that do not impose such taxes (the United States, for one).

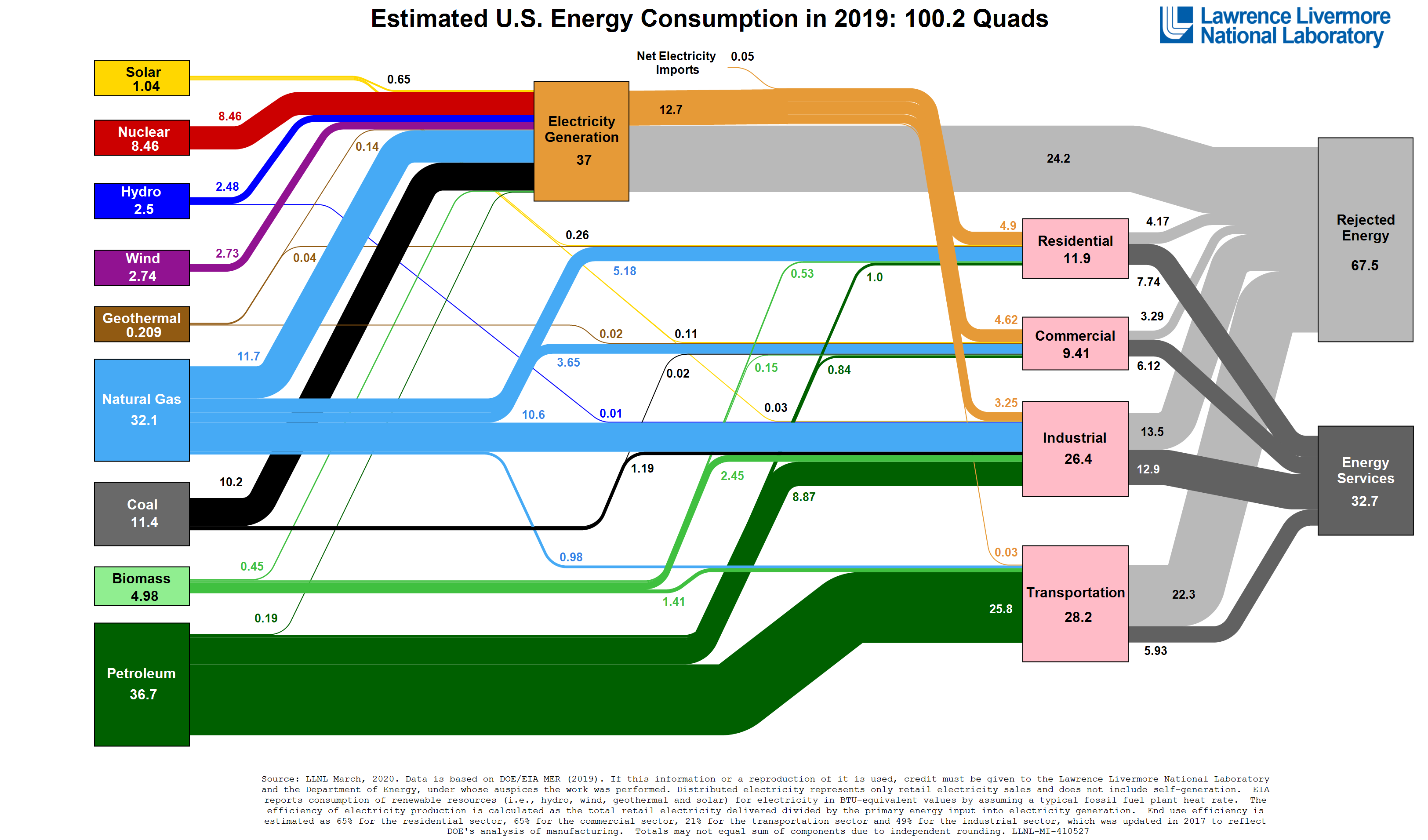

Let’s take a look at electricity generation, for example.

On the electricity generation side, we see that 99% of Quebec’s electric generation comes from non-carbon taxed sources – Hydro (94%) and Wind (5%). Ontario’s non-carbon taxed electricity (91%) is Nuclear (57%), Hydro (24%), Wind (8%) and Solar (2%).

Electricity generation is about a third of energy consumption. A really good illustration is provided by the Lawrence Livermore Labs (this was linked to from one of Peyto’s president’s reports):

You can find detailed Canadian data here, albeit not in such a convenient manner.

One issue is that it takes a lot of energy to extract energy (and resources such as iron ore, copper and pretty much anything else in the ground), and of course this puts Alberta, Saskatchewan and British Columbia at a significant disadvantage with this cost regime.

The political aim with this carbon tax continues to be levying a tax that purports to be country-wide, but the impact is concentrated on a regional basis which conveniently happens to be in areas where there is the least support for the ruling party in government.

For those of you that claim there is a corresponding payment to individuals, while this might be true at first, it is performed to get initial acceptance while the proverbial frog boils in the pot. The rebate will be whittled away and eliminated over the coming years in the name of equality. This will come in the form of income testing these “climate action incentive” payments. Eventually the threshold will be lowered to the maximal vote-buying point and any pretense of the tax being “revenue-neutral” will be eliminated, similar to what happened in British Columbia when they dispensed of the notion in 2017. I wrote about the myth of carbon tax revenue neutrality for another publication back in December 2018.

As an example, in British Columbia, it is estimated in the 2020/2021 fiscal year that the carbon tax will raise about $2 billion in revenues, or about $400 per British Columbian. About $300 million in total is estimated to be directly paid back to people (initially called the “Climate Action Dividend” but renamed “Climate Action Tax Credit” as the word “dividend” appears to be dirty with the current BC NDP government) – normally this Climate Action Tax Credit is $174.50/person that earns less than $35,748 (or family income of $41,708), but this was topped up to $218 due to COVID-19. For relation, the median family income in BC is around $90,000.

In terms of the net carbon tax revenue, the $1.7 billion the BC government collects is free for them to do whatever they want. Nationally, it will work the same way, at least for the provinces that do not levy their own carbon taxes.

The decision to raise carbon taxes across Canada does not cost the ruling Liberal party much politically, but will allow them to raise disproportionately high revenues from those areas and enable the redistribution to their vote-friendly base, namely Ontario and Quebec. Such is the nature of politics and power.