The big news yesterday that made ripples was Riocan REIT (TSX: REI.UN) slashing its monthly distribution from 12 cents to 98 cents.

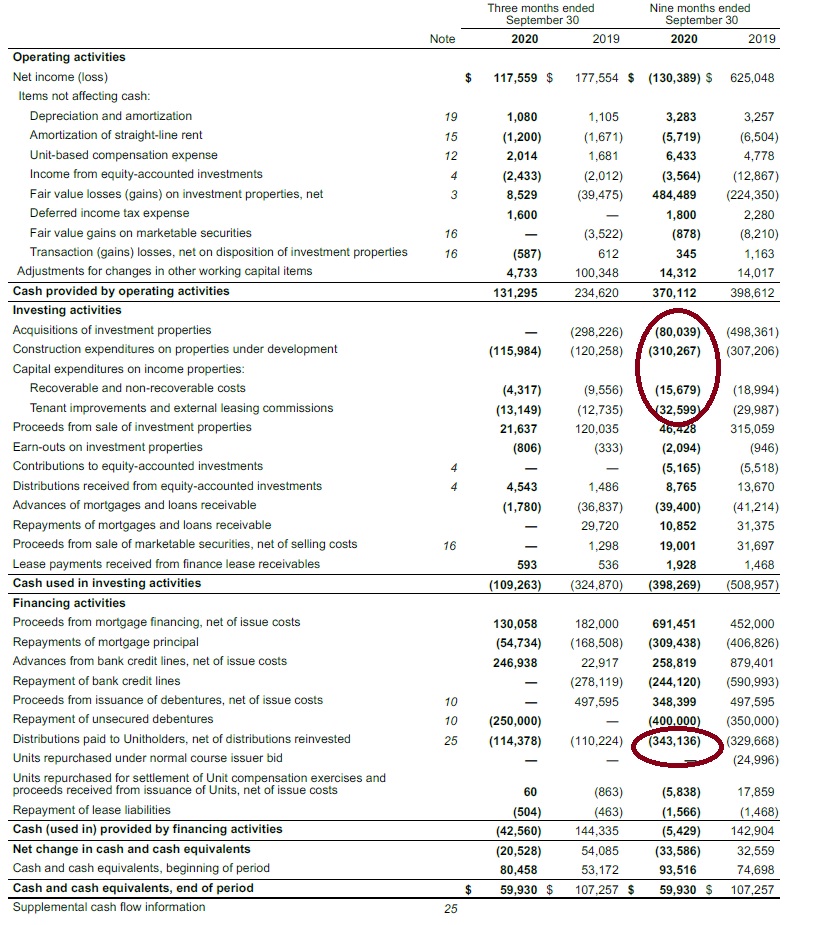

I’m surprised they didn’t cut it further. Their cash flow statement shows that most of their operating cash flow goes out the door in distributions, not leaving a lot left over for construction capital:

A few comments:

1. Riocan is mostly a GTA REIT; about 50% of their revenues come from Toronto, another 1/8th from Ottawa, and almost 1/5th from Alberta. Understanding the GTA environment is key to a proper projection of Riocan’s fortunes, which brings me to point #2:

2. Retail conversions to residential is a component of Riocan’s new business model. This will require capital, a lot more of it. The last moment you want capital markets to constrain your inventory building is in the middle of a construction project. Although Riocan is not in any danger of not being able to raise capital (indeed, they made an impressive unsecured capital raise in March of this year at 2.36%), one never knows in the future.

3. My aversion to the REIT sector has not changed since the COVID-19 crisis occurred.

4. Most importantly – the reaction to this highly suggests that many people in retail-land have units in Riocan. It has been the most commented post on Reddit’s /r/CanadianInvestor in ages, and also it got comments on the Globe and Mail, etc, etc. This is a widely-looked at and widely-owned investment and it highly suggests that there are going to be smarter people than myself out there that will be getting the pricing correct. There are more obscure REITs out there which are more likely to have mispricings if you choose to venture into the sector.

I think they cut it to .08…33%

Thanks, had a bad math moment there.